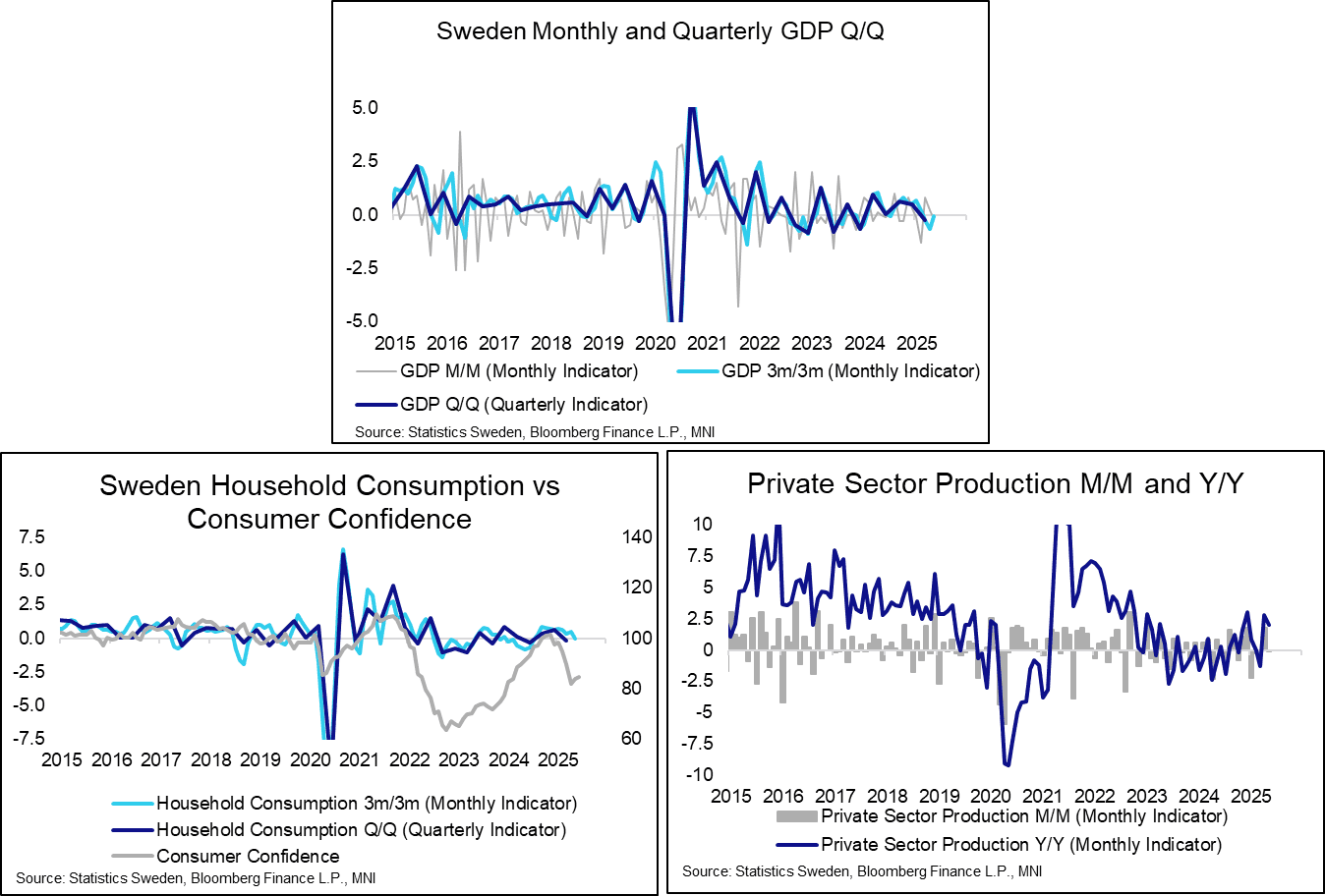

SWEDEN: Monthly GDP Indicator Dragged Lower By Weak Retail Sales Report

The Swedish monthly GDP indicator fell 0.2% M/M in May, in line with the three-analyst strong consensus (range -0.4% to -0.2%). On a 3m/3m basis, GDP fell 0.1%, above April’s weak -0.7% reading but still the third consecutive negative print. The Riksbank projected Q2 GDP at 0.9% Q/Q in the June MPR. Although the monthly activity indicator isn’t best predictor of actual GDP outcomes, and can sometimes be revised quite heavily, that forecast still seems optimistic. Taken alongside the firm flash CPI report earlier this week, another Riksbank cut in September seems more likely than in August for now. However, there is still another month of data (and tariff developments) to come before the August 20 decision.

- Household consumption fell 1.2% M/M (vs +0.4% prior) – an unsurprising development after the extremely weak May retail sales report. On a 3m/3m basis, the consumption indicator was flat (vs 0.5% prior).

- Private sector production also fell on a sequential basis (-0.1% M/M vs +1.8% prior). This was driven by pullbacks in services and construction production, offset a little by a rise in industrial production.

- Although industrial production has grown at 5%+ Y/Y for the last two months, the volatile industrial orders series fell 2.4% Y/Y in May (vs 7.4% prior), potentially indicative of waning demand.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: Bullish Trend Sequence

- RES 4: 0.6603 High Nov 11 ‘24

- RES 3: 0.6582 High Nov 12 ‘24

- RES 2: 0.6550 61.8% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 1: 0.6538 High June 5

- PRICE: 0.6503 @ 07:55 BST Jun 10

- SUP 1: 0.6458/6408 20- and 50-day EMA values

- SUP 2: 0.6357 Low May 12

- SUP 3: 0.6275 Low Apr 14

- SUP 4: 0.6181 Low Apr 11

The trend condition in AUDUSD is unchanged, it remains bullish and the pair continues to trade closer to its recent highs. Key support lies at 0.6408, the 50-day EMA. A clear break of this average is required to highlight a potential short-term reversal. The pair has recently cleared a key short-term resistance at 0.6515, the May 7 high, confirming a resumption of the uptrend. Sights are on 0.6550, a Fibonacci retracement.

STIR: Over 45bp Of BoE Cuts Priced Through Dec

A dovish move in GBP STIRs on the back of the softer-than-expected pay growth and larger-than-expected fall in payrolled employees detailed in previous bullets.

- BoE-dated OIS now shows 46bp of cuts through year-end vs. ~41bp at yesterday’s close.

- The strip now almost fully discounts a 25bp cut come the end of the September MPC (24bp vs. 20bp at yesterday’s close).

- SONIA futures are flat to +8.5.

- SFIZ5 hits the highest level seen since mid-May, while June highs cap the rally in SFIZ6.

- Looking ahead, wage data points to ongoing downside risks vs. BoE forecasts.

- We provided greater colour on the release in previous bullets and will provide the usual detailed review in due course.

- Little of note on the UK calendar for the remainder of the day.

- Domestic focus moves to the release of the government’s spending review, due tomorrow. More colour on that event can be found in our latest Gilt Week Ahead.

- Elsewhere, Wednesday will see BoE’s Saporta speak on monetary policy implementation. Our Gilt Week Ahead provides greater colour on that address as well.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.207 | -0.5 |

Aug-25 | 4.024 | -18.8 |

Sep-25 | 3.972 | -24.0 |

Nov-25 | 3.822 | -39.0 |

Dec-25 | 3.752 | -46.0 |

Feb-26 | 3.652 | -56.0 |

Mar-26 | 3.631 | -58.1 |

NORWAY: Easing CPI-ATE Momentum Underscores Case For H2 Easing

Although Norges Bank is not under pressure to cut rates due to a relatively resilient mainland economy, the unwind of Q1 inflationary pressures (which delayed the first cut back in March) suggest there is scope to ease at least once in H2 - in line with the March MPR rate path.

- Seasonally adjusted CPI-ATE prices rose 0.08% M/M for the second consecutive month in May, and have now been consistent with 2% inflation on an annualised basis since March. 3m/3m momentum pulled back to 2.95% (vs 4.11% in April, 4.22% in March) for the lowest since November 2024.

- Looking at NSA data, services excluding rents fell to 3.04% Y/Y (vs 4.31% prior). As expected, airfares were the largest contributor here, falling 9.78% Y/Y (vs +26.07% prior). However, recreation and culture and restaurant and hotels components also eased somewhat in May.

- Rents decelerated to 3.62% Y/Y (vs 3.88% prior), the lowest since April 2023.

- Domestic goods ex-energy rebounded to 5.38% Y/Y (vs 4.51% prior), while imported goods rose to 1.02% Y/Y (vs 0.31% prior). Food prices rose to 5.05% Y/Y (vs 3.12% prior), following Easter sales in April. Meanwhile, trends in clothing and footwear and furniture and household equipment remain soft. The strengthening NOK appears to be containing imported price pressures.

- Electricity including grid rent pushed up headline inflation, accelerating to 16.82% Y/Y (vs -5.21% prior) on a base effect. Norges Bank should look through this price action.