MNI US OPEN - Venezuela Uncertainty Isolates Market Reaction

EXECUTIVE SUMMARY

- TRUMP SAYS U.S. IS ‘IN CHARGE’ OF VENEZUELA, WHILE RUBIO STRESSES COERCING IT

- VENEZUELA’S NEW LEADER CALLS FOR DIALOGUE AND ‘COEXISTENCE’ WITH U.S.

- TRUMP WARNS COLOMBIA IN THREAT TO OTHER DRUG-PRODUCING COUNTRIES

- DENMARK TELLS TRUMP TO STOP THREATENING GREENLAND

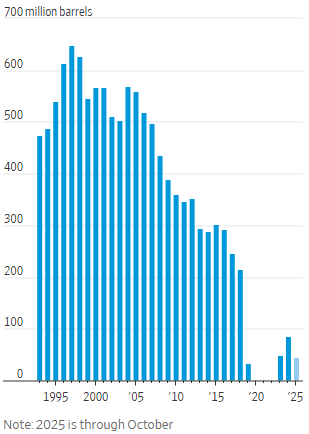

Figure 1: US imports of Venezuelan crude oil and petroleum products, annually

Source: Energy Information Administration, graphic via WSJ

NEWS

MNI POLITICAL RISK ANALYSIS: Political Event Calendar 2026

In our Political Risk calendar for 2026, we include details on the major political events scheduled to take place in developed and emerging markets over the course of the next 12 months. We only include those events that have a set date or period in which they will take place. The known dates outlined in the table below, combined with unconfirmed but expected events and the ever-present prospect of ‘black swan’ shocks, will ensure that political risks continue to have a significant impact on financial, commodity and credit markets through 2026.

MNI SOVEREIGN RATING REVIEW CALENDAR 2026

Please use the above link to access the indicative 2026 sovereign rating review schedules across the five most prominent rating agencies (Fitch, Moody's, S&P, Morningstar DBRS & Scope Ratings). Note that the schedules are indicative only and ratings can be reviewed on an ad-hoc basis. Rating agencies may also adjust their schedules during the year.

US/VENEZUELA (NYT): Trump Says U.S. Is ‘In Charge’ of Venezuela, While Rubio Stresses Coercing It

President Trump on Sunday night asserted again that the United States was “in charge” of Venezuela, hours after his top diplomat had pivoted away from such earlier suggestions of direct control to say that the administration would instead coerce cooperation from the new leadership in Caracas. “We’re dealing with the people that just got sworn in,” Mr. Trump told reporters as he flew back to Washington from Florida. “And don’t ask me who’s in charge, because I’ll give you an answer, and it’ll be very controversial.” “What does that mean?” a reporter asked. “It means we’re in charge,” the president said. Mr. Trump did not provide details, but he appeared to be referring to control over the Venezuelan government, whose top officials made defiant statements after the U.S. military entered the country early Saturday and seized Nicolás Maduro, the autocratic leader.

US/VENEZUELA (NYT): Venezuela’s New Leader Calls for Dialogue and ‘Coexistence’ With U.S.

Acting President Delcy Rodríguez struck a more diplomatic tone than she had on Saturday, inviting the United States to “work together on a cooperative agenda.” A day after a blistering speech in which she accused the Trump administration of illegally kidnapping Nicolás Maduro, Venezuela’s head of state, the country’s new acting president, Delcy Rodríguez, released a statement on Sunday night striking a much more diplomatic tone. In a statement posted on social media, Ms. Rodríguez said that Venezuela “aspires to live without external threats” and “has a right to sovereignty.” But she continued in a more conciliatory tack.

US/COLOMBIA (BBG): Trump Warns Colombia in Threat to Other Drug-Producing Countries

President Donald Trump warned other drug-producing nations in the Western Hemisphere that he wouldn’t long tolerate the flow of illegal substances to the US. A day after US forces captured Venezuelan leader Nicolas Maduro to stand trial in the US, Trump said several other nations need to change their ways. “Colombia is very sick, too, run by a sick man who likes making cocaine and selling it to the United States and he’s not going to be doing it very long, let me tell you,” Trump told reporters Sunday evening aboard Air Force One.

OIL (WSJ): Why Oil Prices Are Barely Moving After the Venezuelan Incursion

Oil futures fell Sunday night to start the first trading session since the U.S. ousted Venezuelan strongman Nicolás Maduro and President Trump subsequently pledged to dispatch American drillers to revive the country’s crude output. U.S. futures for delivery later this month shed 0.5%, trading at about $57 a barrel after the open Sunday in New York. Brent crude futures were down by even less, trading around $60.50. The move in oil markets reflects expectations among energy traders that significant obstacles remain before Venezuelan oil is flowing more freely into global markets. Sanctions applied to pressure Maduro’s regime have been a pillar of support for oil prices that have been depressed by a growing surfeit.

US/DENMARK (BBG): Denmark Tells Trump to Stop Threatening Greenland

Denmark’s prime minister urged Donald Trump to stop threatening to take control of Greenland as the US president’s move to run Venezuela set alarm bells ringing in the Nordic nation about America’s military ambitions. Mette Frederiksen’s comments came in response to Trump’s renewed assertion on Sunday that the US needs Greenland, a semi-autonomous territory within the Danish kingdom, for defense purposes. “I need to say this very directly to the US,” Frederiksen said in a statement. “The US has no right to annex any of the three countries of the Kingdom of Denmark.”

US/TURKEY (BBG): Erdogan Says Turkish Return to F-35 Program Key to NATO Security

President Recep Tayyip Erdogan called for Turkey’s re-entry into the US-led F-35 fighter jet-program, saying it would help cement ties with Washington and strengthen the security of NATO. The written comments, made in a response to questions from Bloomberg, highlight the Turkish leader’s bid to use his rapport with President Donald Trump to repair ties strained almost a decade ago over Turkey’s purchase of Russian-made air defense systems.

FRANCE (FT): French Far Right Courts Business Leaders as It Prepares for Power

France’s far-right leaders Jordan Bardella and Marine Le Pen are courting business leaders and international investors keen to prepare for the possibility that Rassemblement National may come to power. Leading figures at Cac 40 companies have stepped up their engagement with RN — a link once considered taboo — with one senior board member describing it as a “duty” to influence a political force that is leading in opinion polls. At business lunches in Paris, the party is now taken far more seriously by a business class keen to steer it towards a more liberal economic platform.

UK (MNI): UK Labour Market Could Weaken in 2025 - Think Tank

The UK labour market risks weakening this year due to high interest rates and above-inflation increases to the minimum wage, the Resolution Foundation think tank said in a press release on Monday. "The short-term impact could be job displacement and higher unemployment," it said, though it added that there are signs that these factors will allow more productive companies to outcompete struggling firms. The "early effects of AI" may also already be visible, it said.

CHINA (MNI): Chinese Interests in Venezuela Protected by Law - MoFA

MNI (London) China's Xinhua reports comments from Ministry of Foreign Affairs spox Lin Jian in a press conference earlier today, stressing that Beijing views existing contracts between the Chinese and Venezuelan gov'ts as still operational and subject to international law: "No matter how the political situation in Venezuela changes, China's willingness to deepen pragmatic cooperation in various fields will not change, and China's legitimate interests in Venezuela will be protected in accordance with the law." The comments come in the context of the US military operation that removed Venezuelan President Nicolas Maduro from power and detained him on drug trafficking charges.

THAILAND (BBG): Thai Central Bank Ready to Adjust Monetary Policy if Needed

The Bank of Thailand’s Monetary Policy Committee says monetary policy should remain accommodative to support economic recovery and stands ready to adjust monetary policy as appropriate, in line with the evolving economic and inflation outlook. At the same time, it was important to ensure macro-financial stability, while taking into account the limited policy space to absorb potential economic shocks arising from heightened uncertainty in the global economy and financial markets, according to the committee’s edited minutes released on Monday.

DATA

UK DATA (MNI): Lending on the Stronger Side in Nov, Mortgage Approvals in Line

- UK NOV M4 MONEY SUPPLY +0.8% M/M, +4.3% Y/Y

- UK BOE NOV SECURED LENDING GBP4.49 BLN

- UK BOE NOV MORTGAGE APPROVALS 64,530

- UK BOE NOV CONSUMER CREDIT GBP2.08 BLN

UK net mortgage lending increased to GBP4.5bln in November, on the stronger side of expectations, while mortgage approvals again printed broadly in line with consensus and historical norms. Net consumer credit increased to GBP2.08bln, nearly 1bln above consensus. The release points to continued housing market resilience and stronger demand for consumer credit towards the end of 2025. Data from the BoE show net lending on dwellings increased to GBP4.49bln, above consensus of 4.1bln, after a slightly downward revised GBP4.16bln (initially 4.27bln) in October. New mortgage approvals came in at 64.5k, broadly in line with consensus of 64.0k, and still trending in line with the historical average.

SWITZERLAND DATA (MNI): Moderate October Retail Sales

- SWISS NOV RETAIL SALES +0.1% M/M, +2.3% Y/Y (VS +0.2% M/M, +2.2% Y/Y OCT)

Retail sales data underpins the narrative that the Swiss consumer is in solid shape and, barring new shocks, the SNB is likely to hold its policy rate at 0% for the foreseeable future. The series continued Q4 growing marginally, at 0.1% M/M in November (0.2% October, revised from 0.7%). Looking at the drivers of the release shows limited moves within the subcategories, with auto fuel standing out positively, at 0.8% M/M (1.3% prior). However, over the last couple of months, none of the main subseries have exhibited a clear directional trend on a M/M basis.

FOREX: USD Tilts Higher Amid Venezuela Uncertainty, Oil Tied FX Pressured

- The fallout from Venezuela remains difficult to parse for G10 FX, which are instead following cross-market cues via higher precious metals and rallying equities (IT and industrials outperform thanks to tech strength in Asia as well as ASML's 3.5% rally on a Bernstein upgrade).

- The USD's continued recovery off the late December lows nicely coincides with the formation of a golden cross (50-dma > 200-dma), pointing to potential corrective activity in the USD Index's 1% rally since Christmas.

- We noted the distinct pressure on front-end implied vols across G10 FX in the lead-up to Christmas (even when seasonals were accounted for), and little has changed. EUR 3m vols remain trending lower, with JPY the sole standout in vol space.

- Oil-sensitive FX is underperforming as crude softens despite the significant uncertainty over Venezuela’s oil production capability after the capture of Maduro.

- As such, USDCAD upward pressure comes via both legs of the trade, making light work of its 20-day EMA, narrowing the gap to the 1.3806 December 19 high. From a technical perspective, a bear theme remains intact for now, with key short term support at 1.3643 but short-term the corrective bounce may extend.

- USDNOK expectedly also sees gains this morning but remains within its December range, with resistance at 10.2429, the December 18 high.

- Key focus is on any cues if the US will be able to secure power over Venezuela and if further intervention may be needed to achieve that given some question marks on now acting president Delcy Rodriguez.

- Elsewhere, ISM Manufacturing highlights the data calendar for today while markets await Friday's December employment report. This will be the last NFP release before the FOMC's end-January meeting, at which participants would probably require substantially weaker-than-expected figures to spur even consideration of a another 25bp cut.

EGBS: Bunds Pare Early Gains, Trend Condition Bearish

- The trend condition in Bunds remains bearish, with futures having pared early morning gains. Currently +5 ticks at 127.16, support and the bear trigger in Bunds is located at 126.75.

- The move away from today’s 127.31 high may have been a function of solid corporate supply and an uptick in European equities. Crude oil futures have been volatile, with markets still digesting the implications of the US’ special operation in Venezuela over the weekend.

- The German curve is bull flatter, with 30-year yields down 2bps. That leaves 5s30s down almost 2bps to 104.5bps. However, trendline support drawn from the April 2025 low remains intact.

- Long-end swap spreads are little changed. One focus for EUR rates markets in H1 is the impact of Dutch pension fund flows, with several funds having transitioned to a defined contribution scheme from January 1.

- 10-year EGB spreads to Bunds have unwound earlier narrowing, now up to +1bp wider on the session.

- In supply, Slovenia is holding a 10-year syndication today, and we remain on the lookout for start-of-year mandates from several Eurozone countries. Conventional auction supply kicks off tomorrow with Germany.

- This afternoon’s calendar includes the US ISM manufacturing report, with regional focus on tomorrow’s December flash inflation data from France and Germany.

Figure 1: German 5s30s Curve (Source: Bloomberg Finance L.P)

GILTS: Yields Edge Lower as Geopolitics Dominate, 2s10s Nearer to '25 High

Gilts are a little firmer on the day, with wider core global FI off Asia/Friday lows.

- Geopolitical risks centred on the U.S. seizing Venezuelan President Maduro seemed to provide some background support for core global FI markets as European participants filtered in, with lower oil prices tied to a potential longer run uptick in Venezuelan crude also providing support (albeit with plenty of uncertainty evident on that front).

- However, the impending seasonal surge in both sovereign and corporate supply, coupled with a recovery from lows in oil markets, has limited the rally.

- Gilt futures +16 at 90.94. Key directional triggers remain at 90.50 & 91.93.

- Yields 2-3bp lower across the curve, bull steepening.

- 2s10s breaks above the Nov high (80.305bp), exposing the Sep high (83.794bp) which protects the ’25 top (84.583bp).

- A dovish drift seen in GBP STIRs alongside the move further out the curve. SONIA futures flat to +2.5, BoE-dated OIS pricing ~41bp of easing through year-end vs. ~39bp late Friday.

- UK lending data was a little firmer than expected.

- Final services PMI is due tomorrow, while the DMO’s ’26 supply schedule will get underway on Wednesday, via GBP4.25bln of the 4.125% Mar-31 gilt.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Feb-26 | 3.711 | -1.5 |

Mar-26 | 3.621 | -10.5 |

Apr-26 | 3.508 | -21.8 |

Jun-26 | 3.438 | -28.8 |

Jul-26 | 3.364 | -36.2 |

Sep-26 | 3.343 | -38.3 |

Nov-26 | 3.315 | -41.0 |

Dec-26 | 3.315 | -41.1 |

EQUITIES: Fresh Cycle Highs for Eurostoxx Futures Reinforce Bullish Theme

A bull cycle in Eurostoxx 50 futures remains intact and a fresh cycle high today, reinforces the bull theme and confirms a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 5935.01 next, a Fibonacci projection. On the downside, initial firm support is seen at 5762.47, the 20-day EMA. Short-term weakness in S&P E-Minis appears corrective. A key short-term support has been defined at 6771.50, the Dec 18 low. Clearance of this level is required to signal scope for a deeper retracement and would also highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the primary uptrend.

- Japan's NIKKEI closed higher by 1493.32 pts or +2.97% at 51832.8 and the TOPIX ended 68.55 pts higher or +2.01% at 3477.52.

- Elsewhere, in China the SHANGHAI closed higher by 54.577 pts or +1.38% at 4023.417 and the HANG SENG ended 8.77 pts higher or +0.03% at 26347.24.

- Across Europe, Germany's DAX trades higher by 213.64 pts or +0.87% at 24748.4, FTSE 100 higher by 29.32 pts or +0.29% at 9976.06, CAC 40 up 26.18 pts or +0.32% at 8220.53 and Euro Stoxx 50 up 48.89 pts or +0.84% at 5899.12.

- Dow Jones mini up 24 pts or +0.05% at 48643, S&P 500 mini up 14.25 pts or +0.21% at 6915.75, NASDAQ mini up 128 pts or +0.5% at 25519.

Time: 10:00 GMT

COMMODITIES: Gold Continues to Reverse Late-December Sell-Off

The trend condition in WTI futures remains bearish and recent gains are considered corrective. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the downtrend would signal scope for a move towards $53.77, a Fibonacci projection. Key short-term resistance is $61.25, the Oct 24 high. First resistance is at $58.47, the 50- day EMA. The trend structure in Gold is unchanged, it remains bullish and a sharp sell-off late December appears corrective - for now. The trend is overbought and a deeper retracement would allow this condition to unwind. First support at $4325.1, the 20-day EMA, has been pierced. A clear break of the average would expose the 50-day EMA at $4194.5. For bulls, a resumption of gains would open $4578.3, a Fibonacci projection.

- WTI Crude down $0.06 or -0.1% at $57.22

- Natural Gas down $0.12 or -3.32% at $3.495

- Gold spot up $102.57 or +2.37% at $4435.24

- Copper up $17.5 or +3.07% at $587.2

- Silver up $3.47 or +4.76% at $76.278

- Platinum up $83.79 or +3.91% at $2230.24

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 05/01/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/01/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 05/01/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/01/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 06/01/2026 | 2200/0900 | * | S&P Global Services PMI (f) | |

| 06/01/2026 | 2200/0900 | ** | S&P Global Composite PMI (f) | |

| 06/01/2026 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 06/01/2026 | 0745/0845 | *** | HICP (p) | |

| 06/01/2026 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0815/0915 | ** | S&P Global Composite PMI (f) | |

| 06/01/2026 | 0815/0915 | ECB Cipollone Chairs Intl Monetary System Panel | ||

| 06/01/2026 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0845/0945 | ** | S&P Global Composite PMI (f) | |

| 06/01/2026 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0850/0950 | ** | S&P Global Composite PMI (f) | |

| 06/01/2026 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0855/0955 | ** | S&P Global Composite PMI (f) | |

| 06/01/2026 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 06/01/2026 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0900/1000 | ** | S&P Global Composite PMI (f) | |

| 06/01/2026 | 0930/0930 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0930/0930 | *** | S&P Global/CIPS Composite PMI (f) | |

| 06/01/2026 | 1300/1400 | *** | Germany CPI (p) | |

| 06/01/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 06/01/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 06/01/2026 | 1445/0945 | *** | S&P Global Services PMI (f) | |

| 06/01/2026 | 1445/0945 | *** | S&P Global Composite PMI (f) |