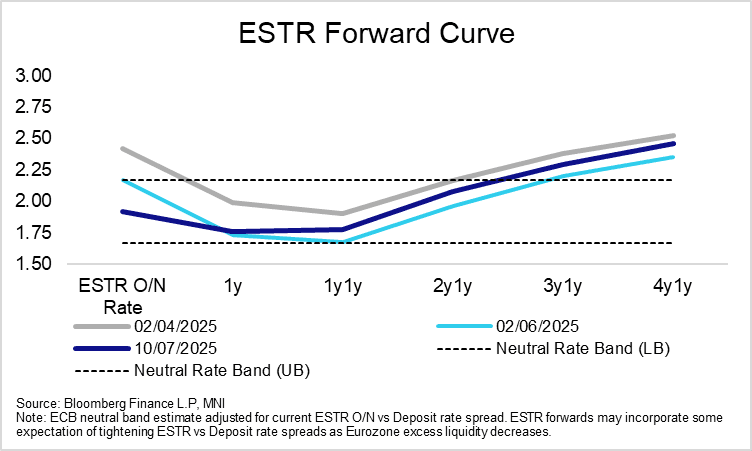

STIR: MT ESTR Forward Rates Converging With April 2 Levels

Increased medium-term German/EU fiscal spending warrants a steeper curve and some implied probability of ECB rate hikes going forward - a reminder that the June 24th German budget saw larger-than-expected deficit projections. However, several analysts believe there are downside risks to the announced investment figures, which may limit the overall growth impulse in the medium-term. While front-end ESTR rates remain comfortably below April 2 levels (i.e. pre-Liberation Day but after the initial German fiscal announcement in early March), medium-term forward rates (e.g. 3y1y, 4y1y) have started to converge back to these levels.

- In an interview released to the MNI Policy Team yesterday, ECB’s Holzmann unsurprisingly said rates should be kept on hold going forward. Perhaps more notably though, he suggested that the NATO commitment to spending up to 5% of GDP on defence and military infrastructure in coming years need not lead to higher eurozone inflation if the money is spent wisely and spare cross-border capacity utilised effectively.

- In the very near-term, ESTR ECB-dated OIS are little changed from yesterday’s close, still consistent with one more 25bp cut to a terminal deposit rate of 1.75%.

- Euribor futures are little changed through the blues. Early dovish flow has included a 98.25/98.37/98.50/98.62 call condor, now bought in 25k today. Z5 currently trades at 98.195.

- ING note that EUR rates markets do not seem “overly concerned about the ongoing trade tensions and that the potential upside and downside for rates is limited”. They think “the next move in euro rates may have to come from the data”.

- Today’s regional calendar includes May industrial production data from Italy, with scheduled appearances from ECB’s Cipollone, Escriva and Villeroy.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Jul-25 | 1.916 | -0.3 |

| Sep-25 | 1.806 | -11.3 |

| Oct-25 | 1.774 | -14.5 |

| Dec-25 | 1.685 | -23.4 |

| Feb-26 | 1.669 | -25.0 |

| Mar-26 | 1.644 | -27.5 |

| Apr-26 | 1.649 | -27.0 |

| Jun-26 | 1.653 | -26.6 |

| Source: MNI/Bloomberg Finance L.P. | ||

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Short Term Resistance In Euribor Contracts Intact

Light dovish repricing in EUR STIRs following the softer-than-expected UK labour market report and early weakness in global equities, but last Friday/yesterday’s highs continue to cap topside across the Euribor strip.

- Euribor futures are up 0.5 to 3.5 ticks through the blues, with ERZ5 once against finding resistance at 98.220, and ERH6 similarly being contained by 98.240.

- ECB-dated OIS price 25.5bps of easing through year-end (vs 24.5bps at yesterday’s close), with 15bps priced through September.

- Yesterday evening, ECB’s Holzmann provided more colour on his decision to dissent at last Thursday’s meeting. However, he still noted that “if the economic situation takes a turn for the worse there could be more rate cuts”.

- In our view, this highlights that the Governing Council still leans dovish on net, and the risks are skewed towards another cut this cycle.

- Today’s regional calendar includes the June Sentix survey and commentary from Holzmann and Rehn. Villeroy has noted that policy and inflation is in a “favourable zone”, but this doesn’t mean the ECB is static.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Cut Adjusted Effective ESTR Rate (bp) |

| Jul-25 | 1.894 | -2.6 |

| Sep-25 | 1.771 | -14.9 |

| Oct-25 | 1.738 | -18.3 |

| Dec-25 | 1.666 | -25.5 |

| Feb-26 | 1.653 | -26.7 |

| Mar-26 | 1.646 | -27.4 |

| Apr-26 | 1.650 | -27.1 |

| Jun-26 | 1.660 | -26.0 |

| Source: MNI/Bloomberg Finance L.P. | ||

GILTS: Bull Steepening After Labour Market Data Drives Dovish Repricing In STIRs

Gilts rally on the back of the labour market data (softer-than-expected wages and payrolls readings), which punctuated ongoing downside risks to BoE wage growth projections and promoted a dovish repricing in STIRs.

- Gilt futures trade through Monday & Friday highs, rallying as far as 92.49 before fading back to 92.40.

- The short-term bullish impulse remains intact in the contract.

- Initial resistance is located at the June 5 high (92.63), which protects a Fibonacci resistance point (92.79).

- Yields 4.5-6.0bp lower, curve bull steepens.

- 2s10s last 63bp, recent forays below 60bp have been short-lived and limited in scope.

- 5s30s back above 120bp after 3 daily closes below that level.

- GBP STIR pricing holds around levels flagged ahead of the gilt open. 46bp of cuts priced through December, with the next 25bp step almost fully priced come the end of the September MPC.

- We remain on the lookout for the launch of the syndication of the DMO’s new long 15-year 1.75% Sep-38 index-linked gilt.

- Broader domestic focus moves to the release of the government’s spending review, due tomorrow. More colour on that event can be found in our latest Gilt Week Ahead.

- Elsewhere, Wednesday will see BoE’s Saporta speak on monetary policy implementation. Our Gilt Week Ahead provides greater colour on that address as well.

FOREX: FX Exchange traded Roll pace

- As expected, some Desks have taken advantage of the steadier two way moves in Cross assets to start rolling their CME FX positions into September, the June Expiry is on the 16th June.

FX ROLL PACE:

- EUR: 20% vs 12% Yesterday.

- GBP: 24% vs 18%.

- JPY: 44% vs 35%.

- CHF: 30% vs 19%.

- CAD: 22% vs 14%.

- AUD: 22% vs 10%.

- NZD: 30% vs 8%.