US DATA: Mortgage Activity Stalls, Jumbo Rates Continue To Trade Inside Regular

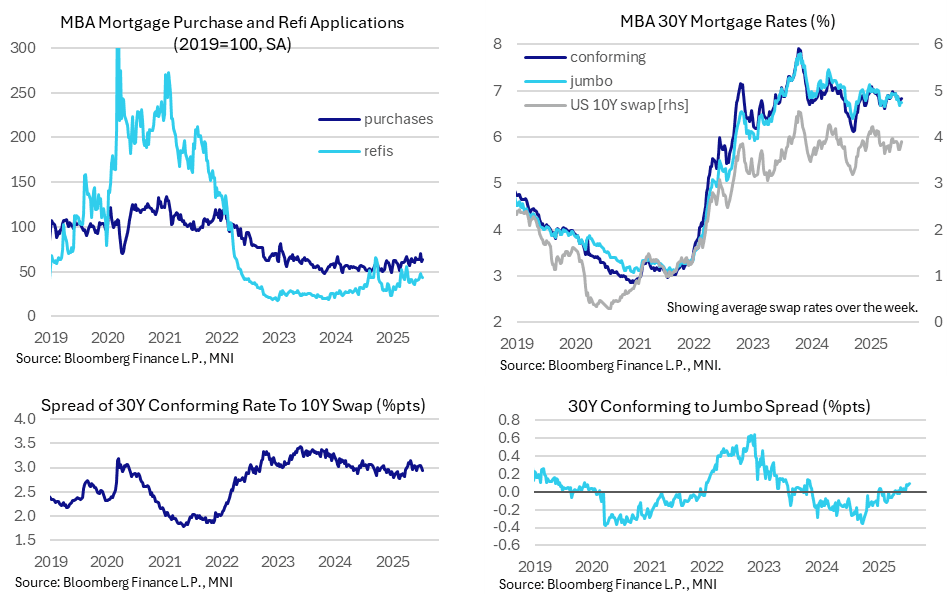

- MBA composite mortgage applications inched up 0.8% (sa) last week, essentially flat after -10% and +9.4% in the previous two weeks.

- New purchase applications outperformed after some rare trend underperformance since June, rising 3.4% after -11.8% compared to -2.6% after -7.4% for refis.

- Relative levels: composite at 54% of 2019 levels vs 64% for new purchases and 43% for refis.

- The 30Y conforming mortgage rate increased 2bp last week to 6.84% after a 5bp increase the week prior. The 6.77% in the first week of July was the lowest since early April.

- With mortgage rates fading a 7bp rise in average 10Y swap rates over the week, the spread narrowed a little further to 295bps for its tightest since mid-June although it has roughly kept to a 295-305bp range since the April reciprocal tariff announcements barring a brief peak of 315bps. It averaged 285bp in Q1.

- Within mortgage rate details, jumbo rates again traded inside at 6.75%. The regular-jumbo spread of 9bps is similar to the previous two weeks having last been higher in Oct 2023 in a sign of relative loosening in specific lending conditions in recent months.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: INVITE: Livestream MNI Connect with Atlanta Fed Bostic On June 30

You are invited to listen to a Livestreamed MNI Connect Video Conference with Federal Reserve Bank of Atlanta Raphael Bostic.

Details below:

- Speaker: Raphael Bostic, Federal Reserve Bank of Atlanta President

- Topic of discussion: 'The US Economic Outlook'

- DATE: Mon, 30 Jun 2025

- TIME: 15:00 - 16:00 BST

- This event is on the record and will run as a Zoom Webinar

To register please go to: MNI Webcast Registration

CROSS ASSET: Bonds Bid & Equities Offered

No clear headline driver for the latest round of equity selling & an FI uptick (Bund futures to fresh session highs, TY tests Asia highs).

- Focus remains centred on the Middle East after the U.S. strike on the Iranian nuclear facilities over the weekend, with hardline rhetoric between Israel & Iran ongoing, along with missile fire in both directions.

- On the lookout for any fresh news on that front.

- Some of the move in equities is attributable to the block sale in Euro Stoxx 50 futures, but that doesn't do much to explain the uptick in bonds.

US TSYS: Early SOFR/Treasury Option Roundup: 10Y Calls

Modest SOFR option volume reported overnight while Treasury options see some decent buying in Au'25 10Y calls. Benign reactions to US bombing 3 Iranian nuclear facilities over the weekend - with lack of a strong response by Iran cited for mildly lower underlying futures, narrow ranges. Projected rate cut pricing steady to mildly cooler vs. late Friday levels (*) as follows: Jul'25 steady at -3.6bp, Sep'25 at -19.5bp (-20bp), Oct'25 at -32.6bp (-33.6bp), Dec'25 at -49.9bp (-51bp).

- SOFR Options:

- Block, 2,500 SFRQ5 95.87/96.12/96.37 call trees, 2.5 ref 95.885

- 1,750 0QQ5 96.87/97.37 call spds

- 2,000 SFRU5 96.00/96.25/96.50 call flys ref 95.88

- 2,400 0QQ5 96.37 puts ref 96.69

- Block, 2,500 0QZ5 97.00/97.31 call spds, 8.5 vs. 96.765/0.10%

- Treasury Options:

- 1,750 wk4 TY 110.25/111.5 call spds, ref 110-29.5, exp 6/27

- over +27,000 TYQ5 112 calls, 28-27 vs 110-29.5/0.26%, appr vol 6.59%

- +20,000 TYQ5 112.5 calls, 20 vs. 110-29.5/0.19%, appr 6.71% vol

- -2,000 TYQ5 111 calls, 48 vs. 110-28/0.47%