US DATA: Mortgage Applications Fade Latest Dip In Mortgage Rates

Sep-03 11:23

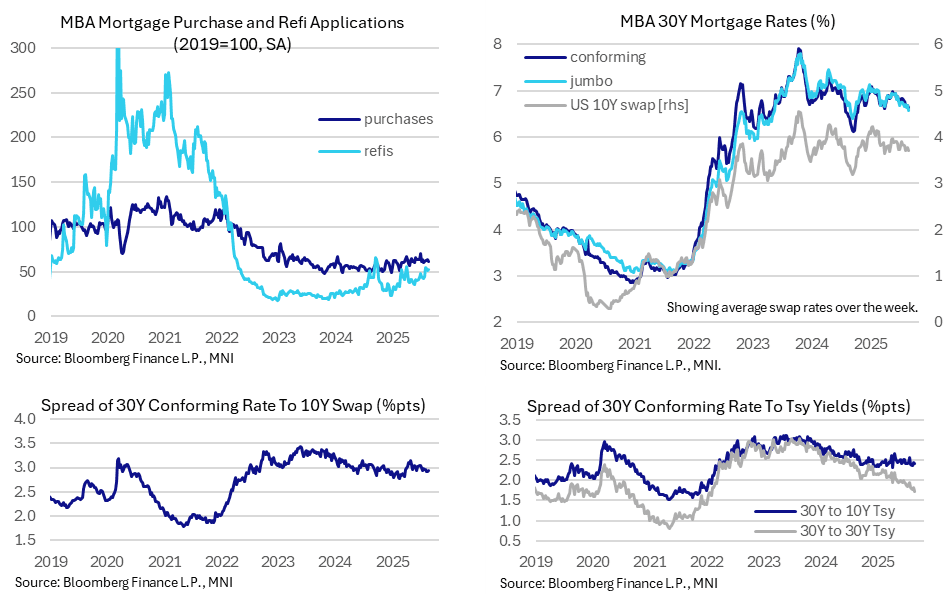

- MBA composite mortgage applications dipped -1.2% (sa) last week, a third consecutive small weekly decline after a refi-driven 11% increase earlier in August.

- New purchase applications -3.1% after 2.2%, refi applications 0.9% after -3.5%.

- Levels relative to 2019 averages: composite 58%, new purchases 61% and refis 52%.

- There wasn’t much sign of a boost from the 5bp decline in the 30Y conforming mortgage rate to 6.64% for a new low since early April’s 6.61% ytd low.

- The spread to average 10Y swap rates over the week meanwhile held at its slightly lower recent levels, between 291-293bp for three weeks now vs the range of 300bp +/-5bp seen mostly since reciprocal tariff announcements in April vs 285bps averaged in Q1. It’s a mild relative easing in lending standards recently.

- US Tsy Sec Bessent has in recent weeks talked on wanting to keep the spread between mortgage rates and treasuries flat or even bring it down. To this end, spreads to 10Y Tsy yields (the usual point of focus) have averaged 240bp over the past month, pretty stable considering they’ve averaged 245bp all year, although that’s down significantly from the closer to 300bp in 2023.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Aug-04 11:14

- EUR/USD: Aug05 $1.1425(E1.6bln), $1.1500(E1.4bln), $1.1550(E1.7bln), $1.1585-00(E2.5bln); Aug06 $1.1500-10(E1.6bln)

- USD/JPY: Aug06 Y152.00($1.0bln); Aug07 Y147.65($1.0bln), Y148.00-15($1.7bln), Y148.50($1.1bln)

- EUR/GBP: Aug05 Gbp0.8650-70(E1.3bln)

- AUD/USD: Aug05 $0.6465-80(A$1.1bln); Aug07 $0.6600(A$2.0bln)

BONDS: TD Maintain Bias for Lower Bund & Gilt Yields At Year-End

Aug-04 11:02

TD Securities note that bond markets “will continue to balance the impact of fiscal and tariffs”. They see “more scope for the latter to weigh on growth in the near term” and look for 10-Year Bund and 10-Year gilt yields to finish ’25 at 2.30% and 3.80%, respectively.

US TSYS: Stabilization Before A Thin Docket Ahead After Last Week’s Swings

Aug-04 10:54

- Treasuries have recently pared losses to further limit moves from Friday’s close with the nonfarm payrolls report and its hugely weak two-month revisions digested. For a succinct summary of last week's swings seen after a patient Fed and weak payrolls report, see the MNI US Macro Weekly (link here).

- We touch on it more in the STIR bullet but President Trump says he will announce a new Fed Governor and BLS commissioner in the coming days following a surprise resignation/termination on Friday.

- Cash yields are 1-2bp higher on the day, with 2Y yields for instance more than 25bp before pre-payrolls levels.

- 10Y yields, currently at 4.232%, appeared to meet some support at 4.20% on Friday, touching 4.2002%. It last breached 4.20% on Jul 1 and before that late Apr/early May.

- TYU5 trades at 112-05+ (-01) having pulled back off an overnight high of 112-12, on solid cumulative volumes of 510k as non-US participants caught up with Friday’s price action.

- Friday’s rally punched through 111-14+ (Jul 22/30 high) whilst the overnight high stopped just short of resistance at a bull trigger of 112-12+ (Jul 1 high). There’s further resistance seen shortly after with 112-15 (61.8% retrace of Apr 7-11 sell-off).

- Data: Factory orders Jun (1000ET)

- Fedspeak: None scheduled

- Bill issuance: US Tsy $82B 13W, $73B 26W bill auctions (1130ET)