ARGENTINA: New Senate Members Sworn In as Negotiations with Regions Continue

- The Senate will hold a special session today to swear-in the 24 senators elected in the national midterms in October. In the coming days, President Milei is expected to issue a decree to summon Congress for extraordinary sessions that would run from Dec 10 to end February. He plans to present drafts of key reforms on Dec 9 and will make the 2026 budget proposal the first legislation introduced to the new Congress session.

- As noted, the government has been working hard to secure the support of the regional governors to advance its reform agenda. Today, Interior Minister Diego Santilli will host Jujuy Governor Carlos Sadir for negotiations. Local media reports this week suggest that the government would be willing to concede on several of the governors demands in exchange for their support on the 2026 Budget, labour reform and tax amnesty law.

- One of those key demands is that the national government releases a portion of the fuel tax to fund public works projects in the regions. Given the ongoing negotiations, the government has postponed the next pending fuel tax hike again, delaying it until January.

- In other news, the government has started a consultation period for an electricity and natural gas price subsidy scheme that will start in January, according to a resolution in the official gazette.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: Return Of The Base-Case Monetary Policy Report Forecast (2/2)

Additionally, despite sticky trim/median inflation, the BOC appears to be increasingly discounting these as measures of overall inflation pressures (see comments later in this preview from Deputy Gov Rhys Mendes, including an MNI interview). We suspect the BOC will continue to signal “broader range of indicators, including alternative measures of core inflation and the distribution of price changes across CPI components, continue to suggest underlying inflation is running around 2½%.”

- Overall, Macklem is unlikely to deliver any clear signals about future decisions at the press conference, keeping market pricing split between one further 25bp cut in the cycle vs no further easing.

- Judging from the last press conference, we wouldn’t be surprised to hear a few questions on the impact of fiscal policy, with PM Carney set to deliver a budget next week (though Macklem will probably defer answers until there is more clarity).

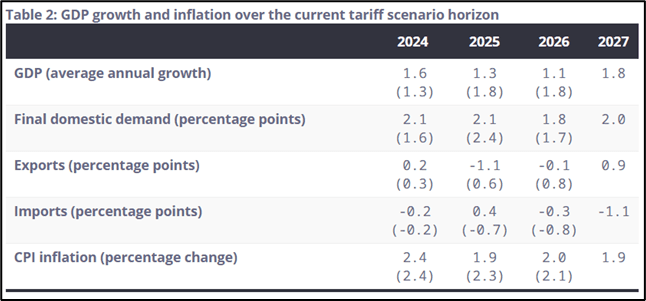

Monetary Policy Report: The BOC is set to release its quarterly Monetary Policy Report along with the decision. The most recent MPRs have eschewed central forecasts in favour of scenarios given elevated uncertainty over the US-Canada trade conflict, but officials have signaled the latest edition should mark the return to a normal forecasting framework.

- It’s difficult to gauge expectations for the MPR, especially since the comparison is with prior scenario-based editions, but vs July we would not be surprised by a slight downgrade to 2025 GDP growth (1.3% in the “current tariff” central-ish scenario in July) with downward for 2026 (1.1% in July). For inflation, the 1.9% 2025 forecast with 2.0% in 2026 should be little changed vs July’s current tariff scenarios.

- Given the understandable uncertainty over the outlook however, we think the MPR's findings will be relatively discounted as a policy steer.

BOC: BOC Set To Cut Despite Mixed Data, Opinions Split On Next Move (1/2)

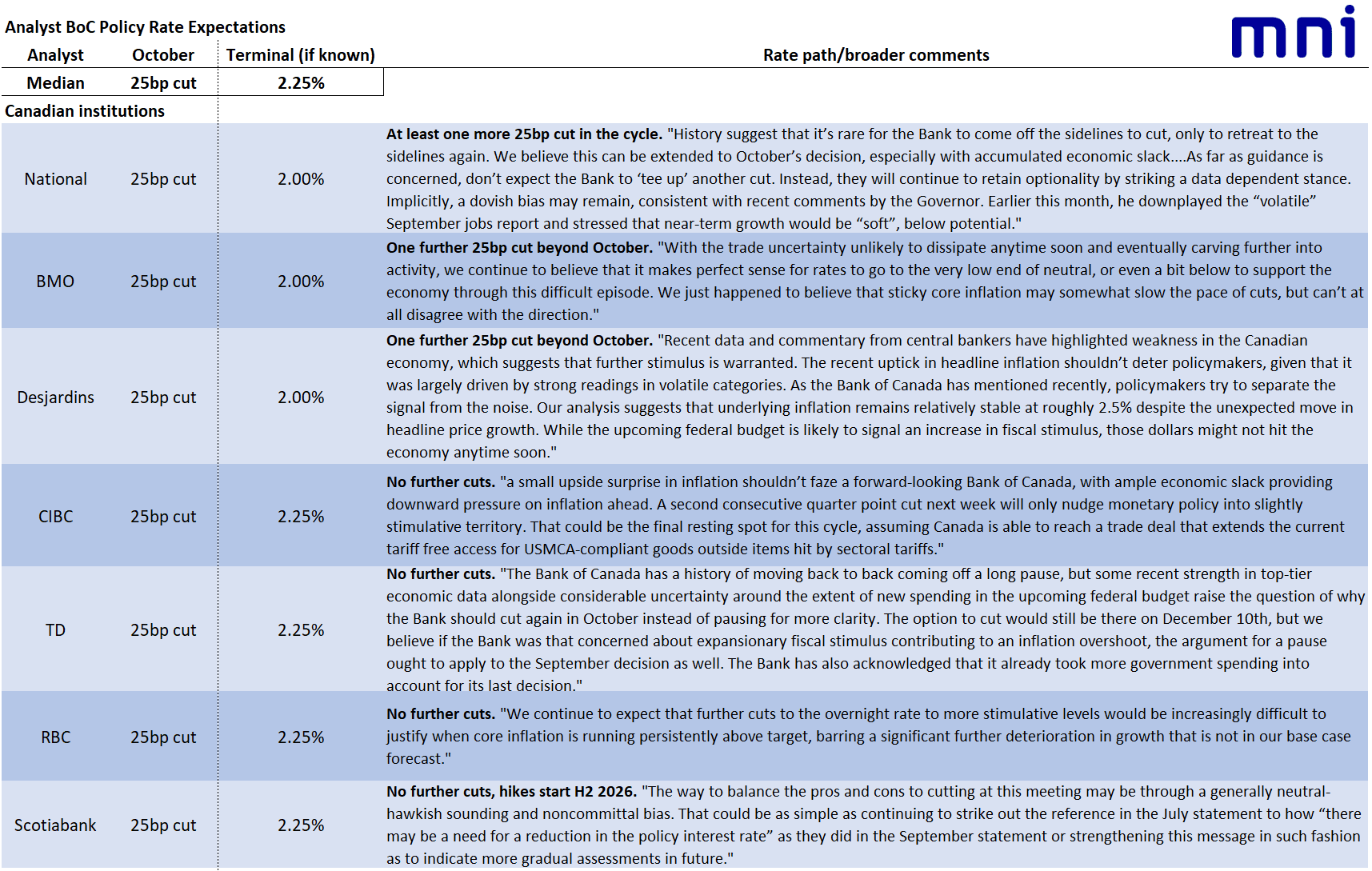

The Bank of Canada is set at 0945ET (1345UK) to announce a cut in its policy rate by 25bp for a second consecutive meeting, to an overnight policy rate of 2.25%. MNI's full preview is here

- Such a move is ~85% priced at this point, though another cut in the cycle isn't fully expected (~40bp through early next year).

- All Canadian bank analysts expect a 25bp cut today - the final holdout for a hold, BMO, changed its mind in a note on Friday. Summary table below. Meanwhile, we're aware of at least two non-Canadian bank analysts looking for the BOC to hold rates: BofA and Morgan Stanley. Overall the median expectation is for a terminal rate of either 2.00% (two cuts from today's level) or 2.25%, though opinion on timing of reaching those levels varies.

- The new 2.25% overnight rate would represent the bottom of the BOC's "neutral" estimate range (2.25%-3.25%), reflecting an environment in which economic slack has built amid the fallout from the US-Canada trade conflict but with trim/median inflation continuing to run at the high end of the BOC's target band.

- Overwhelming market and analyst conviction on a cut appears to understate risks of a rate hold, especially given the mixed inter-meeting data, with stronger-than-expected CPI and labour market data for September not enough to derail another cut amid increasingly muted private sector inflation expectations and a limited rebound in economic activity after Q2's sharp contraction.

- But Gov Macklem appeared to give the green light to a cut in recent comments, and a cut should be considered much more likely than a pause. As our Policy Team reported, Macklem sounded pessimistic about September's unexpectedly strong job gain, the major bright spot in economic data in recent weeks, saying it only reduced the net loss over the past three months, and mentioning auto sector layoffs. Macklem told reporters soft growth will add to slack and weigh on confidence. He said “The latest developments highlight that uncertainty remains elevated,” in response to MNI's question. Overall this Macklem appearance was considered a clear steer toward expecting an October cut.

EQUITY OPTIONS: Large Nokia Option following the NVIDIA news

Following Yesterday's news that NVIDIA was to invest $1bn into Nokia.

Today large upside call:

- Nokia (16th Jan) 8c, bought for 0.33 in 13.5k.

BoFA has also raised its price target to $8.07 from $4.64.