STIR: Modest Hawkish U.S. Adjustments Quickly Fade

For clarity, no notable NET moves following those comments from Daly. Selling flow was seen in the likes of FFV5, SFRU5 and SFRZ5. However, the impact is limited and quickly faded as a 25bp cut remains fully priced for the Sep FOMC. Contracts 0.5-1.0 tick more hawkish on net vs. pre-Daly levels.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT AUCTION RESULTS: 4.25% Jun-32 Gilt Tender

| 4.25% Jun-32 Gilt | |

| Amount | GBP1.00bln |

| Avg yield | 4.161% |

| Bid-to-cover | 4.42x |

| Tail | 0.3bp |

| Avg price | 100.527 |

| Low price | 100.510 |

| Pre-auction mid | 100.506 |

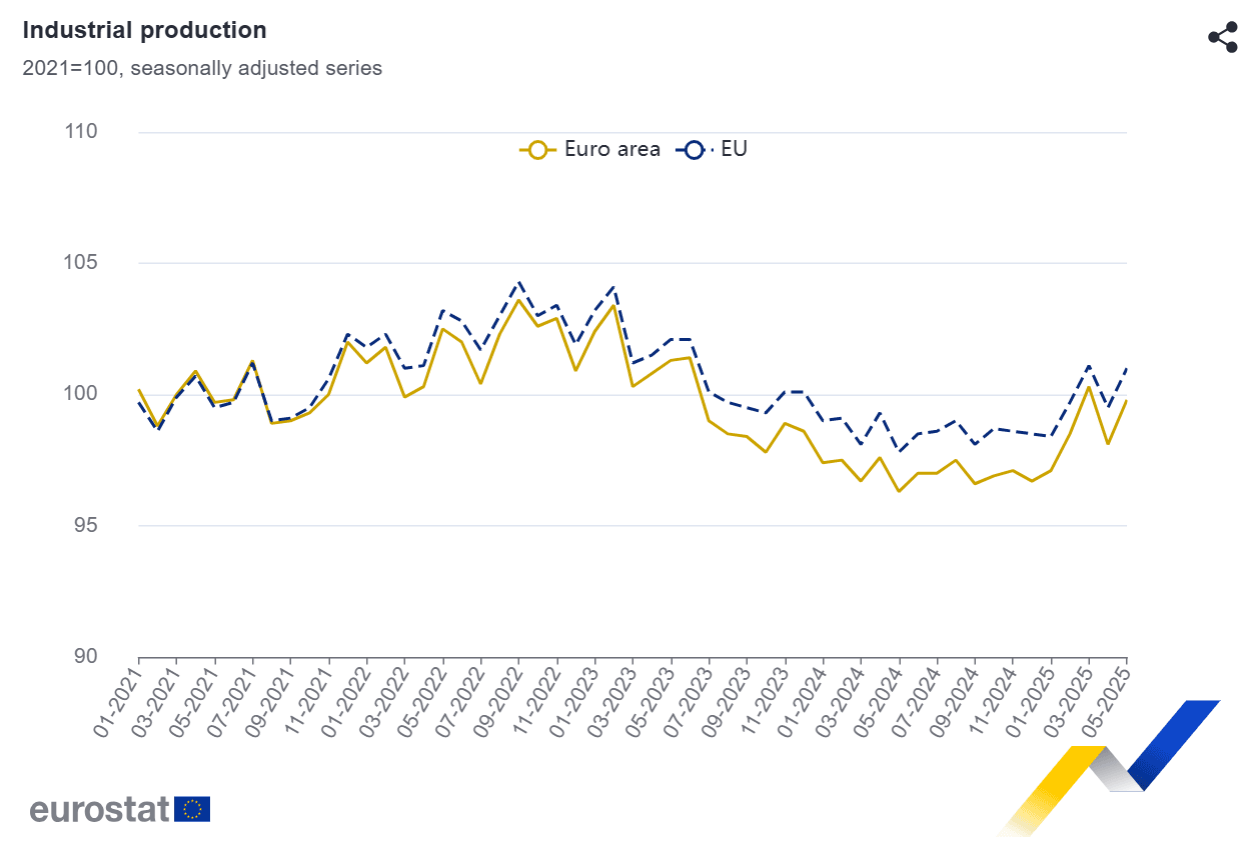

MNI: EUROZONE MAY IP +1.7% M/M, +3.7% Y/Y

- MNI: EUROZONE MAY IP +1.7% M/M, +3.7% Y/Y

EUROZONE DATA: IP Much Stronger Than Expected In May; Ireland A Likely Culprit

Eurozone industrial production was much stronger-than-expected in May, with volatile Irish data once again a likely culprit. On a monthly SA basis, production rose 1.7% M/M, above the 1.0% consensus and April’s -2.2% (revised up from -2.4% initial). After IP data was supported by tariff frontloading in Q1, and April figures were weighed down by Liberation Day-induced uncertainty, the focus over the coming months will be on whether EZ industry can start to exhibit a more durable recovery.

- On an annual basis, production rose 3.7% Y/Y, but note that April’s reading was revised down to 0.2% from an initial 0.8%. In any case, this was the strongest annual print since September 2022.

- At a sub-component level, durable consumer goods fell for the second consecutive month (-1.9% M/M vs -0.4% prior). Meanwhile, nondurables rebounded 8.5% M/M after -5.7% in April. Capital goods also recovered somewhat, rising 2.7% M/M (vs -1.3% prior).

- As noted above, the volatility of Irish IP data was once again apparent in May, consistent with the ongoing US tariff policy uncertainty. Irish IP rose 12.4% M/M, after -12.5% M/M in April, +8.6% M/M in March and +12.6% M/M in February.

- Across the four major Eurozone economies, we have previously flagged mixed trends. Italian and French IP was weaker-than-expected in May, while Spanish and German figures were stronger than expected.

Looking ahead, industrial confidence remains subdued according to the EC’s sentiment survey (-12.0 in June vs -10.4 prior). However, the June manufacturing PMI inched up to a 34 month high of 49.5 (vs 49.4 in May).