FOREX: Muted G10 FX Trading Ahead Of NY, Kiwi Underperforming

G10 currency moves have been limited in pre-New Year APAC trading. The BBDXY USD index is flat and has traded in a narrow range of 1202.76/1203.48. The largest mover has been the kiwi with NZDUSD is down 0.2% to 0.5780 off the intraday low of 0.5776 but still higher overall in December.

- Aussie’s outperformance of kiwi continues helped by its more hawkish central bank and the recent rally in metals. AUDNZD is 0.2% higher at 1.1585, close to the intraday high at 1.1589. The pair is up 1.4% this month and with the RBNZ likely to be on hold through most of 2026 but the RBA possibly hiking, the upward pressure is likely to be maintained.

- Despite today’s decline in copper and silver prices, AUDUSD has held steady around 0.6696 and traded in a narrow of 0.6691/0.6701 with breaks above 0.6700 very brief.

- USDJPY is up 0.1% to 156.52, close to the intraday peak, but continues in the range around 156.00 seen since it peaked at 157.78 on 19 December. There has been no news out of Japan today and the equity market is shut.

- European currencies are slightly weaker against the greenback with EURUSD at 1.1741 and GBPUSD 1.3463. EURGBP is flat at 0.8722 after reaching 0.8727.

- Equities are mixed with the S&P e-mini down 0.1% and Hang Seng -1.0% but TAIEX up 0.9%. Copper is down 1.2% and silver -5.0%, while iron ore remains around $105.50-106/t. Oil prices are up slightly following news of a Ukrainian strike on a Russian refinery. WTI is +0.2% to $58.04/bbl.

- Later US jobless claims print. European stock markets are either closed or have early finishes, which includes the UK.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

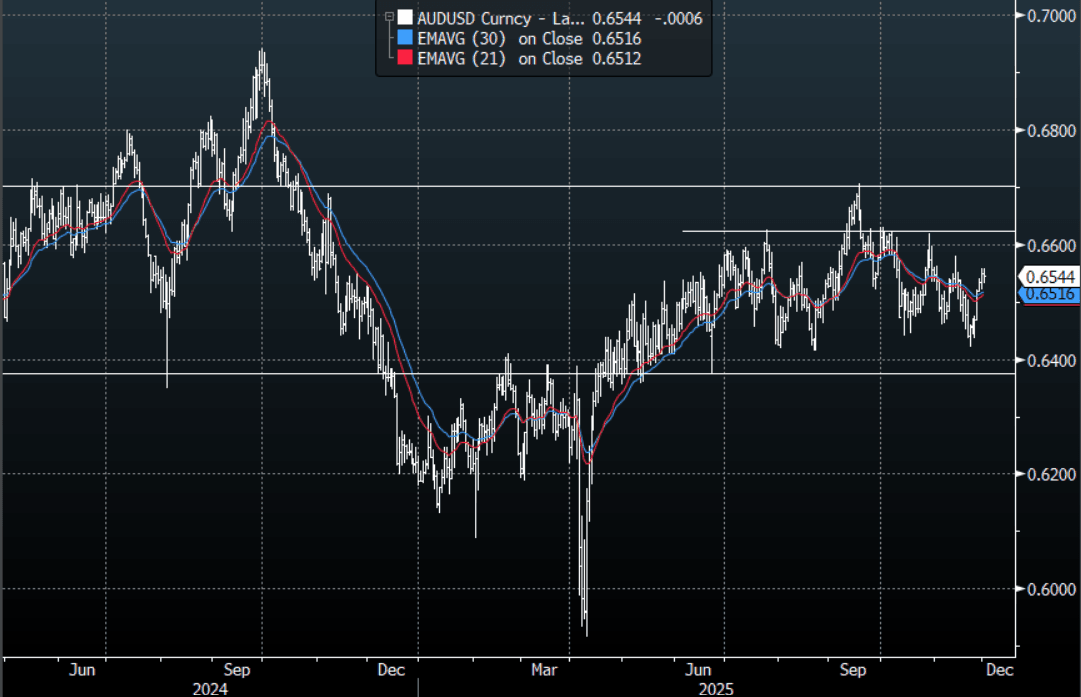

AUD: AUD/USD - Treads Water Around 0.6550, Ignores Risk-Off For Now

The AUD/USD has had a range today of 0.6531 - 0.6557 in the Asia- Pac session, it is currently trading around 0.6545, -0.10%. The AUD/USD has had a subdued session considering the risk-off start to the week. Asia has broadly sold the USD as USD/JPY trades lower, but if this risk-off start to the week turns into something more I would look for the USD to potentially bounce against risk currencies. The AUD is consolidating around 0.6550 just below the pivot toward 0.6550-60 within its wider 0.6350-0.6700 range. On the day, I would not be surprised to see the AUD/USD drift back toward the 0.6490-0.6510 area on the back of this shaky start to the week.

- MNI POLICY: RBA Sees Balanced Risk, Despite Monthly CPI Shock. The Reserve Bank of Australia continues to view the 3.6% cash rate as somewhat restrictive, despite recent strong inflation data, including October’s monthly print, which policymakers will largely look through, MNI understands.

- MNI AU - Wages Bill Continues Rising, Q3 Inventories Flat: Q3 Australian company profits were weaker than expected posting a flat outcome on the quarter after Q2’s sharp fall of 2.6% q/q and are now up only 1.1% y/y (strongest since Q1 2023 though). Inventory volumes fell 0.9% q/q which is likely to be a small detraction from Q3 GDP growth currently expected to rise 0.7% q/q and released on Wednesday. The net export and public demand contributions are released Tuesday.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD445m), 0.6425(AUD444m), 0.6550(AUD521m). Upcoming Close Strikes : 0.6490(AUD710m Dec 4) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 39 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

PRECIOUS METALS: Silver Continues Outperformance, US ISM Later

Continuing Friday’s pattern, silver is outperforming gold in Monday’s APAC session. Silver benefits from high physical demand and the market is currently tight. Prices are up 1.3% to $57.22/oz after an intraday high of $57.864, a new record, and 5.8% rise on Friday. In comparison, gold is flat today at $4238.7/oz reaching $4256.48 earlier and rising 2.0% on Friday. Both metals have found support from increased Fed rate cut pricing which is now at 23pp for the 10 December decision. Yields and the US dollar are little changed today.

- Silver moved above the bull trigger at $54.480 and three other resistance levels including $56.153, a Fibonacci projection, confirming a resumption of the primary uptrend.

- Bloomberg reported that silver inventories in the Shanghai Futures Exchange have fallen to their lowest in almost 10 years.

- However, Pepperstone Group believes that silver is being driven by “speculative flows” which given the substantially lower volumes than gold is creating the recent large price moves.

- Equities are mixed with the S&P e-mini down 0.7% and Nikkei -1.8% but Hang Seng is up 0.8% and SE Thai +0.8%. Oil prices are higher with WTI +1.6% to $59.50/bbl. Copper is up 1.5%.

- Later US November manufacturing ISM/PMI, UK October lending and European November manufacturing PMIs are released.

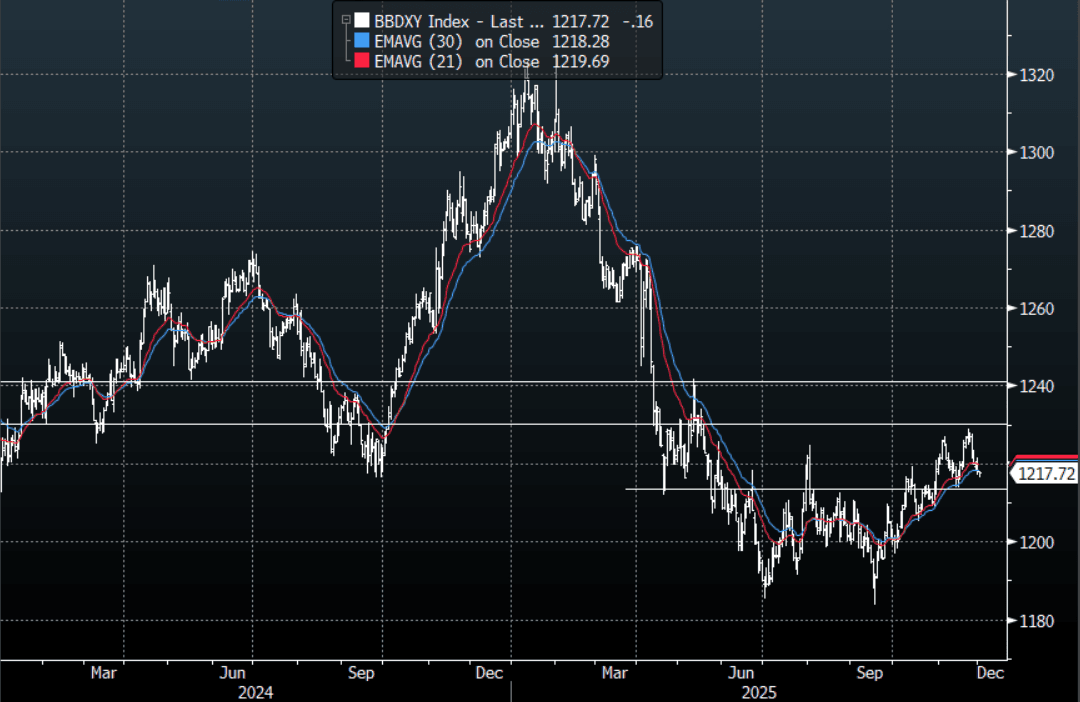

USD: BBDXY - USD Moves Lower In Asia, Dragged Down By USD/JPY

The BBDXY range Friday night was 1217.18 - 1221.55, Asia is currently trading around 1217, -0.05%. Risk has turned very quickly to start the week in Asia thanks to a combination of poor Chinese PMI’s over the weekend and Japanese yields continuing to extend higher as the market prices in a potential December BOJ rate hike. The USD moved lower initially as Asia tends to follow the moves seen in USD/JPY, I suspect we might see this start to differentiate once London comes in. On the day I will be watching to see if the USD can bounce against risk currencies should this risk-off start to the week expand on its initial moves. On the day resistance is back towards the 1222-1224 area where sellers should remerge initially, a sustained break back above here and the market would again turn its focus to the pivotal 1230-1240 area.

- The BBDXY Average True Range for the last 10 Trading days: 366 Points

Fig 1: BBDXY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P