NETHERLANDS: No Confidence Motion In Schoof Cabinet Set To Fail

Stephan van Baarle, leader of the ethnic minority interest Denk party, has submitted a motion of no confidence in the demissionary cabinet of PM Dick Schoof. The prospect of the no confidence motion passing is nil. The leaders of the far-right Party for Freedom (PVV) and centre-left/environmentalist GreenLeft-Labour Party have both said they will not back Schoof's ouster, and combined with the members of the two remaining parties of gov't, this secures a majority for keeping Schoof in office.

- For months the Netherlands has been in a state of effective political paralysis. The withdrawal of Geert Wilders' PVV from the coalition in June left the Schoof gov't without a majority. Unable to gain requisite support, the PM went to the King to request a dissolution of parliament and snap elections. These are due on 29 October.

- In the interim, the minority three-party coalition sat as a 'demissionary' i.e. caretaker, administration that is tasked with the day-to-day running of gov't, but without the ability to pass 'controversial' legislation.

- On 22 Aug, the Christian democratic New Social Contract party withdrew from the demissionary gov't amid disagreements with the remaining two parties (the conservative People's Party for Freedom and Democracy and agrarian Farmer-Citizen Movement) on policies relating to Israel and Gaza.

- The liberal Democrats 66, left-wing Socialist Party, and centre-right Christian Democratic Appeal have called for a narrowing of the scope of legislation deemed 'controversial' for the demissionary cabinet, potentiall further restricting the gov'ts ability to pass bills or make decisions beyond immediate gov't operations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: Kazimir Doesn’t See Anything Forcing ECB To Cut As Soon As September

Bloomberg runs the below headlines from ECB’s Kazimir in an op-ed for the Slovakia central bank’s website.

- "*KAZIMIR: DON'T EXPECT ANYTHING FORCING ECB CUT AS SOON AS SEPT." - BBG

- "*KAZIMIR: UPSIDE INFLATION RISKS PERSIST, WARRANT VIGILANCE"

- "*KAZIMIR: TRADE DEAL `WELCOME NEWS,' CAN HELP LIFT UNCERTAINTY"

- "*KAZIMIR: MAJOR HIT TO LABOR MARKET COULD FORCE ECB ACTION"

- "*ECB'S KAZIMIR: PRE-COMMITTING WOULD BE A `FOOL'S ERRAND'"

This is the first update in over a month for Kazimir, with his latest two-sided comments broadly in keeping with his prior outlook. From Jun 24: “I belong to the governors who think we’ve reached our goal, that we are at the neutral range,”….“I personally would not touch rates before we’ll have a much clearer picture regarding trade-war scenarios.”

Sources pieces since last week's ECB meeting have touched on the high bar seen for the September meeting (for which there is currently just 4bp of cuts priced vs 10bp prior to Thursday's ECB press conference).

BONDS: Early Weakness Reversed, EGBs Lead

Core global FI markets reversed the Asia-Pac gap lower, with the inflation readthrough in the wake of the U.S.-EU trade deal and some ongoing questions surrounding trade between the two eventually outweighing any growth boost when it comes to bonds.

- Benchmark global equity index futures have eased back from Asia-London handover highs but remain comfortably firmer on the day.

- Bund futures as high as 129.74, bulls unable to test the 20-day EMA (129.97). Bears remain in technical control, Friday’s multi-month low (128.84) provides initial support.

- German yields are 2-3bp lower, belly and intermediates outperform. 10s hold below 2.75% after Friday’s brief move above.

- EGB spreads to Bunds little changed to 1bp tighter, aided by firmer equities.

- Gilts follow cues from peers with little in the way of meaningful UK news flow. Futures as high as 91.85, last +31 at 91.77. Initial resistance at the 20-day EMA (91.92) goes untested. Initial support comes in at the July 24 low (91.18).

- UK yields 1-4bp lower, curve flatter. 10s ~1bp wider vs. Bunds.

- ECB & BoE pricing little changed after the recent hawkish adjustments, 16bp of ECB easing showing through year-end, ~46bp of BoE cuts priced over the same horizon.

- Focus is on wider macro matters (any ongoing adjustment to the U.S.-EU trade deal and Sino-U.S. discussions in Stockholm).

- Note the BoE will sell GBP750mln of medium-dated gilts from its APF this afternoon.

- Plenty of EUR event risk as the week moves on, with the ECB’s inflation expectations survey (Tuesday), wage tracking data & (Wednesday), Eurozone GDP (Wednesday) & Eurozone HICP (Friday) all eyed.

EUROPEAN INFLATION: Expectations Not Swayed By Two-Sided Trade Deal Impacts

- As discussed, there has been little reaction in European front rates to weekend news on the US-EU trade deal with a 15% tariff on EU goods, having already been rumoured last week.

- There is still just 4bp of cuts priced for the Sept ECB, having adjusted from 10bp prior to Thursday’s ECB press conference and subsequent sources pieces pointing to a high bar to a cut next meeting. This had been ~ 12.5bp before headlines earlier in the week on the trade deal nearing.

- Recall Lagarde from the Q&A: "But one thing I will add to that is that the sooner this trade uncertainty is resolved – I think we use the word “resolved swiftly” – so the sooner it is resolved, the less uncertainty we will have to deal with, and that would be welcomed by any economic actors, including ourselves.”

- From a near-term domestic inflation angle, the deal has clearly reduced the prospects of EU retaliation, for which there had been growing support for more penal approaches. Nevertheless, details on the deal more broadly are sparse.

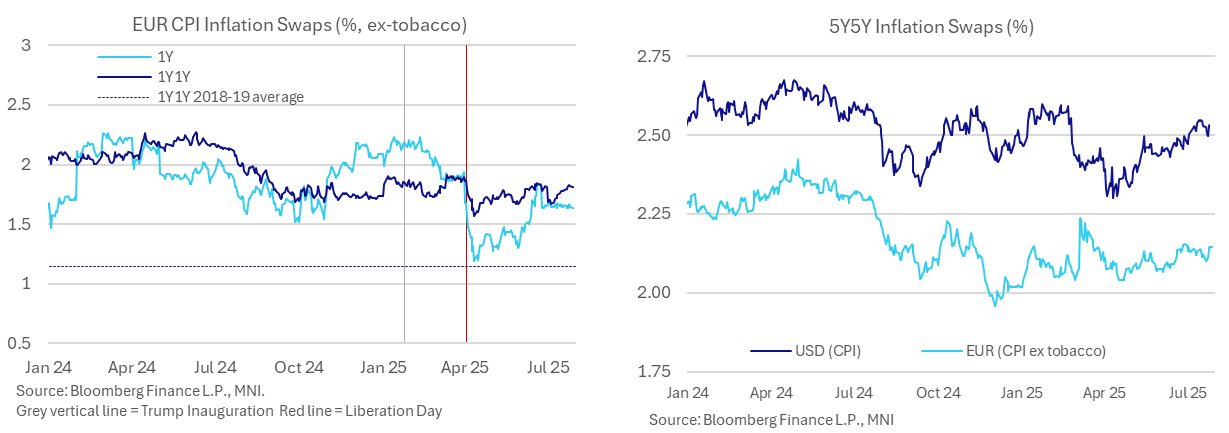

- For now, 1Y inflation swaps are just 0.5bp lower than Friday’s close, at 1.638% a little further off last week’s 1.668% but having broadly kept an unusually narrow range of 1.64-1.69% in July to date.

- 1Y1Y inflation swaps meanwhile at 1.81% are holding their trend climb seen over the month, close to recent highs having average close to 1.9% in the two weeks ahead of early April “Liberation Day” tariff announcements. Whilst still below 2%, as they have been since July 2024, they remain far higher than the tepid 1.1% averaged in 2018/19 pre-pandemic.

- Much further out, 5Y5Y inflation expectations at 2.144% are towards the high end of ranges over the past couple months but with little change over the weekend. This remains comfortably between the ~2.05% seen prior to EU and German fiscal announcements in early March after which they briefly surged to 2.22%.