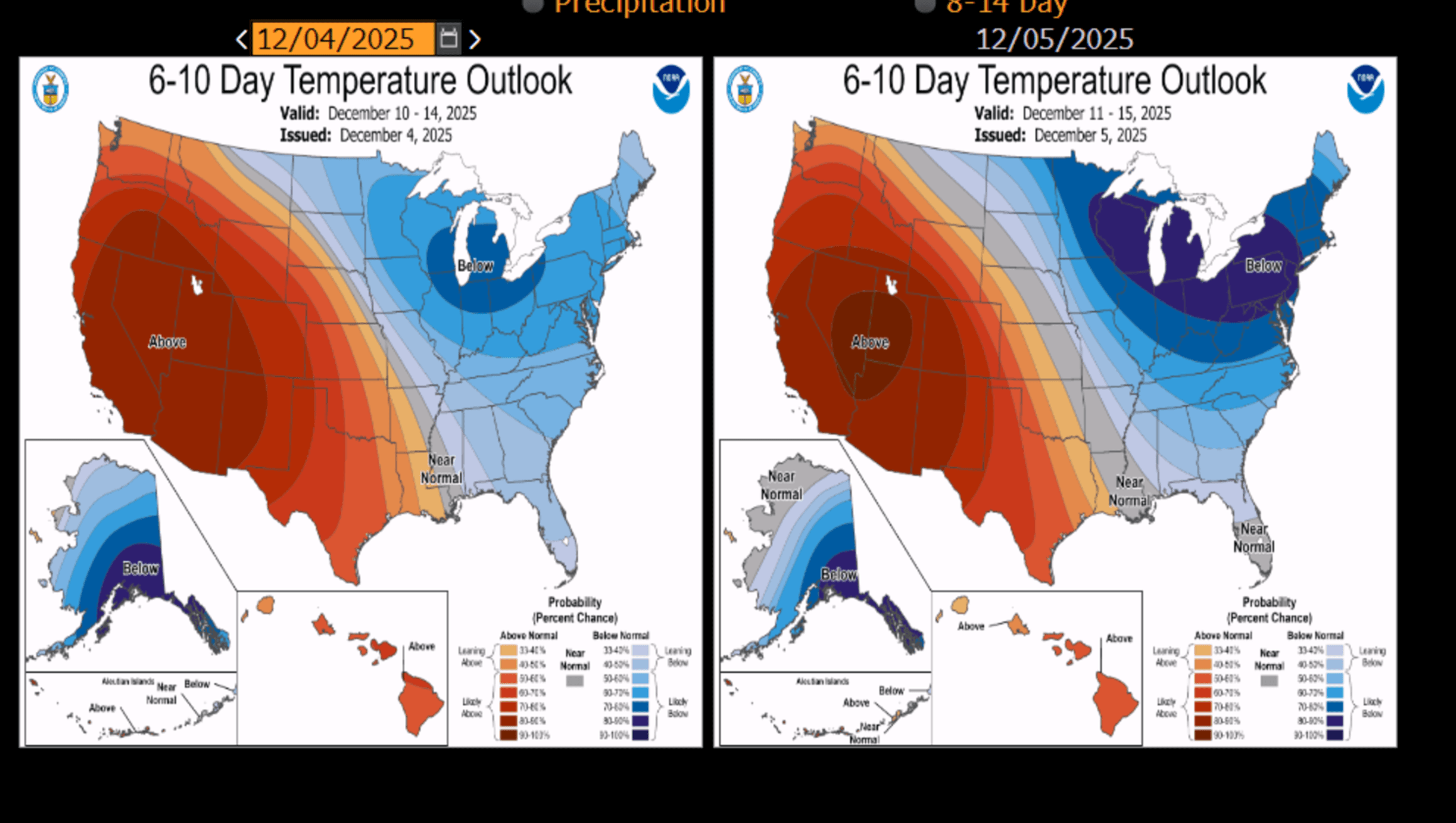

US NATGAS: NOAA 6-10 Day Revised Temp Outlook Shows Drastic Cold Patterns

The NOAA 6-10 outlook shows drastically below-normal temperatures for the Northeast and Midwest

- Jan 26 NG closed today at a three-year high $5.289.

- December is shaping up to be colder than the 10-year and 30-year averages, said Darrell Fletcher, managing director of commodities at Bannockburn Capital Markets.

Cash prices at Algonquin Citygate averaged $20.53 on Dec 4, while Transco Zone 6 NY averaged $7.33.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Pullback Exposes Key Short-Term Support

- RES 4: 0.6707 High Sep 17 and a bull trigger

- RES 3: 0.6666 2.0% 10-dma Envelope

- RES 2: 0.6644 76.4% retracement of the Sep-Oct bear leg

- RES 1: 0.6542/0.6618 50-day EMA / High Oct 29

- PRICE: 0.6497 @ 16:18 GMT Nov 5

- SUP 1: 0.6459 Intraday low

- SUP 2: 0.6440 Low Oct 14 and key support

- SUP 3: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

A softer short-term tone in AUDUSD remains intact for now and this week’s move lower reinforces this theme. The pair has also traded through the 50-day EMA - a bearish development that undermines a recent bullish theme. A continuation lower would signal scope for an extension towards the first key support at 0.6440, the Oct 14 low. Key resistance and a short-term bull trigger is at 0.6618, the Oct 29 high. First resistance is at 0.6542, the 50-day EMA.

US TSYS/SUPPLY: Treasury Advisory Committee Envisages Next Upsizing In FY2027

The Treasury's advisory committee (TBAC) at the November Refunding echoed the Treasury policy statement in eyeing a potential upsizing in coupon sizes albeit on the fairly distant horizon. The TBAC report to the Secretary noted: "The Committee believes that current projections could warrant increases in coupon issuance in FY2027" (which starts in October 2026, in line for an increase as early as the November 2026 Refunding which is MNI's base case). There was no timing mentioned in the previous quarter's edition of the statement.

- Other tidbits from the TBAC materials in this Refunding:

- While Treasury's current funding mix was seen to be close to optimal, TBAC was charged with examining a “dynamic issuance strategy” "that shifts issuance mix in response to market conditions". One of the conclusions is that "A strategy that responds to moves in term premium could improve Treasury’s cost profile and remain consistent with “regular and predictable” debt management principles. Such a strategy needs further work to design its parameters, assess its impact, and consider market participants’ reactions to its implementation."

- TBAC warned that there could be direct rates market consequences of the BLS failing to publish both a September and October CPI report: "The Committee highlighted industry focus on the potential implications for the inflation swaps market if multiple CPI prints are missed, which could affect both demand for and secondary market liquidity in TIPS."

- The outlook for demand/supply for Treasuries remained sanguine, though there were some risks to revenue seen coming from legal challenges to the White House's tariffs: "The balance between supply and demand for US Treasuries remains a key focus for investors both domestically and abroad. Deficits are projected to be $1.940tn in FY2026 and $2.052tn in FY2027 in the latest dealer survey, $106bn lower in aggregate compared to last quarter’s estimates. The level of tariff revenue has become an important input into deficit projections, meaning markets are watching the outcome of trade negotiations as well as court decisions that could affect tariff implementation. Overall, demand at auctions remains robust, with bid-to-cover ratios in normal ranges."

- The report highlighted recent funding market pressures: "In October, short-term interest rates showed signs of upward pressure. There was robust discussion among the Committee as to whether this was more of a supply/collateral story or a demand/reserves story – ultimately some of both ... There was discussion about whether reserve levels are moving from “abundant” to “ample"" - though no firm conclusions were reached.

- TBAC also discussed the ramping up of Treasury cash in October to $1T, which was above Treasury's stated end-quarter target of $850B - concluding that better communication over cash targets could be beneficial. "The Committee felt that market participants may not appreciate the need for flexible TGA balances intra-quarter vis-a-vis stated quarter-end assumptions (currently $850b), as per policy, and suggested enhanced communication as an item for further consideration for Treasury."

US TSYS: ADP Payrolls Growth Stabilized, Tsy Contemplates Coupon Size Inc

- Tsys initially retreated after larger than expected ADP jobs gain - then extended lows after in-line refunding annc - while coupon sizes expected to remain stable for "at least the next several quarters" - Tsy contemplating coupon size increase and no discussion of ramping up bills in lieu adding to bear curve steepening.

- Tsys tracked German Bunds lower with no obvious headline of Block driver, unlikely that comment from Fed Miran adding to the decline: "DATA SUGGEST RATES CAN BE A LITTLE LOWER THAN THEY ARE" while "KEEPING POLICY THAT RESTRICTIVE RUNS UNNECESSARY RISKS," Bbg.

- Currently, the Dec'25 10Y contract trades -15 at 112-10 vs. 112-09.5 low, nearing the reversal trigger at 112-06. The weakness was triggered by the clean break below the 50-day EMA, currently at 112-26+, and highlights potential for a deeper retracement near-term. 10Y yield +.0720 at 4.1571%. Curves bear steepen: 2s10s +1.637 at 52.366, 5s30s +.412 at 97.121.

- Conservative Supreme Court justices Amy Coney Barrett, Neil Gorsuch, and Chief Justice John Roberts all appeared sceptical of President Donald Trump’s reciprocal tariffs, during questions to Trump’s lawyer during today’s hearing. The implied probability of Trump winning the case has dropped to 20%, per Polymarket.

- Due to the ongoing, weekly Jobless Claims, Non-Farm Productivity / Unit Labor Costs and Wholesale Inventories / Sales has been suspended. That leaves: Challenger Job Cuts (0730ET), Revelio Public Labor Statistics and Chicago Fed Labor Market Indicator (both 0830ET).

- Myriad Fed speakers on tap tomorrow: NY Fed Williams lecture at Goethe Univ. Frankfurt (1100ET), Fed Gov Barr moderated discussion community development (1100ET), Cleveland Fed Hammack Economic Club of NY (1200ET), Fed Gov Waller CB & Payments panel (1530ET), Philly Fed Paulson Consumer Finance Inst (1630ET), StL Fed Musalem fireside chat on policy (1730ET).