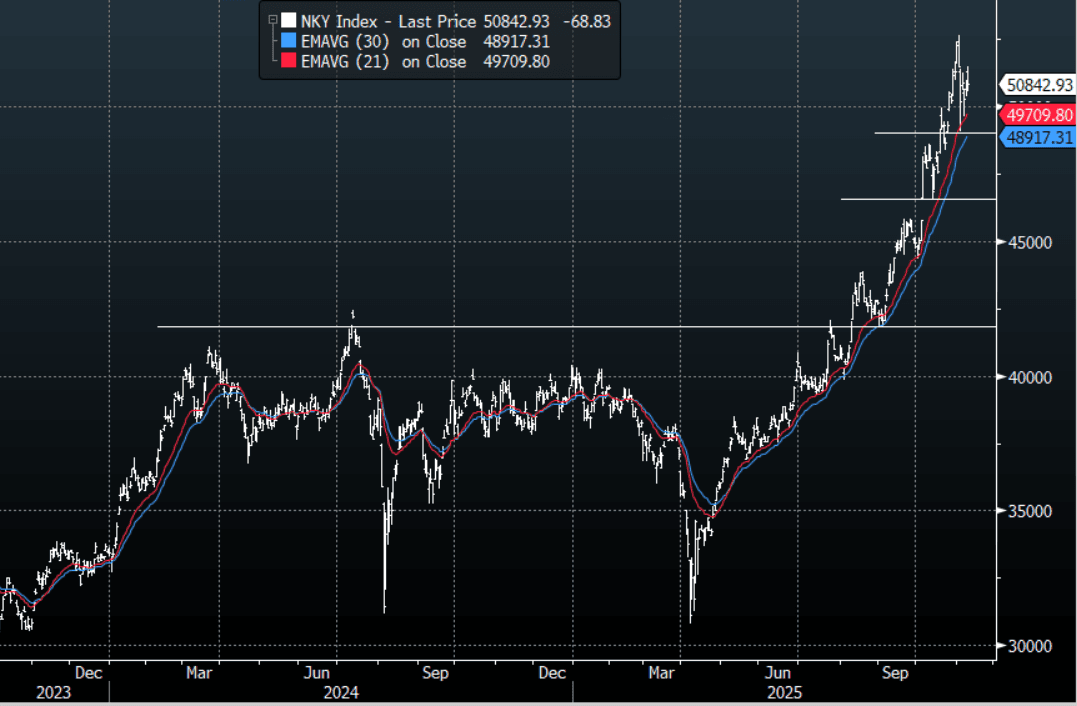

JAPAN: Nikkei(NHZ5) - Momentum Stalls Toward 51500, Look For Consolidation

The Nikkei(NHZ5) contract overnight range was 50770 - 51220, closing -0.14%. The Nikkei stalled towards the 51500 area yesterday and drifted lower off those highs. The Index has gone parabolic beginning in August/September, it looked to finally be putting in some sort of a top last week but with global sentiment improving again this price action could potentially continue into year-end. The support between 49000-49500 proved to be solid last week and while this continues to hold, I suspect the bulls will be around on dips as the focus turns back to the year's highs above 52 600 and a potential “Santa Rally.” This price action is pretty wild and the acceleration higher has been relentless but I do become wary when price action becomes parabolic, it's prudent to not fight the market when the price moves like this but history tells us when it does eventually stall the pullback could be just as brutal. Look for a 50500-51500 range on the day as it looks to consolidate these recent gains.

Fig 1: Nikkei Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

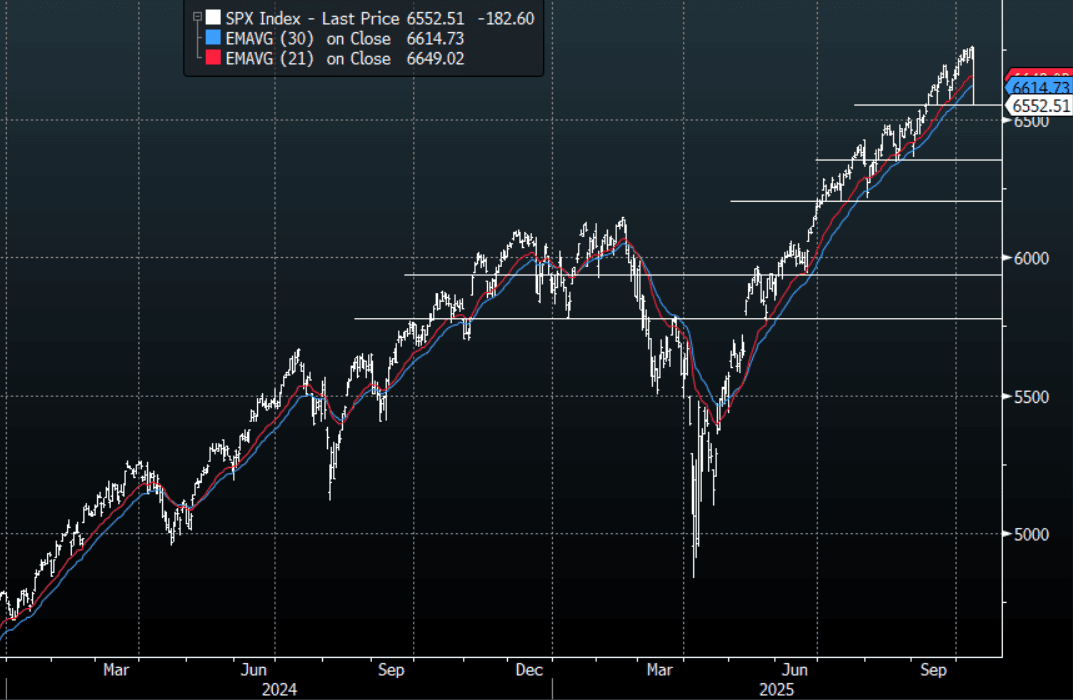

US STOCKS: S&P(ESZ5)- Gaps Higher On The Open On Attempts To Calm Market Worries

The S&P(ESZ5) overnight range was 6540.25 - 6806.50, SPX closed -2.71%, Asia is currently trading around 6665. The E-Mini’s have gapped higher on the open as the US attempts to lower the temperature and looks to set a more conciliatory tone as China played down the impact of its new controls, E-minis(S&P) +1.05%, NQZ5 +1.50%. The stock market looks to have put in a short-term top for now, we might see further retracement from Fridays lows around the 6500/6550 support as the market tries to latch onto anything positive. I feel that the damage done to leveraged accounts on Friday would make it difficult for the market to just move on from this and start making new all-time highs again. Personally I see very little chance of China changing its stance so I suspect those still very overweight will probably use any bounce to just lighten up positioning. Levels back toward 6700 and above are likely to be faded first up.

- Rush Doshi believes China will not back down on X, but they are at pains to stress the move is not a ban: “1 They're worried about the global reaction to their moves. So they stressed (twice) verbatim that these export control measures on rare earths are not prohibitions/bans. 2 They do not want to withdraw the controls. They also stressed these controls are their sovereign right. 3 They haven't announced a response to Trump's threats. They say only the boilerplate "they do not want to fight, but aren't afraid of fighting." Suggests they may not want to see further escalation.”

- “Bottom Line: Trump wants this regime withdrawn. Beijing won't do that, but is trying to reassure it won't implement it punitively. Obviously, that is not a credible promise on Beijing's part, and US and PRC positions are at odds.”

Fig 1: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

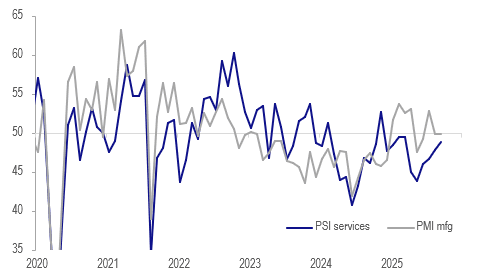

NEW ZEALAND: Services & Manufacturing Indices Signal Ongoing Weak Q3 Activity

The BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. The manufacturing sector stagnated in August/September, while services continued to contract but at a slower rate with September up one point to 48.8, highest since March. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

- The Q3 averages of the PMI and PSI show that there was some improvement in the quarter compared to Q2. Manufacturing rose 1 point to 50.9, slight growth, and services almost 3 points to 47.7, ongoing contraction.

- Forward-looking services orders rose to 51.4 from 47.8, the highest since November 2024. They continued to contract in Q3 overall at 48.6 but at a slower pace than Q2’s 45.5. Manufacturing saw an increase in orders in Q3 at 53.1 up from 49.5.

- Labour demand remained soft consistent with other data signaling a weak Q3 print on 5 November. September services employment fell to 47.8 from 48.7 with Q3 showing a further contraction in staffing at 47.6 (Q2 46.4). Manufacturing employment contracted too in the quarter.

NZ BNZ services vs manufacturing indices

Source: MNI - Market News/LSEG

JGB TECHS: (Z5) Bearish Trend Sequence Intact

- RES 3: 140.08 High Jun 13

- RES 2: 139.05 High Aug 4

- RES 1: 137.30 - High Sep 8 and key short-term resistance

- PRICE: 136.03 @ 15:44 BST Oct 10

- SUP 1: 135.61 - Low Oct 08

- SUP 2: 135.39 - 1.618 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

- SUP 3: 134.69 - 2.000 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

A bear threat in JGB futures remains present despite the intraday spike Monday. The contract pulled well off the intraday high, keeping the bias negative for now. The latest sell-off has also resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection. Key short-term resistance has been defined at 137.30, the Sep 8 high.