MNI UST Issuance Deep Dive: July 2025

Jul-02 21:15By: Tim Cooper and 2 more...

Fiscal Policy+ 3

Download Full Report Here

EXECUTIVE SUMMARY

- July is set to be a key month for US issuance. The "One Big Beautiful" fiscal bill is nearing passage as we write, which will of course have deficit financing implications, not to mention an increase in the debt limit ($5T in the Senate version of the bill), thereby ending that impasse. Additionally reforms to the Supplementary Leverage Ratio for large banks looks imminent, which would in theory provide a lift to Treasury demand.

- The month will culminate with the quarterly Refunding process, highlighted by July 28's financing estimates, followed by July 30's announcement of upcoming auction sizes and any adjustment to guidance. We will look at these issues in our Refunding Preview later this month.

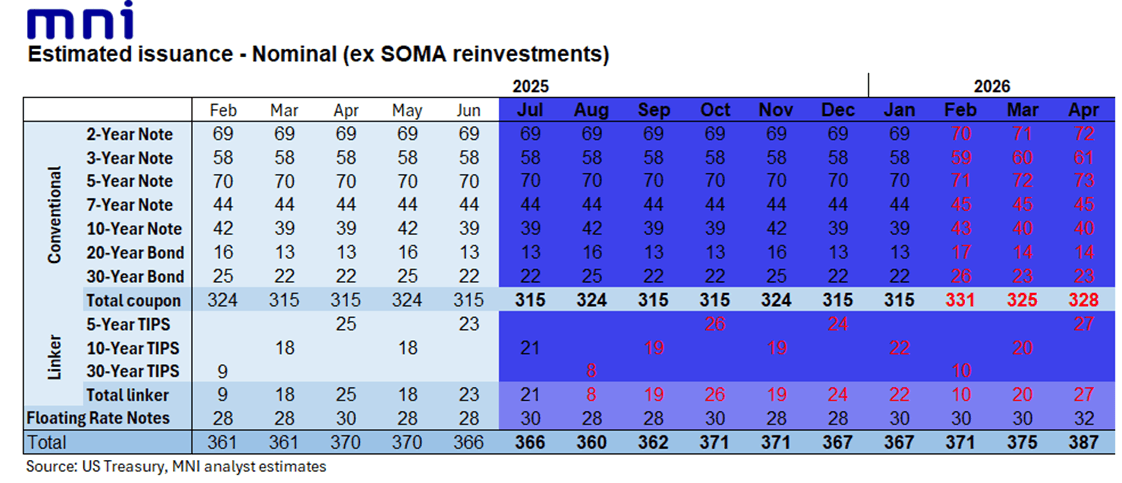

- Future Coupon Upsizing: MNI's working assumption has been that coupon sizes would next be raised in early 2026, potentially at the February refunding. Consensus has been mixed on this topic, with most analysts seeing the next upsizing at some point in 2026, though others suggesting it could occur beyond next year. Indeed it is increasingly in question whether Treasury's next move will be an increase or a decrease in coupon sizes.

- June Auction Review: June’s Treasury coupon auctions were mixed, with four trading through and three tailing.

- Upcoming issuance: July’s issuance schedule is set to see $315B in nominal Treasury coupon sales (unch from June), in addition to $21B in 10Y TIPS and $30B FRN for a total of $366B (unch from June). Sales for the month start on Tuesday July 8 with $58B of 3Y Note, Wednesday July 9 with $39B of 10Y Note, and Thursday July 10 with $22B of 30Y Bond (all announced on Thursday Jul 3).