EU CONSUMER STAPLES: Nestle: 3Q Results (x2)

Oct-16 12:08

(NESNVX; Aa3/AA-/A+) (equities +7.5%)

#MNI #Consumer

Strong 3Q sales alongside a one month in CEO who is announcing a 6%/16,000 job cut and adding phrases like "we will be ruthless in assessing our talent...we now need to be tougher linking compensation to performance...I'm a bit competitive" is likely helping sentiment recover from recent multi-year lows. Asides worth noting from the call:

- CEO on balance sheet: "we don't like to be at top end of 2-3x range and we are actively working on reducing our leverage"

- Net debt ended last year at CHF55b/2.9x, most of FCF this year likely to be used in dividend which it has assured will not be cut. But it notes FCF guidance for CHF 8b+ excludes €2.1b dividend it will get from Froneri (half owned by it, did a dividend recap recently).

- Notes capex discipline + WC efficiency's alongside water spin-off into potential partnership are sources to delever with next year.

- 4Q outlook: Despite a tougher comparison base (4Q24 +2.8%, v/m +1.7%), still confident volume/mix will remain positive as it builds momentum.

- On size of business (CEO): "my starting point here is that there are very significant benefits to scale...but we do need to become a more agile business...and in that context I'm going to look at everything...is this a growth category, is the returns profile attractive, are we positioned to win in it... across most of the portfolio the answer to these questions is yes …on the water and VMS strategic review it will continue and conclude in 2026"

- Water is rumoured for up to €5b valuation and is 3.5% of revenue/1.9% of profits. The VMS brands under review is smaller 1.3% of revenue and runs LSD margin (vs. group high teens).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

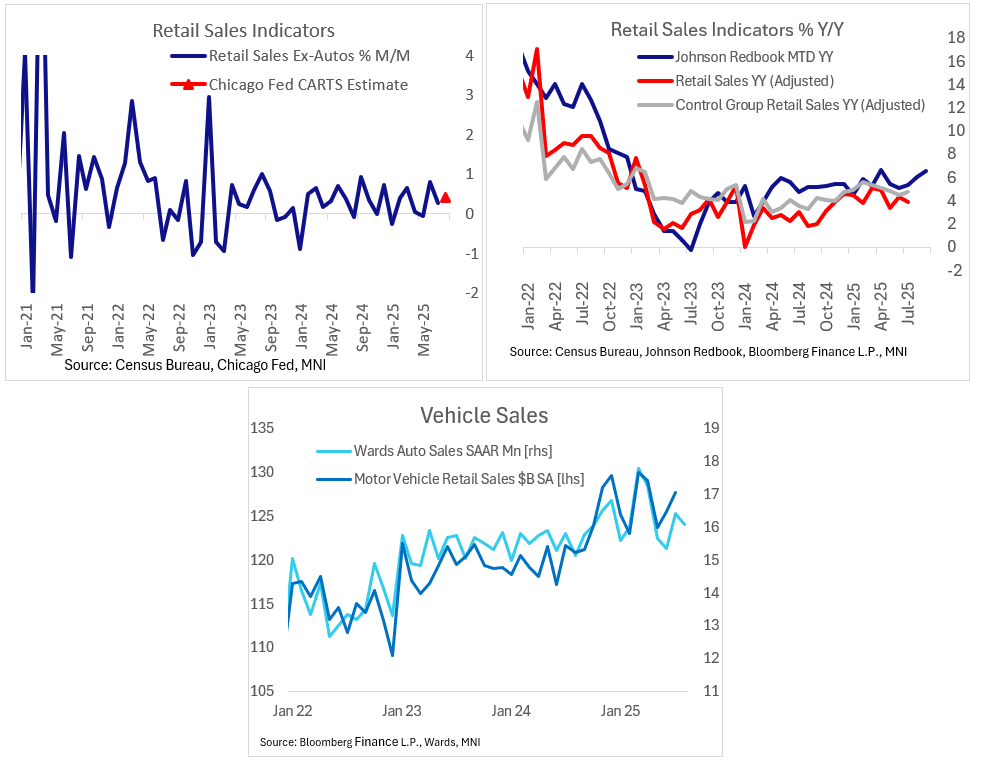

US PREVIEW: Retail Sales Growth Seen Weighed Down By Softer Autos

Sep-16 12:05

Advance retail sales growth (0830ET) is seen slowing in August to 0.2% M/M, from 0.5% prior, all on a nominal seasonally-adjusted basis - though this is largely driven by weaker auto sales.

- Indeed, the ex-auto and ex-auto and gas sales are seen at 0.4% M/M each (accelerating from 0.3%/0.2% prior). That accords with the Chicago Fed's CARTS estimate for ex-auto sales in the month of 0.4% M/M (0.1% M/M in "real" terms when adjusted for inflation).

- The expected pullback is explained largely by industry data: Wards Automotive Group reported 16.07M (annualized) light vehicle sales in August, a little under the 16.10M expected and a pullback from 16.41M in July.

- Otherwise, retail sales growth looked fairly healthy in then month, at least on a nominal basis (Redbook same-store sales rose 6.1% Y/Y in August).

- The GDP-input Control Group, which excludes auto sales among other categories, is seen relatively elevated at 0.4% (0.5% prior).

FED FUNDS FUTURES: Buying In Front End

Sep-16 12:02

FFX5 paper paid 96.125 on ~4.7K. Comes after FFV5 saw paper pay 95.945 on ~6.7K.

GILT PAOF RESULTS: The PAOF for the 4.375% Jan-40 Gilt was not taken up

Sep-16 12:02

- GBP750mln have been on offer.

- This leaves GBP34.113bln of the gilt in issue.