EM CEEMEA CREDIT: Nigeria (NGERIA): CB on Economic Outklook

Dec-31 09:55

(NGERIA; B3/B-pos/B)

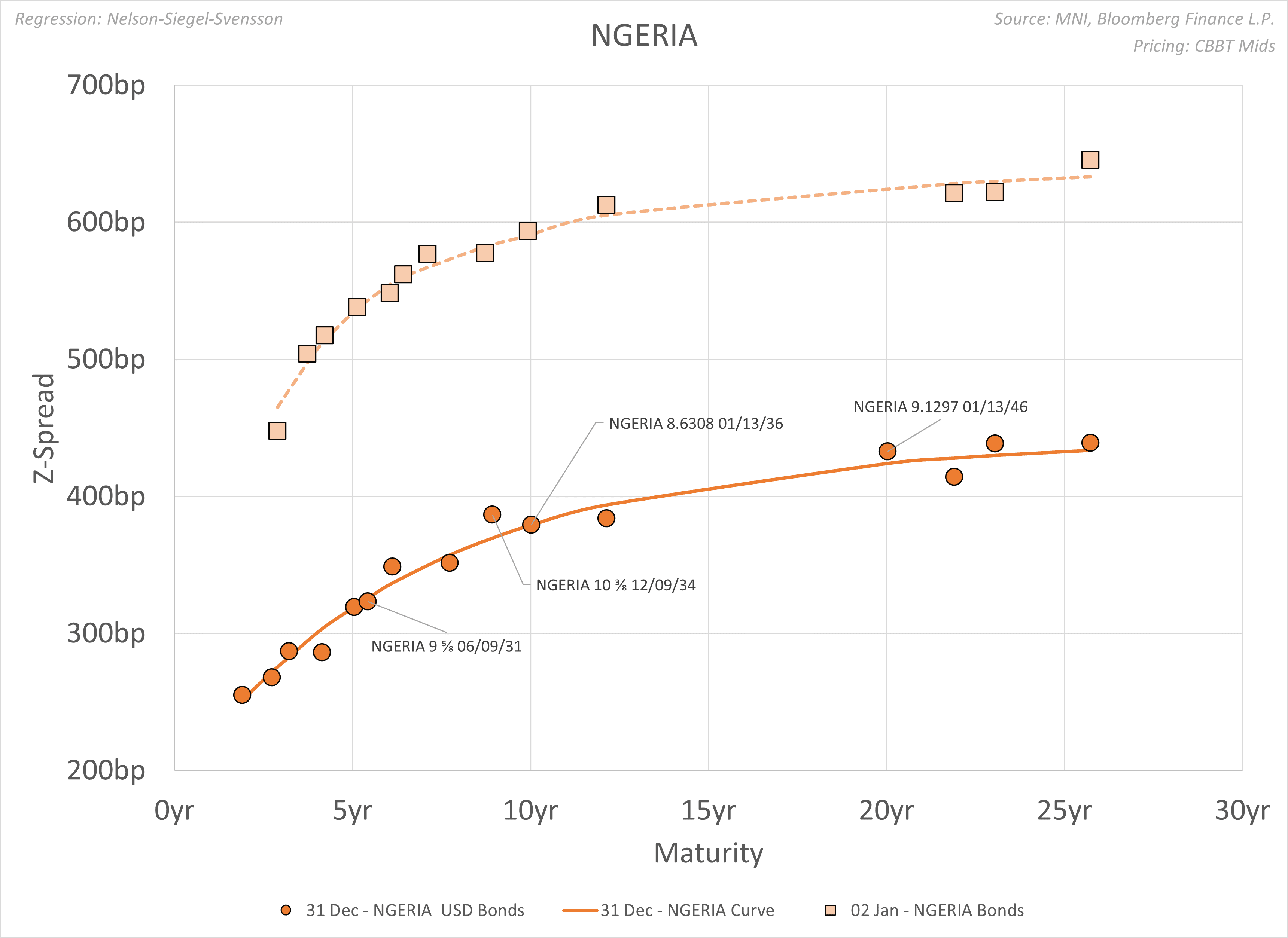

- Supportive for credit sentiment. Nigeria’s Central Bank has released its Macroeconomic Outlook for Nigeria. Whilst several risk factors contribute with varying degrees of uncertainty to form a high impact potential to derail the baseline scenario, from security challenges to unresolved geopolitical tensions, the outlook remains favourable. In secondary markets, the sovereign curve charts approx. 200bp tighter in 2025, with recently issued benchmark bonds NGERIA 36s and NGERIA 46s in line with the curve (see chart below).

- In terms of broad macroeconomic indicators, estimated real GDP growth is at 3.89% for FY25, on consistent strength in oil prod’n (+9.39%, avg prod’n +7.1% at 1.67mbpd) and contribution from non-oil related sectors (+3.70%, in evidence quarrying and coal mining). Projections for FY26 see growth at 4.49%, with a baseline assumption of 1.5mbpd of oil volumes and avg price of $55/bbl.

- On the inflation front, the data has finally reacted to strong policy intervention allowing for a more benign outlook. Projections show a downward trend, in line with scope for further easing of monetary policy stance, with headline inflation expected at sub 13% for ’26 and 10.75% for ‘27, coupled with transitional inflation targets at 16.5% and 13% for ’26 and ’27 respectively (range +/- 2%).

- In terms of monetary policy, in line with its objective to support sustainable economic growth, the CB availed itself with available tools to keep a tight focus on “maintaining monetary, price and financial system stability”. The earlier tightening of the base rate (started in Feb ’24, up 875bp to peak of 27.50%) coupled with conservative liquidity and cash reserve ratios, has been somewhat eased with a moderate 50bp cut to 27.0% post summer, together with a widening of the standing facilities corridor and lower cash reserve ratio. Broad money supply shows a 6.02% growth (to end-Oct.) suggesting a revamp in economic activity. Projections for FY26 indicate M3 at 8.12%. We view this as an important evolution.

- The banking system is assessed as stable, with conservative liquidity ratio (>60% vs 30% requirement) and adequate capital position (CAR at 11.60% vs 10.00% minimum) following an increase in minimum capital requirements earlier in the year (tiered increases in paid-up capital). Overall, we believe the sector shows room for improvement in terms of asset quality, with a spike in NPLs around mid-year ’25 following the withdrawal of pandemic-related regulatory forbearance, since trending lower to a 7.0% level, still higher than the benchmark prudential limit of 5.0% indicated by the CB.

- In terms of fiscal policy, fiscal revenues for FY25 sit at a provisional NGN34.82tn, up almost 22% y/y, on significant contribution from oil-related stable prices and higher prod’n volumes (NGN20.16tn, accounts for over 58% of total). Importantly, FY26 projections indicate an increase to NGN35.5tn on sustained oil rev’s (see baseline assumption mentioned above). Among non-oil rev’s (less than 42% of total), supportive fiscal reforms (Nigeria Tax Act 2025, effective Jan ’26) broadening the tax base are expected to see an increase in tax-related contributions, currently at 46% of total non-oil rev’s. in terms of govt expenditure, projections indicate a more stable y/y trend, with FY26 projections marginally lower at NGN47.64tn. The fiscal deficit for FY26 is estimated at just over 3% of GDP, with financing expected to raise a meagre NGN1.76tn from external sources, the bulk being via domestic sources (NGN7.02tn) and multi/bi-lateral project loans (NGN2.96tn).

- In terms of debt profile, we think total public debt remains moderate at NGN152.40tn, having declined to short of 34% of GDP (end-Jun) vs 38.8% at end-’24. FY26 projections show a marginal rise to 34.68%. Of total debt, external debt sits at an already modest 47% area, close to the target of 45%. We see this as supportive for credit.

- We note that the overall BoP surplus is estimated at USD5.8bn for FY25, a y/y decline. C/A surplus short of USD17bn marks a decline y/y, with trade surplus rising and services deficit lowering. FY26 projections see an increase to USD18.81bn, approx. 11% of GDP. Of note, external reserves’ estimates increased by some USD5bn y/y to just over USD45bn for end-Dec ‘25. For FY26, projections increase to just more than USD51bn, on expectations for higher oil-related public and private Dangote) contributions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Schatz Ratio Put Condor

Dec-01 09:53

DUF6 107.20/107.10/107.00/106.80p condor 1x1x1x0.5, bought for 1 an 1.25 in 6k.

STIR: Goldman Like Mid-'26 ECB Receivers To Hedge Core Position

Dec-01 09:51

ECB-dated OIS currently prices ~7bp of easing through September ’26, which represents the trough in the implied rate path.

- We have previously noted that Friday’s country-level November flash inflation data had little impact on ECB pricing, dampening the likelihood of a meaningful move around tomorrow’s Eurozone-wide HICP data.

- Ultimately, we believe that spot inflation may need to start undershooting the Bank’s target before markets become more sympathetic to the idea of another 25bp cut being added to the cycle.

- Still, several sell-side desks have outlined receiver-side plays as cheap hedges or good risk/reward plays in recent weeks.

- Goldman Sachs deem “current levels of low implied vol as attractive and see value in receivers focused around mid-2026 (June) ECB pricing to hedge core EUR rates shorts”, as “recent focus on disinflation - including from Chinese export competition - suggests risks to the 2026 ECB path”. This is even as they note that their “base case remains that the ECB will remain on hold and that EU cyclical conditions will drive core rates higher over time”.

EGB OPTIONS: Outright Bund Put buyer

Dec-01 09:46

RXF6 128.50p, bought for 35 and 35.5 in 3k.