EM CEEMEA CREDIT: Nigeria (NGERIA): Supportive Stance from FinMin

Jan-15 15:13

(NGERIA; B3/B-pos/B) * Supportive for credit sentiment, valuations reflect the more favorable out...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Mar'26 2Y Buy

Dec-16 15:12

- +7,500 TUH6 104-12.125, buy through 104-12 post time offer at 0959:00ET, DV01 $298,000.

- The 2Y contract trades 104-12.62 last (+1.5)

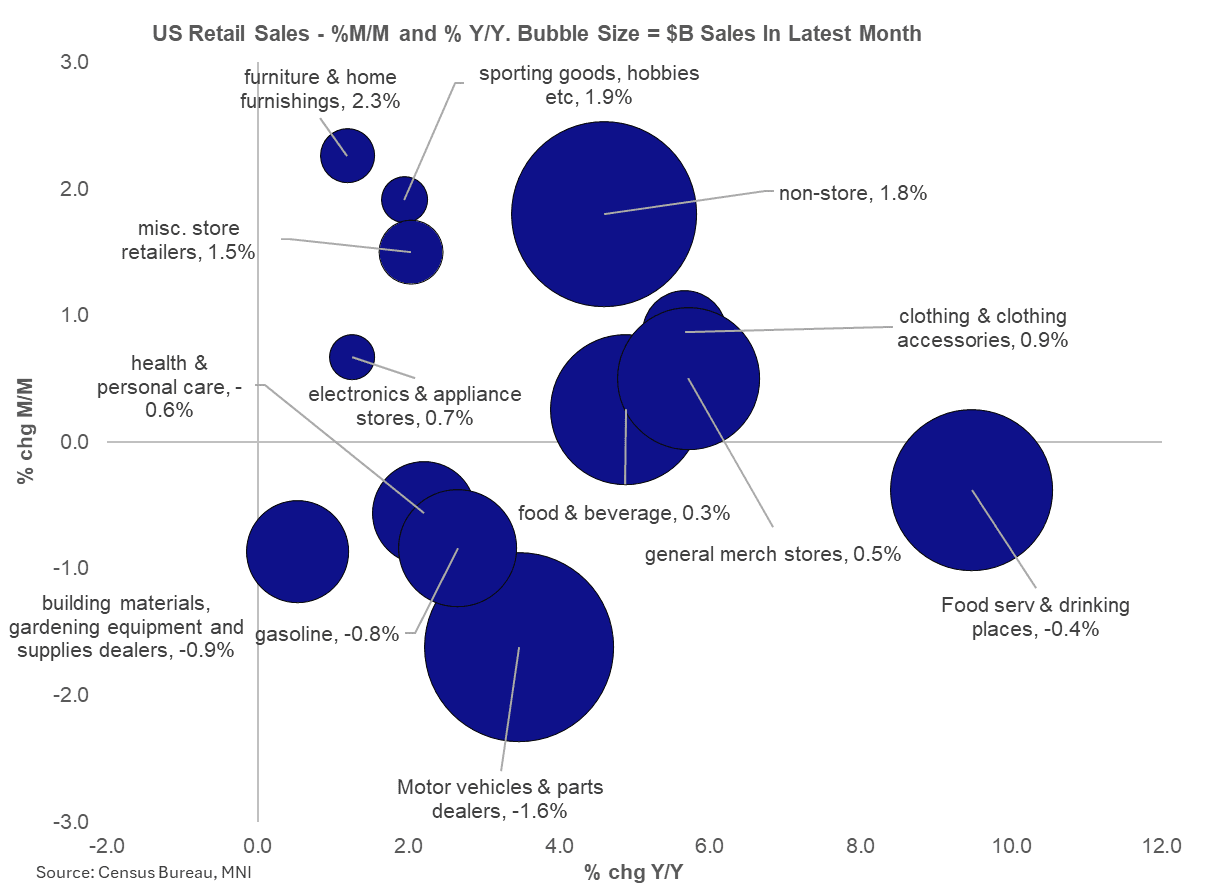

US DATA: Core Retail Sales Maintained Strong Momentum At Start Of Q4

Dec-16 15:10

Retail sales growth was flat in October after rising 0.1% prior, a little softer than the expected 0.1% gain - but core sales were significantly stronger than expected, implying strong retail momentum at the start of Q4.

- The Census Bureau's delayed report showed Control retail sales grew at the fastest monthly pace since June in October, with a 0.85% M/M gain (0.4% consensus) more than reversing September's unexpectedly poor -0.09%. Overall ex-autos sales grew by 0.4% (0.1% prior; 0.2% consensus), with ex-autos/gas up 0.5% (just under 0.0% prior, 0.4% consensus).

- The headline/core divergence was widely expected on account of soft gasoline (7-month worst -0.8% M/M) and auto (6-month worst -1.7%) sales, neither of which are included in the Control Group.

- Among other key categories, non-store retailers saw a 1.8% M/M jump after September's rare contraction (-0.4%) that had dragged on Control sales.

- In less good news, food services/drinking places sales (not in the Control Group) fell 0.4% for the worst performance since February. Indeed it was really only ex-Control categories that contracted M/M, with the other being building materials (-0.9%, 3rd drop in 4 months); the only Control Group included category to see a drop was Health and Personal Care (-0.6% M/M).

- The implied Control Group's 3M/3M annualized rise of 6.1% is a step down from 6.5% in the prior 2 months, but September's marked the best quarterly figure since Q1 2023 so this was still impressive.

- All of these should be taken with the caveat that they are in nominal terms, but at least nominal momentum appears to have been carrying through to November and December per "alternative" retail sales reports.

EQUITIES: Large Option Expiry in the SPX on Friday

Dec-16 15:10

The huge Option expiry in Notional Term for triple Witching (Friday) has gone up again on the SPX and other Indices/single Stocks:

- SPX: $4.30T vs $4.25T Yesterday.

- NDX: $171.02bn vs $167.13bn.

- Amazon: $24.96bn vs $24.75bn.

- Apple: $26.88bn vs $26.13bn.

- SX5E: €462.31bn vs €461.51bn.

- SX7E: €38.19bn vs €38.23bn.

- Dax: €52.56bn vs €52.56bn.