MNI US OPEN - US Shutdown Enters 7th Day as Standoff Continues

EXECUTIVE SUMMARY

- TRUMP SAYS HE’S OPEN TO NEGOTIATING WITH DEMOCRATS, THEN BACKTRACKS

- MACRON SEEKS LAST-DITCH TALKS TO SALVAGE FRANCE’S GOVERNMENT

- SCHMID SAYS FED MUST MAINTAIN CREDIBILITY ON INFLATION

- MNI RBNZ PREVIEW - HOW MUCH TO EASE?

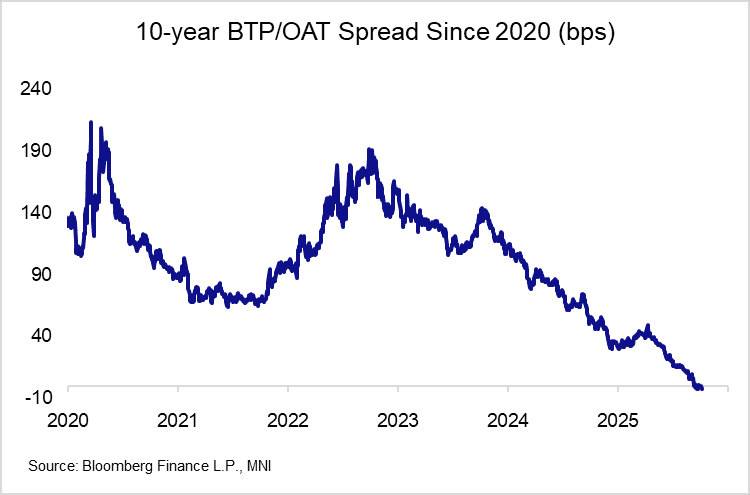

Figure 1: French political woes favour further IT/FR spread tightening

NEWS

US (NYT): President Says He’s Open to Negotiating, Then Backtracks

With the government shut down for a sixth day, President Trump briefly dangled the possibility of a negotiation with Democrats, only to pull back several hours later — insisting that Democrats must end the standoff first before he would be willing to make a deal on health care. Earlier, he had suggested that he was open to a deal on the extension of Affordable Care Act subsidies, the first indication that he was willing to negotiate.

US (Politico): Trump Administration Weighs Selling Parts of $1.6t Federal Student Loan Portfolio

Trump administration officials are exploring options to sell off parts of the federal government's $1.6 trillion student loan portfolio to the private market, according to three people familiar with the matter. The discussions have taken place among senior Education Department and Treasury Department officials and have focused on selling high-performing portions of the government’s massive portfolio of student debt, which is owed by about 45 million Americans.

FED (MNI): Schmid Says Fed Must Maintain Credibility on Inflation

Kansas City Fed President Jeff Schmid said Monday that monetary policy must remain restrictive in the face of an inflation path that remains unacceptably elevated. "With inflation still too high, monetary policy should lean against demand growth to allow the space for supply to grow and relieve price pressures in the economy," Schmid said according to prepared remarks.

FRANCE (BBG): Macron Seeks Last-Ditch Talks to Salvage France’s Government

President Emmanuel Macron gave his outgoing prime minister, Sebastien Lecornu, until Wednesday night to negotiate with France’s political parties in a last-ditch effort to prevent the country from falling deeper into crisis. Lecornu unexpectedly resigned early Monday, blaming the intransigence of antagonistic political groups — including Macron’s centrist minority — for their failure to agree to a new cabinet, which was unveiled Sunday evening.

FRANCE (MNI): Macronist Former PM Calls for Early Presidential Election

Former Prime Minister Edouard Philippe has publicly called for presidential elections to be brought forward from mid-2027 to try and break the current political crisis that is set to claim France's third prime minister in less than a year. Philippe's intervention is a notable one. Opposition figures have frequently called for President Emmanuel Macron to stand down and call a snap election. However, Philippe not only hails from the centrist bloc of parties that supports the gov't, but also served as Macron's first prime minister on coming to office in 2017.

JAPAN (BBG): Japan 30-Year Bond Sale Demand Calms Nerves After Market Jolt

Japan’s 30-year sovereign bond auction demand was firm enough to calm a jittery market following the surprise victory of pro-stimulus conservative Sanae Takaichi in the ruling party leadership race. The bid-to-cover ratio, a key measure of demand, was 3.41, compared with 3.31 at the previous auction and a 12-month average of 3.37. Government bond futures pared losses after the result, and the 30-year bond yield fell 5 basis points to 3.235%.

MNI RBNZ PREVIEW - OCTOBER 2025: How Much to Ease?

After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October. The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August. 36bps of easing is priced for Wednesday’s meeting, with a cumulative 63bps by November 2025.

DATA

GERMANY DATA (MNI): August Factory Orders Weak, Driven by Foreign Sector

- GERMANY AUG FACTORY ORDERS -0.8% M/M (VS -2.7% JUL)

August manufacturing orders (-0.8% M/M vs 1.2% consensus) were driven by weak developments in the foreign sector which more than outweighed some recovery in domestic orders. A minor July revision (now -2.7% from -2.9% unrevised) does not move the needle. "When large-scale orders are excluded, new orders were 3.3% lower than in the previous month. The less volatile three-month on three-month comparison showed that new orders in the period from June 2025 to August 2025 were 2.3% lower than in the previous three months; when large-scale orders are excluded, new orders were down 2.0%.", Destatis comments.

FRANCE DATA (MNI): Export Growth Recovering But Momentum Weak

The French trade deficit was E5.53bln in August, down from E5.74bln in July (revised from E5.56bln initial) and a year-to-date high of E7.42bln in February. Assuming unchanged nominal GDP growth of ~0.5% Q/Q in Q3, this implies a steady goods trade deficit of around 2.7% GDP. Imports fell 0.4% M/M for the second consecutive month, a sign of continued weakness in domestic demand against a backdrop of ongoing political/fiscal/economic uncertainty. However, Y/Y import growth continues to slowly recover from the 2023 lows, trending back toward pre-covid growth rates.

NORWAY DATA (MNI): Manufacturing Production Momentum Down in Q3, But Growth Still Positive

Norwegian manufacturing industrial production momentum has fallen from the highs seen in Q2, but continues to exhibit positive growth. Manufacturing production rose 0.7% M/M in August, with July's reading revised up four tenths to 0.4%. That left 3m/3m growth at 0.3% (vs 0.4% in July, 2.3% in June). Sentiment gauges (e.g. Regional Network Survey, Stats Norway business confidence and the manufacturing PMI) are consistent with positive production in the coming months.

CHINA DATA (MNI): FX Reserves at Multi Year Highs, Consensus Is for Higher CNY

China markets remain closed until Thursday for National Day celebrations, but we have seen Sep FX reserves figures print. The headline rose to $3338.66bn, from $3322.15bn in August. This is the highest levels for FX reserves since end 2015, see the chart below. At face value this supports the backdrop of generally improved capital flow/strong current account picture as 2025 has unfolded. The general sell-side consensus is for stronger yuan levels as we approach year end, which fits with this backdrop. The consensus via BBG is for USD/CNY hit 7.1000 by year end, then 7.08 by end Q1 next year.

JAPAN DATA (MNI): Household Spending Above Forecasts, Supports BoJ Hike Plans

Japan household spending for August was stronger than forecast (+2.3%y/y, versus 1.2% forecast, 1.4% prior). We are below earlier 2025 highs from a y/y momentum standpoint, but the trend has steadily improved from late 2024 lows. It should add, albeit at the margins, to the case for a further BoJ rate hike, although little is priced for the Oct meeting (implied rate of 0.52%, versus a current effective rate of 0.477%).

AUSTRALIA DATA (MNI): Stall in Disinflation Weighing on Consumer Confidence

Westpac consumer confidence fell for the second straight month in October as higher inflation prints appear to have weighed on assessments of family finances and the economy. Thus, Q3 CPI on 29 October is likely to be important for households too. The RBA's decision to leave rates at 3.6% and cautious tone appear to have actually reassured consumers. Sentiment was down 3.5% m/m to 92.1, the lowest in 6 months. Households remain cautious but are prepared to spend at the right price. Q3 expenditure growth improved compared to Q2 with signs of a pickup in discretionary spending.

FOREX: EURJPY Pressed Higher Despite Ongoing French Woes

- The initial fade in the JPY on Monday stalled as advisor Honda talked up governmental support for a December BoJ rate hike, however the currency is on the back foot again early Tuesday, helping usher in new weekly highs for USDJPY at 150.83. The move narrows the gap with key resistance and the bull trigger in the pair at 150.92, clearance above which puts prices at the best level since late March. Takaichi's victory in the LDP leadership race remains the primary driver here, with local press focusing on her negotiations with junior coalition partners - who oppose her more conservative political views.

- EURJPY's rally to new alltime highs this week is largely holding, with Tuesday seeing a 176.35 print, however ongoing fiscal and political concerns in France will be containing the strength. Implied EUR vols are steadying and appear to have halted their multi-month downtrend in the front-end. Calls for early Presidential and legislative elections in France to clear the political logjam have been rising - an unlikely occurrence in the very near-term, but a growing possibility given the government's inability to proceed with an acceptable budget.

- NZD is the poorest performing currency on the day, with AUD not far behind. Price action comes ahead of the RBNZ rate decision on Wednesday, at which markets are split between expecting a 25bps rate cut, or something more sizeable. Consumer confidence data in Australia also deteriorated, dragging AUDUSD toward the weekly lows of 0.6582.

- The ongoing US government shutdown keeps data further delayed, meaning today's trade balance data for August is unlikely to be released (and may have spillover impacts on the Canadian trade balance statistics, which are cross-referenced against the US numbers). As such, the speaker schedule is likely to be of more market importance: Fed's Bostic, Bowman, Miran & Kashkari are all set to appear and may shed some insight into the Fed's views on the shutdown ahead of the Minutes release tomorrow. ECB's Nagel & Lagarde are also on the calendar.

EGBS: German Curve Steepening Resumes; Supply and French Politics in Focus

The German curve has bear steepened this morning, with yields flat to 2.5bps higher. Although the 5s30s curve has traded in a broadly sideways direction since the September ECB decision, the Sep 12 low of 93.4bps has contained downside and allowed a longer-term steepening theme to remain intact. The curve is back above 100bps at typing (+1.2bps today).

- 10-year yields remain within the familiar 2.60-2.80% range, currently +1.5bps at 2.733%.

- Bund futures are -19 ticks at 128.37 on lighter-than-usual volumes, close to yesterday's 128.31 low. German factory orders were weaker-than-expected this morning, but there’s been more focus on today’s sovereign supply and French political headlines.

- After resigning as French PM yesterday, Lecornu has been invited by President Macron to hold 48 hours of emergency talks to try and gain support for the 2026 budget. Prospects appear bleak, keeping French political/fiscal risks top of mind.

- Germany will sell E4.5bln of the 2.20% Oct-30 Bobl at 1030BST, while today’s RAGB auction saw very strong demand across the two lines on offer. The EU is holding a dual tranche 7/15-year syndication today.

- 10-year EGB spreads to Bunds are mixed, with OATs and BTPs up to 1bp wider on the session.

- The US Government shutdown is ongoing, so no data is due this afternoon. ECB President Lagarde and Bundesbank President Nagel will speak this evening – no changes in stance are expected.

GILTS: Curve Bear Steepens, PGT Sees Strong Demand

Gilts hold lower on the day, with this week’s political developments in both France & Japan resulting in bear steepening of core global FI curves.

- Futures have pierced Monday lows, basing at 90.38 before recovering above 98.40.

- Bears remain in technical control, with initial support and resistance still located at 90.26 & 91.28.

- Yields 0.5-2.5bp higher, curve steeper.

- 10s last ~4.75%, still operating within the multi-week 4.60-4.80% closing range.

- Both 2s10s and 5s30s remain in their steepening trends, even after September’s flattening.

- The DMO’s GBP1.25bln sale of the 0.125% Jan-28 gilt via PGT saw strong demand metrics (aided by the easily digestible size), with the line rallying by 1bp in the time since the tender.

- Fiscal matters continue to dominate domestic news flow.

- Former BoE MPC member Saunders told BBG that inflation will provide the government with a net GBP5bln of additional revenue, although that is hardly positive news for households.

- Weakness in the long end has fed into GBP STIRs. SONIA futures flat to 2.5 lower, range lows in SFIZ5 and SFIZ6 remain untested on the day.

- BoE-dated OIS pricing just under 5bp of easing through year-end, we continue to suggest that markets are underpricing the odds of a Q4 rate cut.

- Little of note on the UK calendar for the remainder of the day. Note that BoE chief economist Pill will speak on Wednesday.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.961 | -0.1 |

Dec-25 | 3.919 | -4.8 |

Feb-26 | 3.814 | -15.3 |

Mar-26 | 3.786 | -18.1 |

Apr-26 | 3.712 | -25.5 |

Jun-26 | 3.691 | -27.6 |

Jul-26 | 3.644 | -32.4 |

Sep-26 | 3.632 | -33.5 |

EQUITIES: Bullish Theme in E-Mini S&P Intact, Sights on $6812.29 Proj. Level

Eurostoxx 50 futures remain in a bull-mode condition. Last week’s gains resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position too, highlighting a dominant uptrend. Initial firm support is 5525.00, Aug 22 high. A bull cycle in S&P E-Minis remains intact. The contract traded to a fresh cycle high last week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6694.17. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6575.48.

- Japan's NIKKEI closed higher by 6.12 pts or +0.01% at 47950.88 and the TOPIX ended 1.85 pts higher or +0.06% at 3227.91.

- Across Europe, Germany's DAX trades lower by 31.66 pts or -0.13% at 24350.3, FTSE 100 higher by 9.68 pts or +0.1% at 9488.7, CAC 40 down 4.88 pts or -0.06% at 7966.9 and Euro Stoxx 50 down 4.83 pts or -0.09% at 5623.89.

- Dow Jones mini down 102 pts or -0.22% at 46856, S&P 500 mini down 8.5 pts or -0.13% at 6780.5, NASDAQ mini down 26.25 pts or -0.1% at 25159.

Time: 10:00 BST

COMMODITIES: Fresh Cycle Highs in Gold Reinforces Current Conditions

WTI futures remain in a bear-mode condition and gains are considered corrective. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens a bearish theme and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal. A bull cycle in Gold remains in play and Monday’s fresh cycle high, reinforces current conditions. This maintains the price sequence of higher highs and higher lows. Furthermore, momentum studies highlight a condition known as momentum drag - where momentum studies remain in overbought territory and move sideways - a bullish signal. Sights are on $3987.3 next, a Fibonacci projection. Support to watch lies at $3753.2, the 20-day EMA.

- WTI Crude down $0.11 or -0.18% at $61.6

- Natural Gas up $0.04 or +1.04% at $3.394

- Gold spot down $7.78 or -0.2% at $3951.39

- Copper up $2.4 or +0.48% at $506.05

- Silver down $0.3 or -0.61% at $48.186

- Platinum down $10.18 or -0.63% at $1613.01

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 07/10/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 07/10/2025 | 1400/1000 | * | Ivey PMI | |

| 07/10/2025 | 1405/1005 | Fed's Miki Bowman | ||

| 07/10/2025 | 1430/1030 | Fed Governor Stephen Miran | ||

| 07/10/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/10/2025 | 1530/1130 | Minneapolis Fed's Neel Kashkari | ||

| 07/10/2025 | 1610/1810 | ECB Lagarde Speech at Business France Event | ||

| 07/10/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 07/10/2025 | 1900/1500 | * | Consumer Credit | |

| 07/10/2025 | 2005/1605 | Fed Governor Stephen Miran | ||

| 08/10/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 08/10/2025 | 2330/0830 | ** | Average Wages (p) | |

| 08/10/2025 | 2350/0850 | Balance of Payments | ||

| 08/10/2025 | 0100/1400 | *** | RBNZ official cash rate decision | |

| 08/10/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/10/2025 | 0600/0800 | ** | Industrial Production | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 08/10/2025 | 1030/1230 | ECB Elderson In Panel at Finance Conference | ||

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr | ||

| 08/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 08/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 08/10/2025 | 1500/1600 | BOE Pill Speech at University of Birmingham | ||

| 08/10/2025 | 1600/1800 | ECB Lagarde Video Message at Werner Report Event | ||

| 08/10/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 08/10/2025 | 1800/1400 | FOMC Minutes | ||

| 08/10/2025 | 1915/1515 | Minneapolis Fed's Neel Kashkari | ||

| 08/10/2025 | 2145/1745 | Fed Governor Michael Barr |

Note: Due to U.S. government shutdown, some data may be unavailable.