EU TECHNOLOGY: Nexi Q125 Results

May-08 10:10

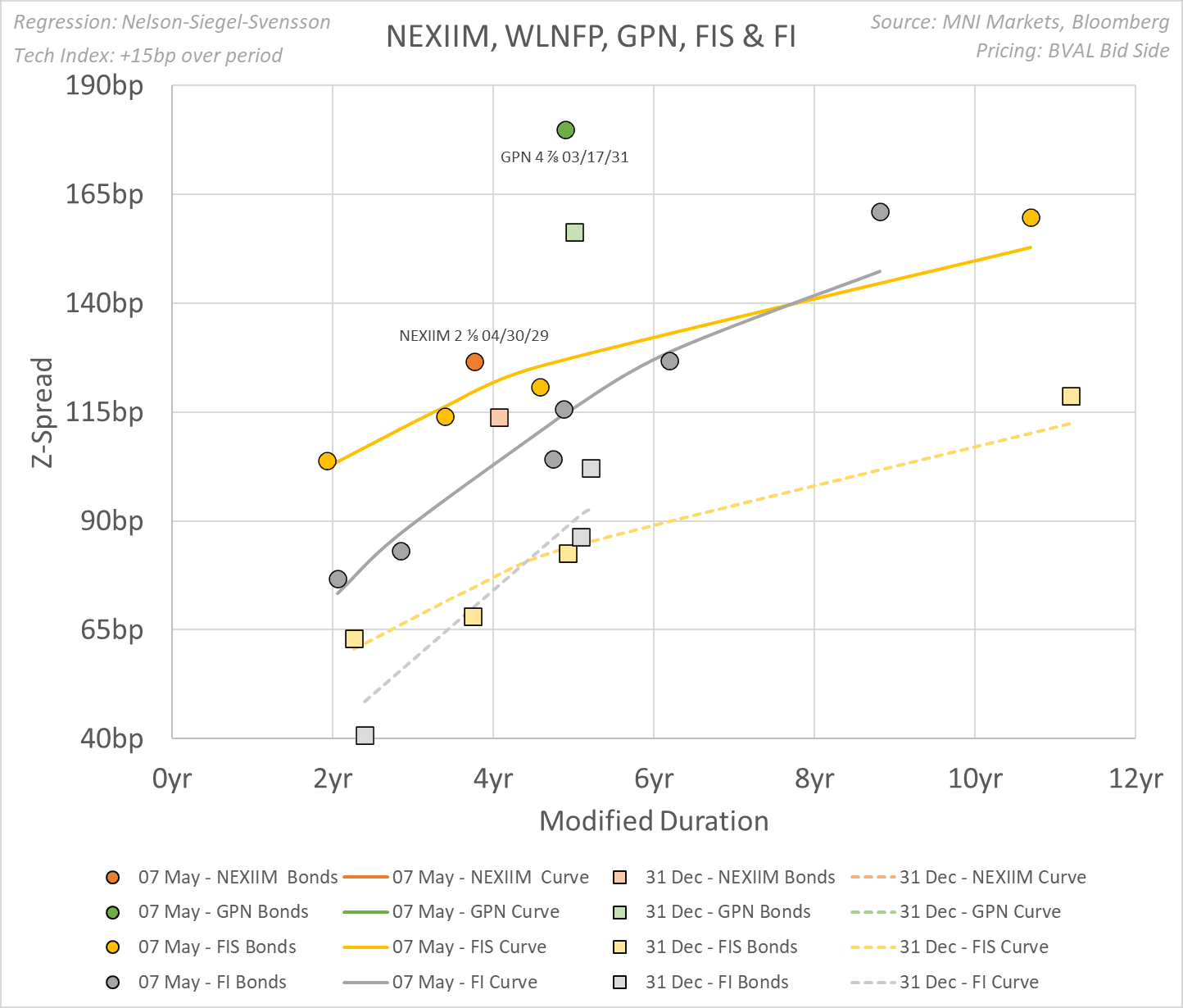

NEXIIM

Not a spread mover; Results broadly in line with leverage moving into the target range as the management affirms the tilt towards payouts. Some debt-relevant comments from the call below.

- Q1 revs €810mn (+4%, 1% miss) with MS/IS slightly soft at +5%/+3% and DBS in line at +1%.

- Q1 EBITDA €387mn (+7%, 2% beat). FY guidance affirmed. Comments on s/h tilt unchanged.

- Q1 NFD €4.8bn w/ reported leverage 2.5x vs. 2.7x at Q4 against the 2-2.5x target.

- Q: “When should we expect some news on the refinancing of the bond expiring next April?”

- A: “We will go when the market conditions are best for us to optimize our capital structure. So it's an opportunistic approach to funding. It's not something we need to do. We have until midpoint next year, if I remember correctly, for the bond to be reimbursed and at some point between now and then we'll try and pick the best time to do so. We won't wait for the last moment. I guess that's the only thing that I would say.”

- He was also asked a question on CoC language and covenants; clarified no covenants as docs are IG-styled. Asked about releveraging to “5x or more” (as an example) he clarified this was not a scenario under consideration though technically it was allowed by the docs.

- Asked about CoC language, he clarified the double-trigger i.e. CoC triggered by 50%+1 by a non-permitted party (i.e. Advent, Bain, H&F, CDP as per docs) with a ratings downgrade (docs; if two or more IG ratings, a DG that results in them no longer having two or more IG ratings i.e. at current ratings a downgrade from S&P or Fitch would trigger).

- On managing the cost of debt; “With regards to the cost of debt now, as you correctly noted, we are now benefiting from better kind of credit spread than we used to given our IG status. But at the same time, rates are now higher than they used to be. I think we will work to mitigate the impact on our cost of debt going forward.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FINLAND T-BILL AUCTION RESULTS: 7-month / 10-month RFTBs

Apr-08 10:05

| Type | 7-month RFTB | 10-month RFTB |

| Maturity | Nov 13, 2025 | Feb 13, 2026 |

| Amount | E845mln | E1.15bln |

| Target | E2bln | Shared |

| Previous | E685mln | E1.317bln |

| Avg yield | 2.13% | 2.1% |

| Previous | 2.27% | 2.29% |

| Bid-to-cover | 1.42x | 1.09x |

| Previous | 2.29x | 1.4x |

| Previous date | Mar 11, 2025 | Mar 11, 2025 |

Source: Bloomberg

EGB OPTIONS: Schatz put spread

Apr-08 10:04

DUK5 106.70/106.50ps, bought for 1.5 in ~11.9k.

US NFIB MAR SMALL BUSINESS INDEX 97.4

Apr-08 10:00

- US NFIB MAR SMALL BUSINESS INDEX 97.4