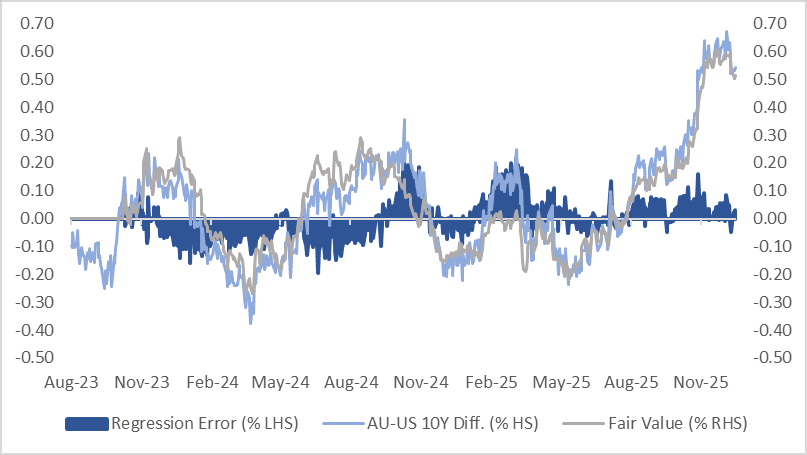

AUSSIE BONDS: Modestly Cheaper, Recent Narrowing In AU-US 10Y Diff Reverses

ACGBs (YM -1.0 & XM -2.0) are modestly weaker.

- Job vacancies were down -0.2%q/q (ending in Nov). Job vacancies remain around 30% off 2022 highs, but the trend though was only down modestly, to end Nov just under 327k.

- Cash US tsys are slightly richer, with a steepening bias, in today’s Asia-Pac session.

- Cash ACGBs are 1-2bps cheaper with the AU-US 10-year yield differential at at +55bps. A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month (1Y3M) swap spread over the past two years suggests the current spread sits 3bps above its regression-implied fair value.

- Today’s Oct-36 auction result extended the recent trend of firm pricing for ACGBs, with the weighted average yield printing 0.22bps through prevailing mids, according to Yieldbroker. However, demand was weaker, as reflected by a cover ratio of 3.1950x, down from the prior 3.7100x. The AOFM plans to sell A$700mn 3.25% 2029 bond on Friday.

- The bills strip is little changed.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 30% for February to 90% by June and 144% by December 2026.

- Tomorrow, the local calendar will see Consumer Inflation Expectation data.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

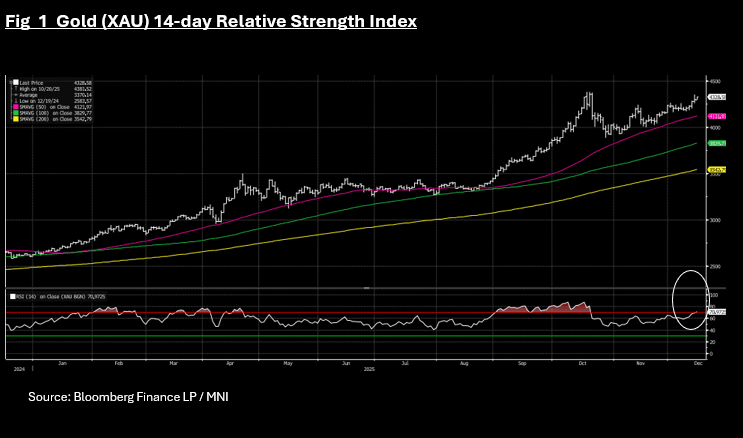

GOLD: Gold Gains on Equity Weakness

- Gold has continued last week's rally Monday as equity markets across the region have a weak start.

- Gold is up +0.67% to US$4,328.41 and is now -0.60% below the October high of US$4,356.30

- Gains in recent days sees gold now overbought on the 14-day relative strength index. Having spent most of September and October overbought gold then moderated back below.

- Gold will have the dual forces impacting it over the coming days being equity markets and the technical outlook. Equity volatility could provide a natural bid to gold into month end yet US interest rates will continue to be key in the next move for bullion.

- As data continues to flow in the US post shutdown, there will be a lot to digest for gold markets as they assess the probability of rate cuts in 2026.

- Currently the market has only 6bps of cuts priced in for the next FED meeting, suggesting that should this week's data be weaker than expected, markets could look to price in greater expectations for cuts.

- Weaker data could feed into gold prices also. Given gold has no coupon, it is very sensitive to rate cuts (reduces funding costs) and this week could be provide further input into whether the next FED meeting could become a 'live' meeting.

- CMOC Group, one of China’s biggest miners, extended its push into precious metals with a $1 billion deal to buy the Brazilian operations of Equinox Gold Corp. It will take full ownership of two Equinox entities — Leagold LatAm Holdings BV and Luna Gold Corp. — that control several mines or deposits in the South American nation. (per BBG)

- ANZ Group analysts have restated their forecasts for gold, predicting it will reach US$4,800 in 2026.

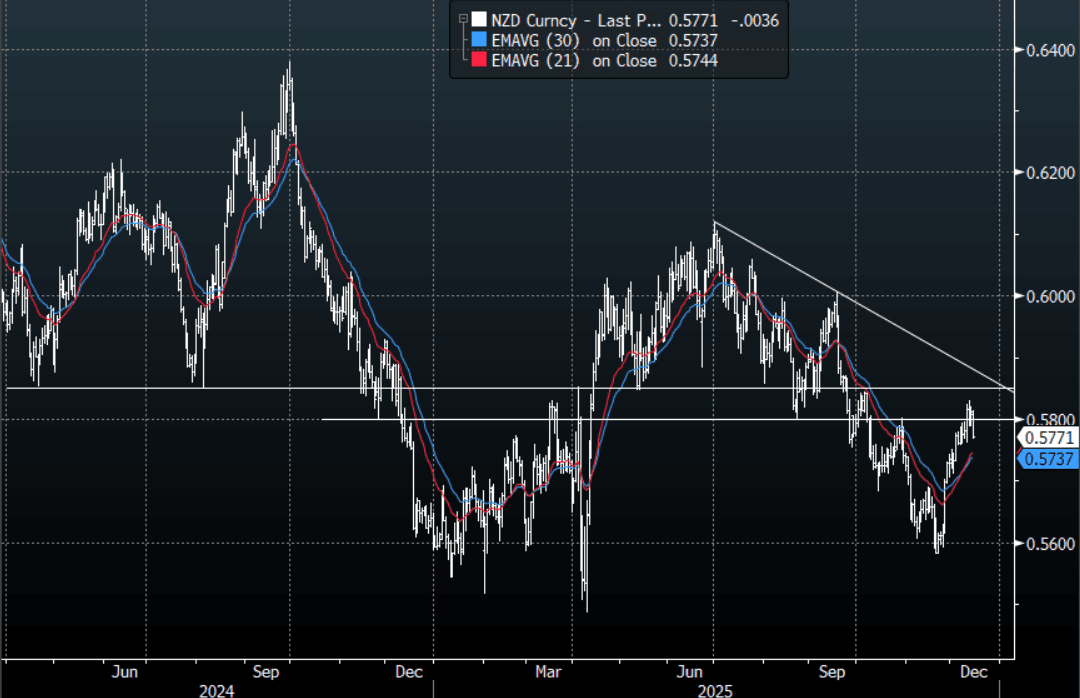

NZD: NZD/USD - Fails Above 0.5800, Support seen 0.5730-50 Initially

The NZD/USD had a range today of 0.5766-0.5814 in the Asia-Pac session, going into the London open trading around 0.5766, -0.70%. The NZD has slid lower in our day aided by comments from the RBNZ Governor. The US stock market wobbled on Friday as AI concerns came back to the fore and US yields in the long end tick back up. This saw the USD’s decline stall but it has not bounced, yet. The NZD’s momentum higher looks to have stalled above 0.5800 for now. On the day, price has broken below the 0.5780 area, signaling a potential retracement to the more important 0.5730/0.5750 support. I have this area between 0.5800-0.5900 as being decent longer-term resistance and it has provided some early headwinds on its first attempt.

- RBNZ Governor - Financial Conditions Have Tightened More Than Expected: The RBNZ has released some remarks from new Governor Breman. The Governor states that the economy has evolved broadly in line with the conditions laid out in the Nov policy review: "We continue to see signs that growth is recovering after having stalled in the middle of this year. The labour market is still weak but is expected to recover as demand in the economy strengthens. We remain confident that annual headline consumer price index inflation will decline towards the 2 per cent target mid-point by the middle of next year."

- She added that the OCR projections imply a slight risk of further easing, but: "However, if economic conditions evolve as expected the OCR is likely to remain at its current level of 2.25 per cent for some time.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD410m Dec 18 ), 0.5690(NZD531m Dec 18 ), 0.5860(NZD471m Dec 18 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

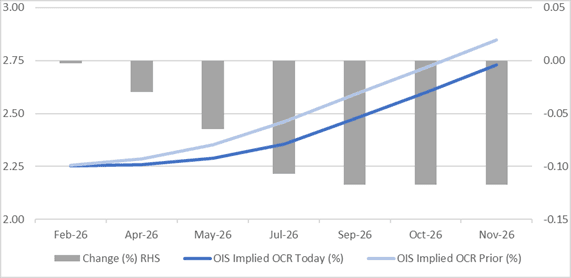

BONDS: NZGBS: Strong Rally As RBNZ Gov Pushes Back Vs Hike Expns

NZGBs closed showing a bull-steepener, with yields 5-9bps lower, after the market viewed comments from RBNZ Governor Anna Breman as a warning that market pricing was too hawkish.

- RBNZ Governor Anna Breman has pushed back against investor bets on an interest-rate hike next year, saying she expects the Official Cash Rate will remain unchanged for some time. “Financial market conditions have tightened since the November decision, beyond what is implied by our central projection for the OCR,” Breman said in a statement Monday in Wellington. “As always, we are closely monitoring wholesale market interest rates and their effect on households and businesses.”

- On a relative basis, NZGBs have outperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 4-5bps lower. Today’s move has halted the sharp rebound in the NZ-AU differential following the recent RBNZ policy decision and guidance.

- Swap rates closed 1-5bps lower, with a steeper 2s10s curve.

- RBNZ-dated OIS pricing closed 12bps softer for late 2026 meetings. No tightening is priced for February, while November 2026 now assigns 48bps.

- Tomorrow, the local calendar will see Food Prices and Non-Resident Bond Holdings data alongside the Government’s Half-Year Fiscal Update.

Figure 1: RBNZ Dated OIS Current vs. Prior (%)

Bloomberg Finance LP