PLN: No Reaction in PLN to NBP Decision, Focus on Presser Tomorrow

Dec-03 15:14

- Little to no reaction in EURPLN to either the rate decision itself or the policy statement given only a small minority of analysts had been looking for a hold (5 out of 32 surveyed analysts were expecting no change). The statement has offered little in the way of surprises – the cut is described as an “adjustment” while fiscal policy is again flagged as a risk to the inflation outlook – and as usual more focus will be on Governor Glapinski’s press conference tomorrow.

- For EURPLN, spot remains contained within a relatively narrow range. Key support is at 4.2230, the May 15 low, and while this level has been tested on a number of occasions, the cross is yet to make a sustained break below it. A convincing break would turn focus towards the 4.20 handle. First resistance is 4.2693, the Oct 10 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

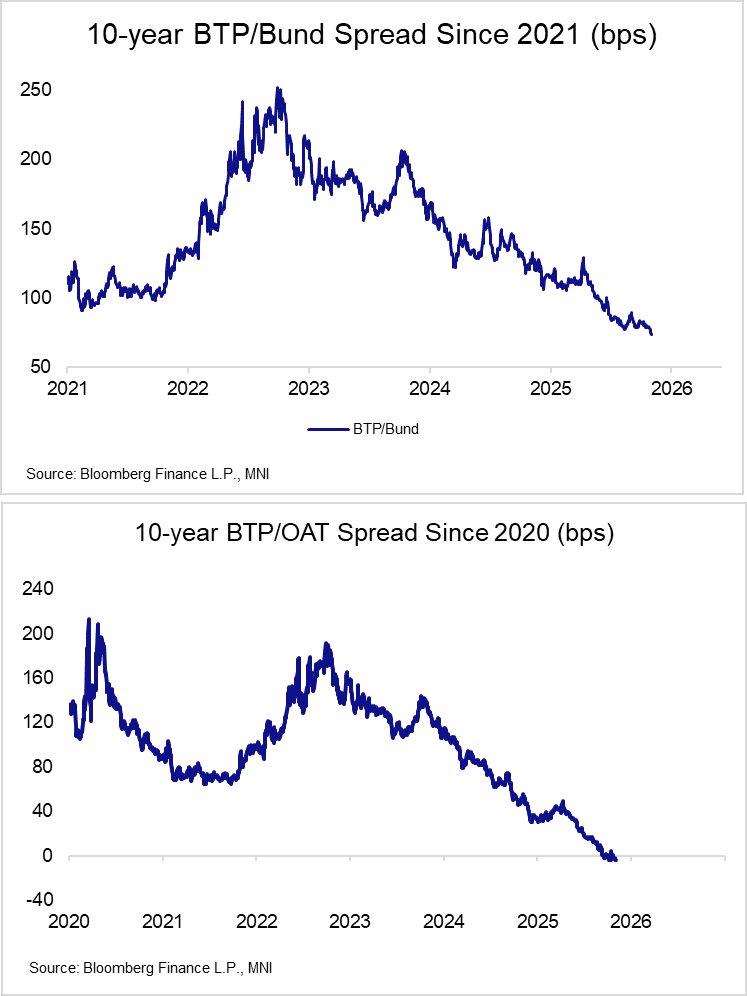

EGBS: Tightening Momentum In BTP/Bund Spread Persists

Nov-03 15:12

Tightening momentum in the 10-year BTP/Bund spread has persisted since October 23rd. The continued pullback in EUR rates volatility, alongside the relative attractiveness of BTPs versus OATs (from a political/fiscal standpoint) appear to be outweighing weak Italian growth fundamentals. The spread is at its lowest since early 2010, with downside attention now on the 70bps figure.

- EUR 3m10y swaption vol is another 0.5bps lower today at 50.8bps, the lowest since 2021. Last week’s heavy regional calendar is now in the rear-view, and did not bring any major surprises.

- Although OATs also outperform Bunds intraday, the 10-year OAT/Bund spread remains stuck in a 75-80bps range, with lingering political risks limiting narrowing episodes.

- The 10-year BTP/OAT spread has moved deeper into negative territory, now at -4.5bps. Meanwhile, the 30-year BTP/OAT spread turned negative for the first time on record last Friday.

- The next round of Italian supply is due next week, while France will sell LT OATs on Thursday. Note however there are E4.1bln of Italian coupon payments due this week.

US TSYS: Post-ISM Data React

Nov-03 15:02

- Treasuries continue to recover from this morning's deal-tied selling, trading mildly higher in 2s-10s after lower than expected ISM Mfg & Prices Paid data.

- Currently, the Dec'25 10Y trades +2.5 at 112-24 vs. 112-27 high, 10Y yield -.0155 art 4.0930%.

- The 10Y contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

MNI: US ISM OCT MANUF PURCHASING MANAGERS INDEX 48.7

Nov-03 15:00

- MNI: US ISM OCT MANUF PURCHASING MANAGERS INDEX 48.7

- US ISM OCT MANUF PRICES PAID INDEX 58.0