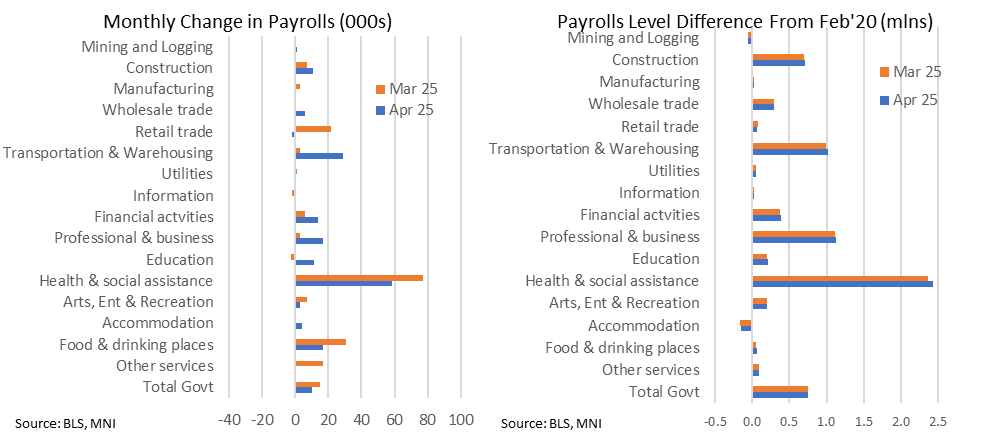

US DATA: No Sign Of Early Tariff Disruption In Payrolls Industry Breakdown

The breakdown of monthly payrolls growth is one of general resilience, with perhaps the greatest surprise being the strength in transportation & warehousing that shows no sign of adverse impacts from tariffs. Of course, this is still early for job losses to be showing up, especially with the pay period including April 12th being still close to the Apr 2 "Liberation Day" tariff announcements (before the partial backtracking on Apr 9) with companies still assessing how to respond under heightened uncertainty.

The below runs through some notable industries this month, all showing seasonally adjusted M/M changes:

- Health & social assistance: still the single largest driver of jobs growth, adding another 58k after 77k in Mar and 57k in Feb.

- Transportation & warehousing: 29k in Apr after 3k in Mar and 18k in Feb. An impressive figure that doesn’t show any imminent signs of net layoffs in tariff-sensitive industries. Note that this is corroborated by Wednesday’s ADP report were trade, transport & utilities was the second strongest sector for hiring on the month.

- Food & drinking places: 17k in Apr after 31k in Mar following an average -33k through Jan-Feb. That’s relatively healthy in April with a monthly profile that looks entirely consistent with adverse weather weighing in Jan-Feb before a warmer than usual March. April was more typical/cooler than average.

- Accommodation: 4k after 0k in Mar and 2k in Feb but these are typical changes for a sector that has been little net job creation in the past eighteen plus months (and is the only sector along with mining that is yet to recoup pandemic losses). It does at least rule out some new weakness amidst signs of foreign travel demand to the US waning.

- Retail trade: -2k in Apr after 22k in Mar and -4k in Feb. In the flip side to a particularly resilient transportation & warehousing category, this has seen a more pronounced pullback from strength in Dec/Jan. However, six of the past twelve months saw declines, all of which were larger.

- Away from the private sector, total government jobs increased by 10k in Apr after 15k in Mar, masking a third consecutive decline in federal payrolls (-9k in Apr after -4k in Mar and -13k in Feb) as weakness continues ahead of an expected sharper rise in layoffs in September with deferred resignations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA: Ontario Premier-'Can Take Tariffs To Zero If Trump Ends Tariff War'

Speaking on CNBC, Ontario Premier Doug Ford says "We would take tariffs to zero if Trump ended his tariff war. And we told him this". Adds that he wants to see Canada exporting more critical minerals to the United States. Ford: 'Lets get back to a USCA (US-Canada) deal, not a USMCA (US-Mexico-Canada) deal'.

- During the interview, Ford refuses to be drawn on the federal election, neither endorsing opposition Conservative Party of Canada (CPC) leader Pierre Poilievre nor PM Mark Carney's Liberals. Ford hails from the Progressive Conservative Party of Ontario, which ostensibly is ideologically linked to the CPC.

STIR: Effective Fed Funds Rate

- FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $264B

- Earlier Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.02), volume: $2.589T

- Broad General Collateral Rate (BGCR): 4.35% (-0.01), volume: $972B

- Tri-Party General Collateral Rate (TCR): 4.35% (-0.01), volume: $936B

- (rate, volume levels reflect prior session)

US TSYS: Goldman Revise Year-End Yield Forecasts Lower

Goldman Sachs note that their “economists' revised tariff baseline complicates the outlook for rates given the opposing impulses on growth and inflation”.

- They ultimately expect the “growth downside to dominate, resulting in lower yields and a steeper curve this year. We have revised our end of ‘25 2-Year and 10-Year yield forecasts to 3.30% and 4.00%, from 3.95% and 4.35%, respectively”.