US CREDIT SUPPLY: NEW DEAL: Constellation Brands $500m WNG 10Y +125 Area

Oct-15 12:51

NEW DEAL: Constellation Brands $500m WNG 10Y +125 Area - BBG

• $500m WNG 10Y Fixed (Nov. 1, 2035) IPT +125 Area

• Issuer: Constellation Brands Inc (STZ)

• Format: SEC registered, domestic, senior unsecured

• Bookrunners: BofA, BBVA, JPM, WFS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK DATA: MNI UK Data Preview: September 2025 Release - CPI and Labour

Sep-15 12:50

For the full analysis report and sell side summaries click here.

- Both labour market data and CPI data will have already been released to MPC members this morning, and both data releases are important for future monetary policy despite markets pricing in only around a 1/3 probability of a rate cut this year (and not fully pricing a 25bp cut until April 2026).

- We think that both Governor Bailey and Deputy Governor Ramsden are very much focused on the labour market print (probably a little more so than inflation). Along with Breeden, all three members are likely needed on board in order for another rate cut this year to materialize.

- We think that the market focus will switch back to AWE private regular pay data. Both the median and mean estimate from the previews that we have read is that this will fall to 4.65%Y/Y in the 3-months to July.

- Headline CPI is expected to remain unchanged on a rounded basis at 3.8%Y/Y (from 3.83%Y/Y in July). The BOE's August MPR forecast is for 3.79%Y/Y while the median of the previews that we have read also looks for a 3.8% print. The focus will be on the unwind of air fares as well as how much higher food inflation climbs.

- We include summary tables for sell side views on the releases as well as including full summaries of analysis inflation views.

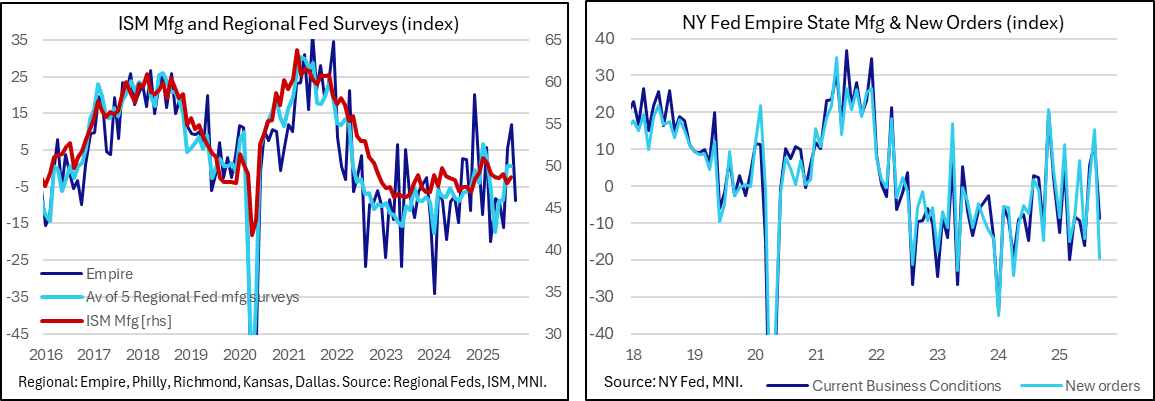

US DATA: Regional Fed Manufacturing Surveys Start Sept On A Weak Note

Sep-15 12:46

- The Empire Fed manufacturing survey saw surprisingly soft business activity in September, at -8.7 (cons 5) after 11.9 in August for its lowest and first negative print since June.

- As usual, this offers the first early look amongst the regional Fed surveys for September, collected Sep 2-9. It sees a sharp pullback for the often volatile survey after outperforming others in the summer.

- “New orders and shipments fell sharply”, down 35pts and 30pts to both their lowest since April 2024 respectively, including -19.6 for new orders.

- The summary from the press release (link) “Delivery times were steady, and supply availability worsened somewhat. Inventories edged lower for a second consecutive month. Employment held steady, while the average workweek declined modestly.”

- “The pace of input price increases was still elevated, though slower than last month, while the pace of selling price increases remained moderate.”

- “Capital spending plans continued to be soft. Firms expected some improvement in conditions in the months ahead, but optimism remained subdued. “ Indeed, the six-month ahead activity index eased to 14.8 having most recently peaked at 24.1 in July (for context, this saw -7.4 in April whilst it ended last year at 26.9).

US: Trump post on Rates

Sep-15 12:41

Donald J. Trump

@realDonaldTrump

“Too Late” MUST CUT INTEREST RATES, NOW, AND BIGGER THAN HE HAD IN MIND. HOUSING WILL SOAR!!! President DJT