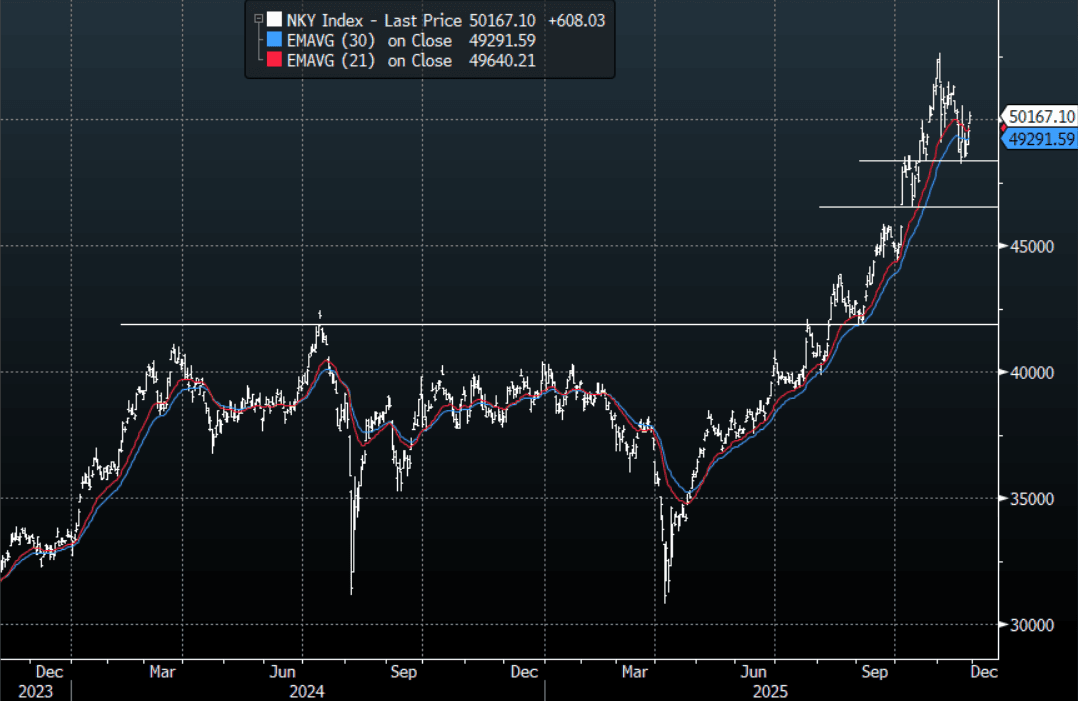

JAPAN: Nikkei(NHZ5) - Consolidates Above 50000, Look For Support Towards 49500

The Nikkei(NHZ5) contract overnight range was 49995 - 50195, Asia is currently trading 50120 +0.05%. The (NHZ5) contract drifted sideways overnight in a very quiet session with the US out. The Nikkei 225 technically remains in an uptrend while the support toward 48000 holds, albeit a very steep one. Can the Asian session build on this strong momentum in risk, it has come a long way very quickly but while this theme dominates then dips should continue to be supported. In the Asian session I suspect dips back toward 49400-49700 will now be supported initially. If the contract can sustain the move back above 50000 it will then target 50600-50800 first and then the 51500-51700 area.

- The Nikkei 225 Index Average True Range(ATR) for the last 10 Trading days: 1034 Points

Fig 1: Nikkei 225 Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Clears Resistance

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.825 @ 15:47 GMT Oct 28

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures rallied further Friday, building on gains earlier in the week posted off the poor Australian jobs data. This further signals that the recent move lower is a correction. Near-term resistance has been cleared into 95.780, the Sep 12 high. The clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg. On the downside, key short-term support to watch has been defined at 95.510, the Sep 3 low.

AUSSIE 3-YEAR TECHS: (Z5) Strong Weekly Close

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.530 @ 15:45 GMT Oct 28

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Aussie 3-yr futures briefly bounced on the US CPI print keeping focus higher despite the break of support last week. Short-term resistance at 96.615, the Sep 12 high, has been broken, with 96.780 is the next upside target. Clearance of this level puts markets at fresh multi-month highs. 96.280 marks next major support - but markets are some way off this mark now.

OIL: High Seaborne Oil Levels & Expected OPEC Output Rise Pressure Crude

Oil continued normalising on Tuesday following the 24 October high driven by news of increased US/EU sanctions on Russia. The fall in the Dallas Fed services index pressured prices. The market is refocusing on supply/demand fundamentals with OPEC’s monthly meeting on Sunday and another output increase probable while the IEA revised the expected 2026 market surplus higher in its October report. This is likely to provide a headwind to oil prices for some time.

- WTI fell 1.8% to $60.18/bbl after breaching $60 a number of times but breaks below were brief. It reached a low of $59.76, just above support at $59.64, 23 October low. It is now 2.9% lower in October and almost 4% off Friday’s high.

- Brent was down 1.8% to $64.47/bbl to be 2.4% lower this month. It touched $64.00 after the Dallas Fed data and then settled around $64.50. It held above initial support at $63.86, while the bear trigger is at $60.07. The expiry of contracts around $65 could add to market volatility, according to Bloomberg.

- OPEC increased its output target 137kbd at the last 2 meetings and another one is likely at the 2 November meeting as the group continues to unwind its previous 1.66mbd reduction.

- According to data from Vortexa there are currently 1.4bn barrels of seaborne oil, which the market is concerned will add to inventories. This is the highest since 2016 (Bloomberg).

- Bloomberg reported that US oil inventories fell a larger than expected 4mn barrels last week, after declining the previous week, according to people familiar with the API data, which may support crude when it resumes trading. Gasoline and distillate were both lower down 6.3mn and 4.4mn respectively. The official EIA data is out on Wednesday.