MNI US Payrolls Preview: Early Test Of Latest Powell Patience

Jul-31 10:36By: Chris Harrison

Employment+ 3

Download Full Report Here

Executive Summary

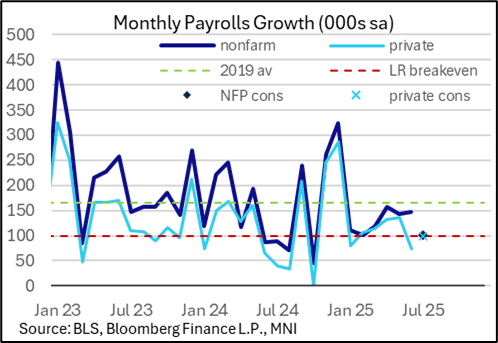

- Nonfarm payrolls growth is seen at 104k in July (sa) per the broad Bloomberg survey after 147k in June.

- The median primary dealer analyst eyes 100k whilst the Bloomberg whisper currently sits at 115k after little net reaction to the stronger than expected ADP report for July.

- Government payroll growth is expected to be much softer after a surprise 73k surge in June, which we think was more likely down to seasonal adjustment quirks. There’s a wide range of primary dealer estimates for public payrolls growth in July, from +20k to -55k.

- Consensus sees private sector payrolls rising 100k after a disappointing 74k in June and the breadth of gains should again be watched. 59k of this came from the cyclically insensitive health & social assistance category, whilst roughly as many of the 250 industries increased on the month as those that decreased.

- Payrolls growth should continue to be viewed against long-run breakeven estimates of around the 100k mark although some, such as Deutsche Bank, see this potentially being as low as 50k owing to continued immigration curbs.

- The unemployment rate is widely expected to tick up a tenth to 4.2% after a surprisingly low 4.11% in June as it pulled back from a cycle high of 4.244% in May. A faster-than-expected deterioration will be required for the final six months of the year to reach the FOMC's June Q4 median projection of 4.5%.

- We highlight FOMC discussions on QCEW data pointing to softer payrolls growth, with Powell citing the unemployment rate as suggesting labor demand and supply are cooling in tandem.

- We expect two-sided risks but with greater sensitivity to a dovish report after a hawkish shift on a patient Powell at Wednesday's FOMC press conference. There is 11.5bp of cuts priced for Sept and 36bp for end-2025.

- We’re still to get the Aug NFP report, preliminary benchmark revision estimates and two CPI reports before the Sept 16-17 FOMC meeting.

Trending Top

May-22 16:54