MNI US Payrolls Preview: Slack Metrics Eyed With Risks Rising

Sep-03 17:11By: Chris Harrison

EmploymentUSUnemploymentJerome Powell+ 1

Hidden PDF

Executive Summary

- Nonfarm payrolls growth is seen at 75k in August (sa) per the broad Bloomberg survey, after 73k in July.

- Revisions are going to be particular focus after last month’s huge downward revisions heavily altered recent trends, with non-health private payrolls growth at best stalling for the past three months, and dominated the market reaction.

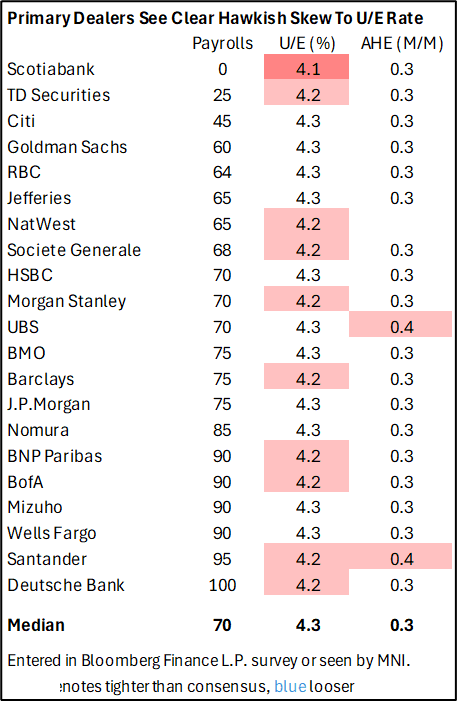

- The median primary dealer analyst eyes 70k whilst the Bloomberg whisper currently sits at 83k but with the ADP report still to come after publication of this preview.

- Payrolls figures are increasingly being seen in light of a sharply reduced ‘breakeven’ pace on significant moderation in labor force growth. We generally see estimates between 50-100k/month.

- The unemployment rate is seen at 4.3% but with a sizeable skew towards a 4.2% - it doesn’t take much from 4.25% in July. This rate has moved within a 4-4.25% range since July 2024 and will be watched closely as gauge of labor market slack amid uncertainty over the signal sent by monthly payroll changes.

- An added complication worth considering is the soon-to-be-published preliminary benchmark revision due Tuesday (Sep 9), with expectations of a second year of heavy downward revisions.

- Whilst there has been a dovish build-up to this payrolls report, and with ADP and ISM services still to come before then, we currently assess that risks for market reaction are skewed towards a downside surprise.