MNI US OPEN - US, Iran Start Second Round of Nuclear Talks

EXECUTIVE SUMMARY

- SECOND ROUND OF INDIRECT US-IRAN NUCLEAR TALKS UNDERWAY IN GENEVA

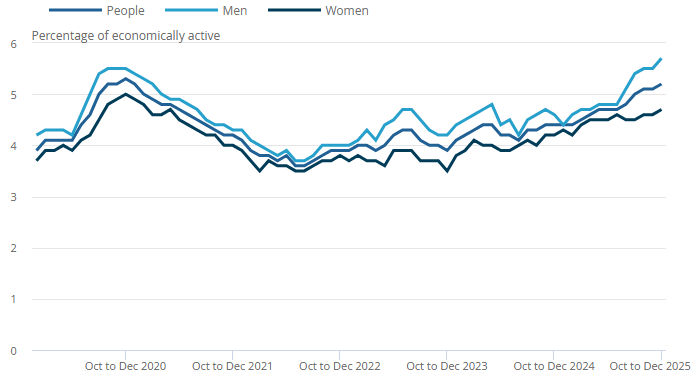

- UK UNEMPLOYMENT RATE AT POST-PANDEMIC HIGH 5.2%

- UKRAINE AND RUSSIA HOLD PEACE TALKS, BUT EXPECTATIONS ARE LOW

- MNI RBNZ PREVIEW: ON HOLD, HIKE TIMING KEY FOCUS

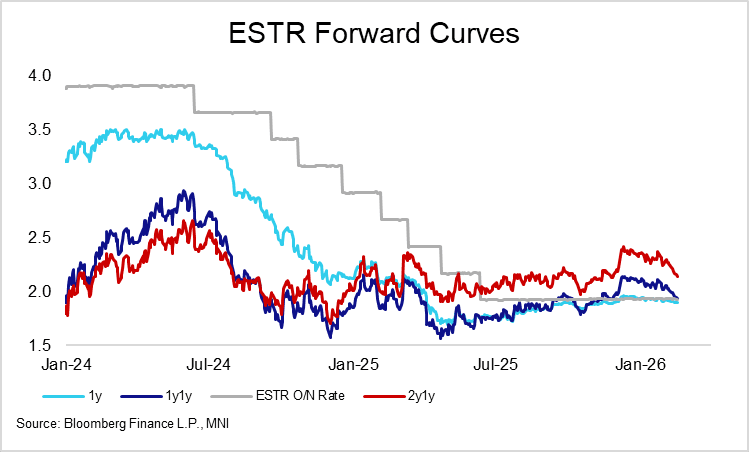

Figure 1: Implied probability of another ECB cut continues to inch higher

Figure 2: UK unemployment rate rises to 5-year high

Source: ONS

NEWS

US/IRAN (MNI): Second Round of Indirect US-Iran Nuclear Talks Underway in Geneva

A second round of indirect nuclear talks between the US and Iran is underway in Switzerland. Reuters reports that a senior Iranian official said ahead of talks, "the key to sustaining effective talks is US seriousness on lifting sanctions and avoiding unrealistic demands." The official adds that Iran's approach to talks with the US is "positive and serious", but it has no preconceptions about the outcome. The official echoes yesterday's statement from Foreign Minister Abbas Araghchi, saying "Iran is in Geneva with genuine, constructive proposals," but appearing to manage expectations of a breakthrough. The comments suggest Tehran is maintaining a hardline posture going into talks, likely assessing the US is wary of committing to a military operation, despite the large-scale mobilisation of defensive assets to the region. The comments indicate Tehran is unlikely to offer flexibility on US demands to expand talks to cover the range of Iran's ballistic missile programme and its support for regional proxy groups.

US/CUBA (BBG): Trump Says Rubio in Talks With Cuba as It Faces Economic Crisis

President Donald Trump said that US government officials, including Secretary of State Marco Rubio, are in discussions with Cuba’s Communist regime as the island nation faces worsening economic conditions. “We’re talking to Cuba right now, and Marco Rubio is talking to Cuba right now,” Trump told reporters on Monday. Cuba should “absolutely make a deal because it’s a humanitarian threat,” Trump told reporters aboard Air Force One. “In the meantime, there’s an embargo, there’s no oil, there’s no money, there’s no anything.”

RUSSIA/UKRAINE (NYT): Ukraine and Russia Hold Peace Talks, but Expectations Are Low

Ukrainian and Russian officials planned to meet on Tuesday in Switzerland for a new round of U.S.-brokered peace talks, but hopes of a breakthrough to end the war were low. Fighting rages on, past negotiations have produced little, and major hurdles to a deal are unresolved. The talks marked the third trilateral meeting between Ukrainian, Russian and American negotiators in roughly as many weeks. Ukraine and Russia have described two previous rounds of discussions in the United Arab Emirates as productive. But those talks delivered scant progress beyond a prisoner-of-war exchange, as the conflict enters its fifth year later this month.

NORWAY (MNI INTERVIEW): Global Competition Caps Norway Wages - Stats Head

The head of Statistics Norway and pay advisory chair Geir Axelsen tells MNI about the background for pay settlements. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

FRANCE/INDIA (BBG): Macron Pushes Fighter Jet Deal on High-Profile India Trip

French President Emmanuel Macron is pulling out all the stops to court Indian Prime Minister Narendra Modi and persuade him to buy French fighter jets, beginning his fourth visit to India since his election in 2017 with considerable fanfare. The trip comes as India moves closer to purchasing 114 Rafale jets in what would be one of its largest air force upgrades in recent years. Earlier this month, a committee chaired by the Indian defense minister cleared the acquisition, though several steps remain before a formal contract is signed, including negotiations over price and local production.

JAPAN (RTRS): Japan's Debt Issuance to Surge 28% in Fiscal 2029 from 2026, Finance Ministry Estimates

Japan's annual bond issuance will likely surge 28% three years from now due to rising debt-financing costs, a finance ministry estimate reviewed by Reuters showed on Tuesday, casting doubt on Prime Minister Sanae Takaichi's argument that the country can deliver tax cuts without boosting debt. Under the estimate, Japan would need to issue up to 38 trillion yen ($248.32 billion) worth of bonds in the fiscal year starting in April 2029 to fill a hole from expenditures surpassing tax revenues, up from 29.6 trillion yen in fiscal 2026.

BOJ (BBG): BOJ Likely to Raise Key Rate in April, Ex-Board Member Says

The Bank of Japan is likely to seize on a raft of new data available in April as an opportunity to raise its benchmark interest rate, looking past rumblings in the market over the possibility of a move in March, according to a former BOJ board member. “A rate hike in March would entail risk, as it would be based on expectations, not confirmation,” Seiji Adachi said Monday in an interview. “They’ll have a lot of data they can use to confirm improvement in underlying inflation in April.” Adachi’s view is consistent with growing market expectations that Governor Kazuo Ueda’s board may move in the spring — sooner than most economists predicted after the last rate hike in December.

RBA (MNI): RBA Board Sees Persistent Inflation - Minutes

Reserve Bank of Australia board members judged inflation remained too high, with underlying price pressures running above the central projection from six months earlier, a key factor behind the decision to lift the cash rate 25 basis points to 3.85% earlier this month, published minutes showed Tuesday. Members noted staff assessed that while much of the recent inflation rise reflected less-persistent factors that should fade, a meaningful share stemmed from underlying pressures likely to persist under current policy. As a result, the central inflation forecast was revised materially higher, remaining above target through 2026 and returning close to the 2.5% midpoint only around mid-2028, assuming the cash rate follows the market path.

MNI RBNZ PREVIEW: On Hold, Hike Timing Key Focus

At tomorrow’s RBNZ meeting the central bank is widely expected to keep rates on hold. The Bloomberg survey of sell-side economists shows all 22 economists see the policy rate being held at 2.25%. Our strong bias is also for no change tomorrow. If realized, this will leave the focus firmly on the outlook, particular on the RBNZ’s new OCR path. The other focus point will be gauging new RBNZ Governor Breman’s tone, as this will be her first rate setting meeting in charge. The RBNZ will also likely be cautious around sounding too hawkish around the outlook, which the market will likely judge via the implied OCR outlook path.

DATA

UK DATA (MNI): Unemployment Rate Rises to 5-Year High, Downward Revision to Nov Single-Month Wage Data

- UK DEC AWE PRIVATE REGULAR PAY +3.43% 3MO Y/Y (VS +3.56% NOV)

- UK DEC 3MO EMPLOYMENT CHANGE +52K (VS +82K NOV)

- UK JAN PAYE PAYROLLS TOTAL EMPLOYEES 30.28M (VS 30.29M DEC)

- UK DEC UNEMPLOYMENT RATE 5.21% (VS 5.09% NOV)

The main story in the private sector regular pay data was a 0.19pp downward revision to November's single-month reading, now estimated at 3.28% from 3.47% initial. That was key in bringing 3m Y/Y private sector pay in line with consensus and BOE forecasts. Downward revisions were seen in an all industry groups other than wholesaling, retailing, hotels & restaurants. On the employment side, the 3m employment change was +52k, below the MNI consensus of 90k and the Bloomberg consensus of 52k (and vs +82k prior). That left the 16-64 employment rate at 74.96% in the 3-months to December, down from 75.09% in the 3-months to Sep-Nov and 75.04% in Jul-Sep. The 16+ unemployment rate rose to 5.21% in the 3-months from October to December, the highest level in five years. This was up from 5.09% in the 3-months to November and 4.97% in the 3-months to September.

GERMANY DATA (MNI): Final CPI Confirms Broad-Based Services Slowdown

- GERMANY JAN FINAL CPI 2.1% Y/Y (2.1% FLASH, 1.8% DEC)

Final German CPI data, unrevised at a headline level with 0.1% M/M and 2.1% Y/Y, confirms our reading of the state-level data that the January services slowdown was broad-based. This indicates the annual repricing of a large amount of items under the category has been slower than before, an encouraging sign for the ECB's view that services inflation will moderate over the medium term. Separately, German HICP data is available for January but back data details appear to be missing. We'll comment once released in full but for now, the press release notes that HICP inflation was confirmed at -0.1% M/M and 2.1% Y/Y.

GERMANY ZEW FEB ECONOMIC EXPECTATIONS 58.3 (MNI)

GERMANY ZEW FEB CURRENT CONDITIONS -65.9 (MNI)

NEW ZEALAND DATA (MNI): Food Prices Surge In Jan, But Other Components Mostly Down M/M

For Jan, NZ food prices surged 2.5%m/m, the strongest rise monthly rise since Jan 2022. Jan does tend to be a strong month for m/m rises, with Jan 2025 seeing a 1.9%m/m gain in food prices. In y/y terms, food prices are up 4.6%, versus 4.0% in Dec, but this is still below 2025 highs of 5.0%. Outside of food, other monthly price change updates were close to flat or down on Dec outcomes.

FOREX: GBP Dips to 1.3552 Following Jobs Data, Before Recovering

- A set of softer-than-expected jobs data weighed on GBP early Tuesday, with GBPUSD having a sharp move from around 1.3610 to session lows of 1.3552. Spot has subsequently bounced back to 1.36 as we approach the NY crossover.

- GBPUSD's dip is deemed corrective at this juncture, with moving average studies continuing to highlight a dominant uptrend, and only a break of the 50-day EMA at 1.3531 would undermine the bull theme. Tomorrow's UK CPI print will also be very influential in driving short-term sentiment.

- The Japanese yen is the best performer across the G10 Tuesday, steadily reversing yesterday’s post GDP price action as a sources piece pointed away from a March hike and the softer risk sentiment across global markets also weighs at the margin.

- USDJPY has slipped back below 153.00 in sympathy and lows at 152.60/37/27 look like potential acceleration points ahead of the 152.10 yearly lows. Elsewhere, a lack of renewed optimism for the Euro has been weighing on EURJPY, prompting fresh two-month lows below 181.00 this morning, meaning the cross is testing key support at 181.22.

- The next key event for JPY may be PM Takaichi's general policy speech on Friday, which is reported to include a multi-year special budget for investment into growth initiatives and crisis management.

- NZD is slightly stronger ahead of Wednesday’s RBNZ decision, the first for newly appointed Governor Breman. Any hawkish lean would place the 0.6093 NZDUSD cycle highs back in focus.

- Fed's Barr and Daly will be interesting to watch as they speak on AI today. ECB's Escriva and Makhlouf are also scheduled to appear. In terms of data, Canada CPI for January takes focus, while Japanese trade data is scheduled overnight ahead of the RBNZ.

BONDS: 10-Year Gilt/Bund Narrows Following UK Jobs Data, Curves Bull Flatten

The 10-year Gilt/Bund spread has narrowed 2bps to 162.5bps, with UK paper outperforming German counterparts following this morning’s UK labour market data. Although wage pressures were broadly in line with consensus, the quantities side of the labour market continues to soften.

- 10-year Gilt yields are now down 4bps today at 4.359%, having pierced trendline support drawn from the November 2022 lows. Next support is the Jan 14 low at 4.336%

- Bund yields are down 2.2bps to 2.73%, taking cues from overnight moves in USTs and JGBs rather than any regional driver. The February German ZEW survey saw a weaker than expected expectations component (58.3 vs 65.2 cons, 59.6 prior), but this wasn’t a market mover.

- Both the UK and German curves have bull flattened on the session.

- In futures, Gilts are +38 ticks at 92.30. Initial resistance is the Jan 19 high at 92.51. Bund futures are +19 ticks at 129.39, with key resistance noted at the Nov 26 high of 129.55.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels. No material underperformance in RAGBs on reports that Austria is set to activate its National Escape Clause for defence spending.

- The UK is holding two tenders today, while Germany and Finland are holding conventional auctions in the EGB space. Croatia is holding a syndication for a new 10-year benchmark.

EQUITIES: Bearish Threat for E-Mini S&P Remains Present, Key Support at 6751.50

The medium-term trend condition in EuroStoxx 50 futures is unchanged, it remains bullish and the latest pullback appears corrective - for now. The contract has pierced the 6100.00 handle. A clear breach of this hurdle would open 6134.00, a Fibonacci projection point. Key support to watch lies at the 50-day EMA, at 5908.77. Clearance of this average would highlight a short-term top. A sharp sell-off on Feb 12 in S&P E-Minis reinstates a potential bearish threat leaving key resistance at 7043.00, the Jan 28 high and bull trigger, intact for now. Attention turns to the key support at 6751.50, the Feb 6 low, where a break would highlight a top and a stronger short-term reversal. This would open 6691.56, a Fibonacci retracement point. Initial resistance to watch is at 6919.38, the 50-day EMA.

- Japan's NIKKEI closed lower by 239.92 pts or -0.42% at 56566.49 and the TOPIX ended 25.83 pts lower or -0.68% at 3761.55.

- Across Europe, Germany's DAX trades higher by 64.31 pts or +0.26% at 24865.74, FTSE 100 higher by 51.21 pts or +0.49% at 10524.76, CAC 40 up 17.28 pts or +0.21% at 8333.78 and Euro Stoxx 50 up 12.62 pts or +0.21% at 5991.5.

- Dow Jones mini up 9 pts or +0.02% at 49577, S&P 500 mini down 9 pts or -0.13% at 6841.5, NASDAQ mini down 114.75 pts or -0.46% at 24688.75.

Time: 10:15 GMT (05:15 ET)

COMMODITIES: WTI Futures Test 20-Day EMA Support Again, Bull Cycle Intact

A bull cycle in WTI futures remains intact. However, the move lower from the Jan 29 high continues to highlight a corrective phase. Attention is on support at the 20-day EMA, at $62.61 (pierced). The 50-day EMA lies at $60.95. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high. Clearance of it would resume the uptrend. Recent gains in Gold highlight a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sell from the Jan 29 high continues to highlight a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent overbought condition. A resumption of bearish activity would refocus attention on $4403.0, Feb 2 low.

- WTI Crude up $0.6 or +0.95% at $63.45

- Natural Gas down $0.13 or -4.04% at $3.108

- Gold spot down $56.63 or -1.13% at $4936.21

- Copper down $8.3 or -1.42% at $577.7

- Silver down $1.67 or -2.18% at $74.9726

- Platinum down $36.71 or -1.8% at $2008.48

Time: 10:15 GMT (05:15 ET)

| Date | GMT/Local | Impact | Country | Event |

| 17/02/2026 | - | ECB de Guindos at ECOFIN Meeting | ||

| 17/02/2026 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/02/2026 | 1330/0830 | ** | Wholesale Trade | |

| 17/02/2026 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/02/2026 | 1330/0830 | *** | CPI | |

| 17/02/2026 | 1500/1000 | ** | NAHB Home Builder Index | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/02/2026 | 1745/1245 | Fed Governor Michael Barr | ||

| 17/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 17/02/2026 | 1930/1430 | San Francisco Fed's Mary Daly | ||

| 18/02/2026 | 0001/0001 | * | Brightmine Pay Deals for Whole Economy | |

| 18/02/2026 | 0030/1130 | *** | Quarterly Wage Price Index | |

| 18/02/2026 | 0100/1400 | *** | RBNZ Official Cash Rate Decision | |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report | |

| 18/02/2026 | 0700/0700 | *** | Producer Prices | |

| 18/02/2026 | 0745/0845 | *** | HICP (f) | |

| 18/02/2026 | 0900/1000 | ECB Cipollone at ABI's Executive Committee Meeting | ||

| 18/02/2026 | 1000/0500 | * | CREA Existing Home Sales | |

| 18/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/02/2026 | 1415/0915 | *** | Industrial Production | |

| 18/02/2026 | 1700/1800 | ECB Schnabel Panel at Berlin-Brandenburg Academy of Sciences and Humanities | ||

| 18/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/02/2026 | 1800/1300 | Fed's Michelle Bowman | ||

| 18/02/2026 | 1900/1400 | *** | FOMC Minutes | |

| 18/02/2026 | 2100/1600 | ** | TICS | |

| 19/02/2026 | 2350/0850 | * | Machinery orders |