US NATGAS: Natural Gas End of Day Summary: Henry Hub Rangebound

Jul-18 18:19

Henry Hub has dipped sharply into losses, after Baker Hughes data showed the US gas rig count jumping to its highest since March 2024. It has since regained ground to move back to rangebound.

- US Natgas AUG 25 unchanged at 3.54$/mmbtu

- US Natgas SEP 25 down 0.1% at 3.58$/mmbtu

- Baker Hughes US gas rig count: 117 (9) - up 16 rigs, or 15.8% on the year. The highest since March 2024

- Lower 48 natural gas demand is estimated down 0.83 bcf/d to 80.00 bcf/d today but above the 30-day average around 76.50 bcf/d, Bloomberg shows.

- The NOAA 6–14-day forecast shows stronger above normal weather expanding across most of the country, with a small pocket of below normal temperatures on the Pacific Coast.

- US domestic natural gas production marginally higher today at 108.34 bcf/d today, according to BNEF, the highest since May 23.

- Total feedgas flows to US LNG export terminals is down by 0.22 bcf/d to 15.51 bcf/d today, Bloomberg shows.

- The Golden Pass LNG project on the US Gulf Coast is set to receive a small of gas, according to data from BNEF.

- Elba Island LNG is set to bring on a small amount of gas today, July 18, according to Reuters

- The EU has backed a fresh sanctions package on Russia after Slovakia lifted its veto. It includes measures sanctioning the Nord Stream gas pipelines.

- Russian LNG exports may decrease 6-7% this year, according to Bloomberg.

- Asian spot LNG prices declined this week due to weaker demand and strong inventories, with buyers in South Asia on the sidelines as prices remain too high, Reuters said.

- Global LNG and gas prices could remain volatile into 2026, as the market is vulnerable to supply disruption, Bloomberg said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

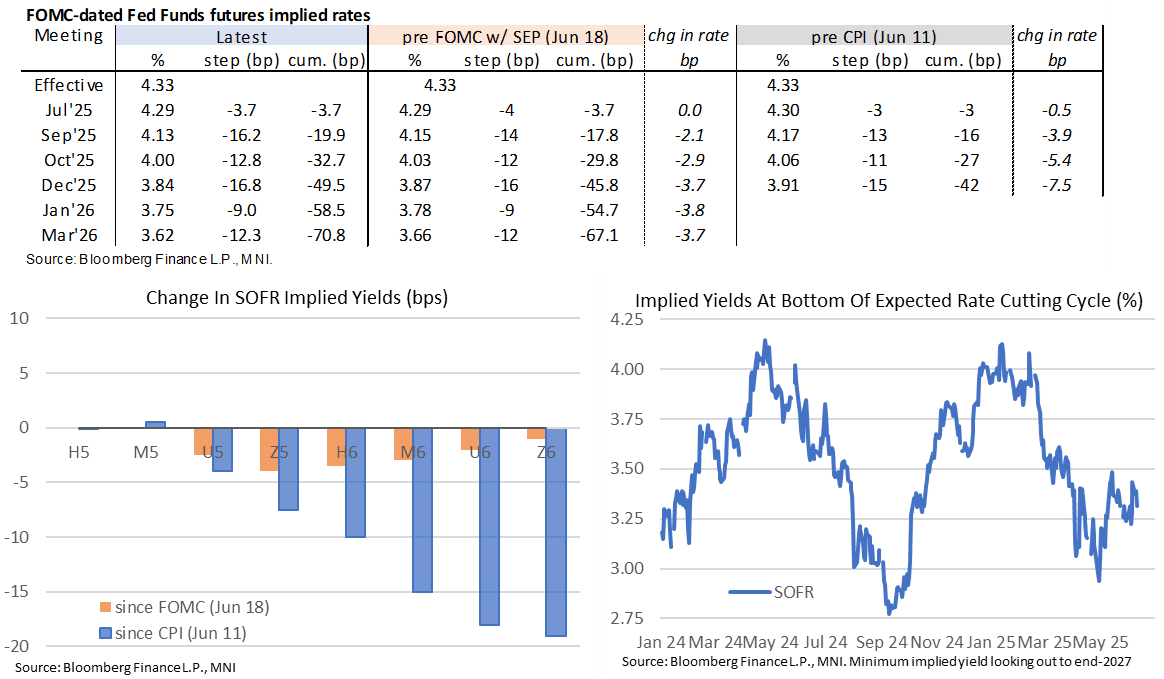

STIR: Fed Rate Path Reverses Day's Flattening On Dot Plot

Jun-18 18:19

- Fed Funds implied rates have slipped with the FOMC decision and SEP, with the unchanged median dot for 2025 pointing to two cuts in 2H25 catching most attention.

- 2026 and 2027 median dots were shifted higher however.

- It more than reverses a nudge higher in the 90 minutes ahead of the decision, with the Dec’25 3.5bp lower post-decision.

- Cumulative cuts from 4.33% effective: 3.5bp Jul, 20bp Sep, 32.5bp Oct, 49.5bp Dec and 58.5bp Jan.

- SOFR futures steepen, with SFRZ5/Z6 back to -0.62 (+0.01) vs -0.65 pre-decision.

- The implied terminal yield of 3.235% (SFRH7) sees little change post-decision, just 0.5bp lower for -4bp on the day. It points to ~110bp of cuts remaining for the cycle.

FOREX: Greenback Holding onto Moderate Declines Post-Fed Decision

Jun-18 18:19

- Some initial pressure on the greenback has been seen on the unchanged median dot for 2025, which still sees two rate cuts this year. USDJPY drops around 40 pips and in the process takes out a collection of short-term lows ~144.40 to a 144.34 low. Higher 2026 and 2027 dots see the dollar off its worst levels against the majors, as equities also give back their initial pop higher.

- For USDJPY, overnight highs broadly matched an initial resistance level of 145.46, Jun 11 high. On the downside, the May 27 low at 142.80 is the first notable support.

- AUD and NZD remain outperformers on the session, although this is largely a function of the steep risk sell-off late Tuesday, and the subsequent recoveries today.

- EURUSD holds back above the 1.15 handle for now, outperforming the likes of GBPUSD, which has struggled to hold above 1.3450 all session. Ahead of tomorrow’s Bank of England, weak sterling price action places attention on the next important support, which lies at 1.3350, the 50-day EMA.

FED: Dot Plot: Higher Shift In Outer Years Notable

Jun-18 18:16

The shift in the dot distribution vs March is below.

- It was a predictably close call going into this meeting between 2 cuts (3.9%) and 1 (4.1%) being signalled by the Dots for end-2025. The new Dot Plot shows 9 participants saw 1 or zero cuts, while the remaining 10 eyeing 2 or 3 cuts won the day. However, 7 of 19 members now anticipate no rate cuts this year. We think that the 8 in the 2-cut median probably reflects the core of the Committee including Chair Powell (with Gov Waller probably even more dovish at 3 cuts), but this wasn't far from signalling a higher end-year rate.

- More surprising was the shift higher in outer years, though again this was a close call.

- 10 of 19 now see a cumulative 75bp or less of cuts between now and end-2026, versus just 6 who saw such little easing at the March meeting. That said, there's one member who sees even more cumulative cuts by end-2026 than they expected before, and the median was close to remaining steady at 3.4%.

- For end-2027, there is a clearer shift with 6 dots at 3.1% now appearing in the 3.4% row. 11 of 19 members now see rates at 3.4% or higher by end-2027, versus 8 prior. This median is usually just a little above the longer-run dot, and perhaps this upward shift is reflective of the economic projections' medians showing that the 2% inflation target won't be hit by end-2027.

- On that note, none of the longer-run dot projections were changed vs March's meeting, a modest surprise given some had seen the median itself shifting up at this meeting (it remains at 3.0%).