US DATA: Mortgage Applications Dip Despite Modest Rate Relief

Jun-04 11:47

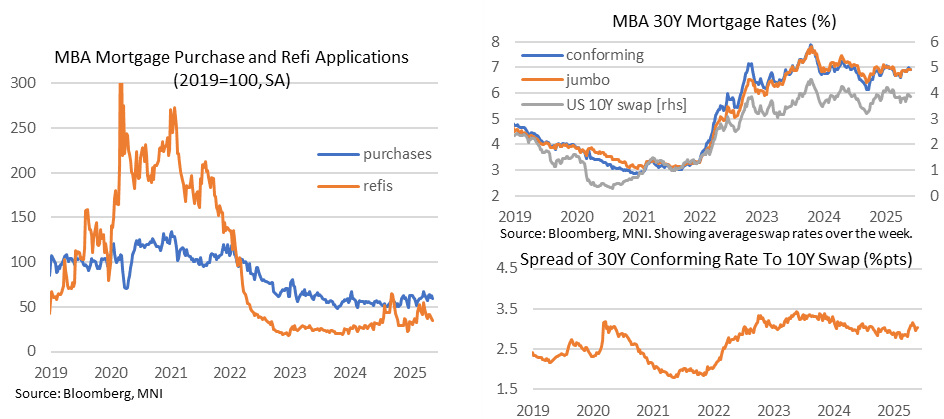

- MBA composite applications dipped -3.9% last week (sa) for a third consecutive weekly decline.

- Unusually, it was led by new purchases (-4.4% admittedly after 2.7%) whilst refis fell further (-3.5% after -7.1%).

- Relative levels for context: composite applications at 48% of 2019 averages (lowest since late April), new purchases at 60% (lowest since late April) and refis at 35% (lowest since Feb).

- The decline came despite the 30Y conforming mortgage rate falling 6bps to 6.92%, to reverse the prior week’s increase to what had been its highest since January.

- The spread of 30Y mortgages to 10Y swap rates was broadly stable but still on the higher side for the past year. It increased 2bp to 303bp having fluctuated between 315bp in early May (highest since early 2024 as banks tightened conditions) and 296bp in mid-May (lowest since reciprocal tariffs were announced in early April).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: Bonds Paring Losses

May-05 11:39

- Treasury futures are inching higher, 30Y following shorts to intermediates as curves temper steepening move (2s10s +0.740 at 48.972).

- No particular headline driver, volumes remain light (TYM5 220k) with UK and much of Asia on spring holidays, NY desks gradually populating.

- Tsy Jun'25 10Y contract breaking higher after trading in narrow 4-tick range for the past nine hours, TYM5 +8.5 at 111-13.5, revisiting early overnight high. Initial technical resistance above at 112-01.5 (High Apr 2); price needs to trade above key short-term resistance at 112-20+, the May 1 high, to reinstate a bullish theme.

US TSYS: Early SOFR/Treasury Option Roundup: Focus on Midweek FOMC

May-05 11:25

Option desks report mixed SOFR & Treasury options overnight, lighter volumes with multiple spring holiday closures in Asia and UK. Focus on Wednesday's FOMC policy annc, no rate change expected. Underlying futures mixed, curves twist steeper with the short end outperforming weaker Bonds (2s10s +2.465 at 50.697, 5s30s +3.158 at 90.038). Projected rate cut pricing largely steady to late Friday levels (*) as follows: May'25 at -0.5bp (-0.8bp), Jun'25 at -8.4bp (-8.4bp), Jul'25 at -25.5bp (-25.7bp), Sep'25 -46.9bp (-45.6bp).

- SOFR Options:

- +4,000 SFRZ5 95.93 puts, 9.5 ref 96.475

- 2,000 SFRK5 95.93/96.00 call spds ref 95.80

- over 3,500 SFRK5 96.06 calls, 0.5 ref 95.81

- Treasury Options:

- over 7,500 TYM5 112 calls, 25 last

- 1,600 FVM5 107/107.5 put spds ref 108-14.25

- 2,000 TYM5 110.5/111.25 put spds, 22 ref 111-06.5

- over 3,200 TYM5 111.25 calls, 46 ref 111-08

- 1,000 TYM5 111/112/113/114 call condors

- 1,600 FVM5 107.25 puts ref 108-15.25

USD: The Dollar is still pushing lower

May-05 11:17

- Further intraday lows for the Dollar, nothing fast, 1 pip at a time, but it has been a one way move so far during the early European session and into the US one.

- EUR, GBP, NOK, AUD, JPY, PLN, ZAR, and CAD are all at session high, and this is more of a pure FX move, given the lack of moves in Equities or eve Bonds (Yield).

- AUD is still the best performer and is still eyeing a test to the 0.6500 handle.