POLAND: NBP Say Inflation Developments and Outlook Justified "Adjustment"

Dec-03 15:05

Highlights from the policy statement:

- "Taking into account inflation developments and its outlook for the subsequent quarters, in the Council’s assessment, it became justified to adjust the level of the NBP interest rates"

- "Fiscal policy, recovery of demand in the economy as well as developments in wage growth, energy prices and inflation abroad remain risk factors for inflation outlook."

- "It can be estimated that also inflation net of food and energy prices decreased again."

- "Further decisions of the Council will depend on incoming information regarding prospects for inflation and economic activity."

Click here to see the full release.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-ISM Data React

Nov-03 15:02

- Treasuries continue to recover from this morning's deal-tied selling, trading mildly higher in 2s-10s after lower than expected ISM Mfg & Prices Paid data.

- Currently, the Dec'25 10Y trades +2.5 at 112-24 vs. 112-27 high, 10Y yield -.0155 art 4.0930%.

- The 10Y contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

MNI: US ISM OCT MANUF PURCHASING MANAGERS INDEX 48.7

Nov-03 15:00

- MNI: US ISM OCT MANUF PURCHASING MANAGERS INDEX 48.7

- US ISM OCT MANUF PRICES PAID INDEX 58.0

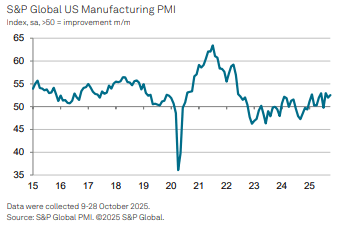

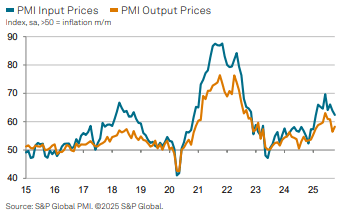

US DATA: PMIs Point To Robust Manufacturing As Inventories Climb

Nov-03 14:58

The manufacturing PMI was revised higher in the final October print to 52.5, leaving a larger increase from 52.0 in September but still below the 3+ year high of 53.0 in August. Finished goods inventories increased at their fastest since the data began in 2007, hinting at further volatility within national account data details ahead, whilst input cost inflation confirmed its softest since February.

- S&P Global US Mfg PMI: 52.5 (cons & flash 52.2) in Oct after 52.0 in September.

- The press release (in full here) points to similar drivers to the flash release of Oct 24 including input cost inflation at its softest since February, but goes into more detail.

- Domestic-led growth: “The performance of the US manufacturing economy improved again in October, with both output and new orders rising at stronger rates. However, growth was domestic led as new exports fell due to tariffs reportedly negatively impacting international trade.”

- Limited optimism but some eye onshoring gains: “Challenges in predicting future trade policy also served to limit confidence in the outlook, although some manufacturers expect to benefit in time from the reshoring of industrial output to the United States.”

- Lowest input cost inflation since February: “Tariffs remained a key source of higher input costs during October with latest data showing another round of historically elevated inflation – albeit the lowest since February. Selling prices were raised markedly in response, and to a quicker degree than September’s recent low.”

- Strong inventory build: “Stocks of finished goods rose to an extent not previously recorded since data

- were first available in 2007, while stocks of purchased inputs showed the second-largest rise seen for over three years. While stock building was partly fueled by expectations of rising demand, some factories also reported increased safety-stock building amid fears of supply shortages or to protect against further price rises, in turn reflecting the recent impact of import tariffs.”