US TSYS/SUPPLY: MNI UST Deep Dive: MNI Aug 2025 Refunding Review

We've just published our review of Treasury's latest quarterly refunding - Download Full Report Here

Bigger Buybacks, Same Guidance: Treasury’s Quarterly Refunding for August brought limited surprises on the guidance and near-term issuance fronts, but a meaningful set of enhancements to the buyback program.

- Financing estimates for the upcoming quarters were almost exactly in line with MNI’s estimates, and reflected a large near-term cash raise via bill issuance.

- With forward guidance on increasing coupon sizes left unchanged, and Treasury clearly leaning on bill issuance to meet borrowing requirements, we are likely to see remaining analyst expectations of an early/mid-2026 upsizing pushed back to later in that year.

- MNI maintains its expectation of the next upsizing coming in August 2026 though risks skew to a later date.

- July’s coupon auctions were mixed, with no clear strength in any particular segment of the curve.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

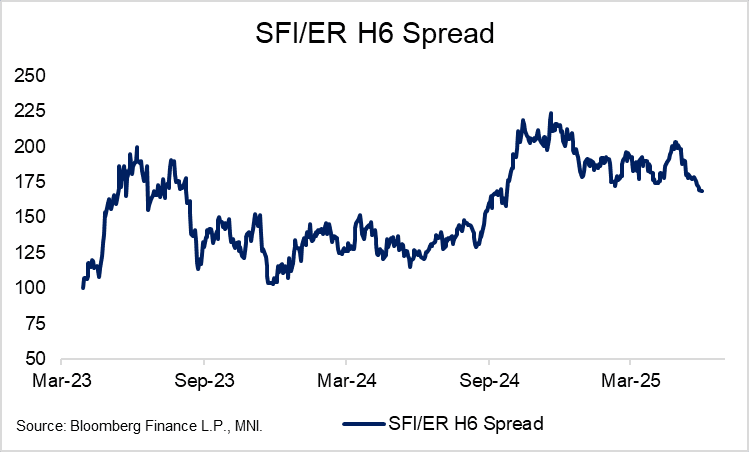

STIR: Lagarde Offers Little New At Sintra, SONIA/Euribor H6 Spread Near YTD Lows

- From a cross-market perspective, we note that the SONIA//Euribor H6 spread has consolidated below the March 11 closing low of 172.5bps over the past few sessions, currently trading at 169bps after closing above 200bps on May 30. The combination of a more cautious ECB stance and dovish BOE repricing drove movements in the spread through June.

- Looking ahead, markets probably need to see greater deterioration in the UK labour market/a swifter than expected moderation in inflation to be comfortable with discounting a meaningful deviation from the once per quarter cutting cycle that has become familiar in recent months.

- Meanwhile, the bar to significant near-term ECB repricing will likely hinge on any unexpected developments in the trade negotiations. The FT reported earlier today that "European capitals have hardened their position in trade talks with Donald Trump, insisting the US drops its tariffs on the EU immediately as part of any framework deal before the looming deadline on July 9". Such a stance could risk an inflammatory reaction from the President.

- President Lagarde offered little of note at today’s Sintra panel, re-iterating the ECB’s data-dependent approach and not elaborating on any questions pertaining to the exchange rate (now in more focus after VP de Guindos’ comments earlier this morning). As such, Euribor futures followed Treasuries lower through the panel, in response to some dovish leaning (or at least, non-committal) comments from Fed Chair Powell – see more above. Futures are flat to +2.5 ticks through the blues, while trendline resistance in the U5/U6 spread remains unchallenged.

- Tomorrow's regional calendar includes unemployment data from Spain, Italy and the Eurozone, though these aren't usually market moving releases.

STIR: BoE Pricing Steady Around 55bp Cuts Through Dec

GBP STIRs have pulled away from dovish session extremes given the adjustment in Fed pricing after the U.S. data.

- SONIA futures flat to +5.5, with the strip bull flattening.

- SFIZ5 & Z6 pierced respective May 9 & May 8 high before a retrace. Bulls will now look to target wider May highs in those contracts.

- BoE-dated OIS hasn’t been able to push consistently beyond 55bp of cuts through year-end, with markets probably needing to see greater deterioration in the labour market/a swifter than expected moderation in inflation to be comfortable with discounting a meaningful deviation from the once per quarter cutting cycle that has become familiar in recent months.

- Comments from BoE dovish dissenter Taylor are due tomorrow.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.005 | -21.3 |

Sep-25 | 3.931 | -28.6 |

Nov-25 | 3.758 | -46.0 |

Dec-25 | 3.665 | -55.2 |

Feb-26 | 3.531 | -68.7 |

Mar-26 | 3.495 | -72.2 |

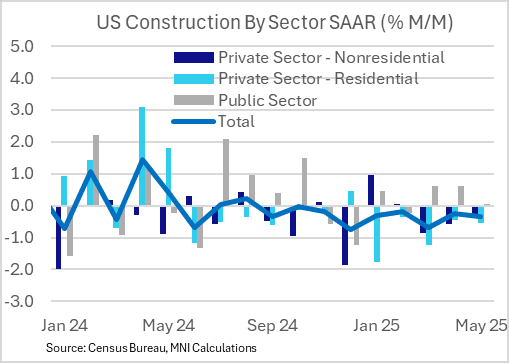

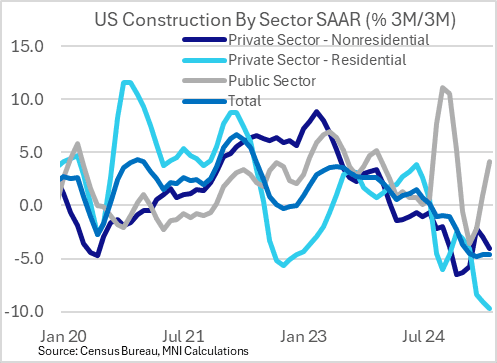

US DATA: Construction Values Continue To Contract With Residential Activity Weak

May's Construction Spending report showed a 7th consecutive monthly drop in value terms, of -0.3% (-0.2% prior rev up from -0.4%), basically in line with -0.2% consensus. This was another weak report that showed broad based weakness across private sector construction, with negative momentum building.

- Overall construction value is now down 3.5% from the May 2024 peak of $2.215T (SAAR) and is contracting at a 4.7% 3M/3M (ie quarterly) annualized rate. While this series is in nominal terms, it's notable that 3M/3M changes are as weak as they have been in the last 25 years.

- That's true across sectors: total private sector construction value fell 0.5% M/M (hasn't posted a positive month since May 2024), led by another weak reading for residential construction (which is half of private sector construction - falling 0.5% M/M).

- Residential construction is now falling at a 9.7% 3M/3M annualized pace, the most since July 2009 amid the US housing crash.

- Two notes on the more positive side from a growth perspective: Manufacturing construction's decline slowed (-0.1%, "best" in 5 months) and is now shrinking at a 3.6% 3M/3M rate, the least bad since November 2024, leaving the door open to a 2nd half recovery. And public sector (one-quarter of overall construction) momentum is roundly picking up, rising 0.1% M/M for the 3rd consecutive sequential gain, and now increasing at a 4.1% 3M/3M pace, fastest in 5 months.

- This report merely confirms that residential investment is contracting and is likely to subtract from GDP this year, with nonresidential structures investment continuing to look weak as well.