US TSYS: Modest Selling Seen Ahead Of FOMC

- Treasuries are extending session lows across the curve, translating to yields 2.5-3.5bp higher on the day.

- TYZ5 at 113-09, with support at 113-04 (Oct 27 low) after the later cleared the 20-day EMA, after which lies 112-26 (50-day EMA).

- That said recent weakness is deemed corrective from a technical backdrop with a bullish structure still in place with resistance at 113-24 (post-CPI high) before 114-02 (Oct 17 high).

- 2Y yields at 3.514% (+2.4bp), off week to date lows of 3.480% and mid-Oct lows of 3.374%. From a longer-term sense, some might look to fade off the 50d MA of 3.562% (equating to 104-07) as the 2Y yield recovers.

- 10Y yields at 4.010% (+3.6bp) with risks look tilted to the downside again on a medium-term basis with the 50d MA providing resistance since August. The October low is 3.9342% whilst next support moves back up to circa 3.90% (23.6% retrace of the 2020/2023 range). Currently at 3.987%.

- SOFR futures see the day’s losses of up to 3 ticks in the M6. The terminal implied yield of 3.015% (H7) last closed higher on Oct 9, i.e. prior to the increase in US-China trade tensions on Oct 10.

- S&P 500 futures have come close to session lows of 6929.75 after fresh record highs of 6952.00 earlier on. That earlier high came close to projected resistance at 6953.25 (2.00 proj of Aug 1-15-20 price swing) after which lies 6974.04 (3.382 proj), whilst support is seen at 6812.25 (Oct 9 high).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Remains Below Resistance

- RES 4: 1.3789 High Jul 1 and key resistance

- RES 3: .3661/3726 High Sep 18 / 17

- RES 2: 1.3537 High Sep 23 1

- RES 1: 1.3485 50-day EMA

- PRICE: 1.3421 @ 16:12 BST Sep 29

- SUP 1: 1.3324 Low Sep 25

- SUP 2: 1.3282 Low Aug 6

- SUP 3: 1.3254 Low Aug 4

- SUP 4: 1.3144 38.2% retracement of the Jan 13 - Jul 1 bull cycle

GBPUSD traded lower last week, marking an extension of the current bear cycle that started Sep 17. The move down has resulted in a break of 1.3491, a trendline support drawn from the Aug 1 low. This undermines a recent bullish theme. Note too that 1.3333, the Sep 3 low and a key support, has been pierced, opening 1.3282 next, the Aug 6 low. Initial key resistance to watch is 1.3537, the Sep 23 high. A break of it would signal a reversal.

BONDS: EGBs-GILTS CASH CLOSE: Bull Flattening As Euro Inflation Week Unfolds

European curves bull flattened Monday.

- Bull flattening started early, with a looming federal government shutdown in the US setting a cautious undertone.

- BOE's Ramsden sounded to be on the dovish side in an appearance and does not appear to be guiding away from a vote for a November cut so far.

- Data didn't have a major market impact. Spanish flash September core HICP was slightly softer than expected, while Eurozone economic confidence slightly above-consensus. BOE credit data was largely in-line.

- UK instruments slightly outperformed German counterparts across most of their respective curves, with the most notable divergence being at the short end.

- Periphery/semi-core EGB spreads closed mixed, with France underperforming amid continued fiscal uncertainty (Friday saw Spain upgraded by Fitch/Moody's and France's outlook lowered by Scope).

- The Eurozone flash September inflation round continues Tuesday with French, German and Italian data, with the bloc-wide figure out Wednesday. MNI's preview is here. We also get UK GDP data Tuesday, as well as several central bank speakers including BOE's Breeden and Mann, and ECB's Lagarde.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.7bps at 2.023%, 5-Yr is down 2.3bps at 2.312%, 10-Yr is down 3.9bps at 2.707%, and 30-Yr is down 5.6bps at 3.272%.

- UK: The 2-Yr yield is down 2.7bps at 3.988%, 5-Yr is down 3bps at 4.145%, 10-Yr is down 4.6bps at 4.7%, and 30-Yr is down 5.2bps at 5.509%.

- Italian BTP spread down 0.9bps at 82.6bps / French OAT up 0.5bps at 82.7bps

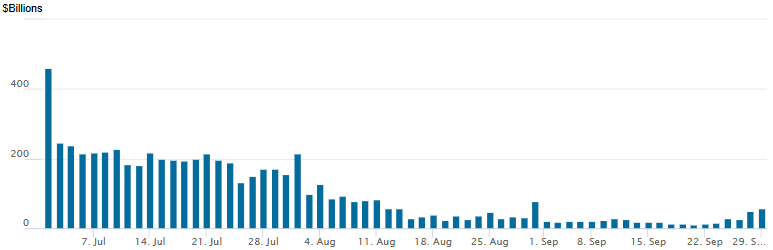

US: FED Reverse Repo Operation Rising Into Month End

RRP usage climbs to $56.220B ahead month end with 26 counterparties this afternoon from $48.073B Friday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.