INDONESIA: Moderate Inflation, BI Can Support Growth But IDR Softer

Oct-02 01:28

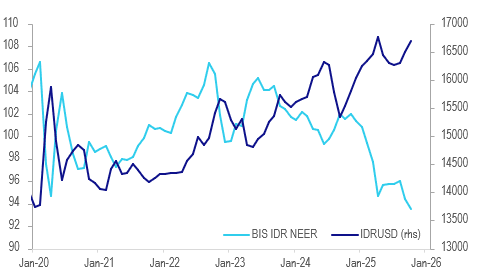

September core inflation held at 2.2%, 0.3pp below April’s peak as domestic demand has softened. Headline was higher than expected at 2.65% though, highest since May 2024, up from August’s 2.3% due to higher volatile food prices and gold jewellery. Both measures remain well within Bank Indonesia’s (BI) 1.5-3.5% target band. There has been less focus on FX stability with three consecutive rate cuts to September as BI shifts to supporting growth. USDIDR is over a percent higher than the last BI meeting and the 22 October decision will show if FX is regaining focus.

- The IDR has also weakened against other currencies with the BIS NEER 0.7% lower since 17 September rate cut.

- JP Morgan continues to forecast 25bp BI rate cuts in October and November given its shift to supporting growth and inflation is currently within its band. JP Morgan also believes it will want to ease before base effects push headline above target in early 2026 but if “growth pressures persist early next year, the central bank may look past the temporary surge in headline CPI and lean on the weak core CPI profile to deliver more easing”.

- Higher volatile food prices contributed to the pickup in headline in September with the 6.4% y/y increase in food prices driven by rice, chili and shallots. JP Morgan notes that unseasonably wet weather has impacted planting.

- Indonesia’s headline and core inflation while moderate are above the non-Japan/China Asian aggregates which were around 1.8% in August but rates at 4.75% also tend to be higher.

IDR

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Central Bank Withdraws CNY150.1bn via OMO

Sep-02 01:24

- The PBOC issued CNY255.7bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY405.8bn.

- Net liquidity withdraws CNY150.1bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.41%, from prior close of 1.44%.

- The China overnight interbank repo rate is at 1.32%, from the prior close of 1.25%.

- The China 7-day interbank repo rate is at 1.41%, from the prior close of 1.45%.

MNI: CHINA PBOC CONDUCTS CNY255.7 BLN VIA 7-DAY REVERSE REPO TUES

Sep-02 01:22

- CHINA PBOC CONDUCTS CNY255.7 BLN VIA 7-DAY REVERSE REPO TUES

CNH: USD/CNY Fixing Edges Higher, Fixing Error Unchanged

Sep-02 01:18

The USD/CNY fix printed at 7.1089, versus a BBG market consensus of 7.1335.

- The fixing continued to edge higher, in line with higher market estimates (relative to Monday's outcome). The fixing error was basically unchanged at -246pips.

- USD/CNH is tracking a touch higher in early Tuesday dealings, last near 7.1360.

- The recent rebound in the USD/CNY fixing comes without much shift in broader USD trends, which may be driving some short covering on USD/CNH.