MNI US OPEN - US CPI to Surge Close to 1% M/M on Energy Spike

EXECUTIVE SUMMARY

- ZELENSKIY’S TOP AIDE SEES UKRAINE NEARING A DEAL WITH PUTIN: BBG

- MNI US CPI PREVIEW: A CRUDE SHIFT FURTHER FROM TARGET

- TRUMP DEMANDS REOPENING OF HORMUZ AS US-IRAN PEACE TALKS NEAR

- MNI POLITICAL RISK ANALYSIS: HUNGARY ELECTION PREVIEW

- TSMC’S SALES BEAT ESTIMATES AFTER WAR FAILS TO DENT AI DEMAND

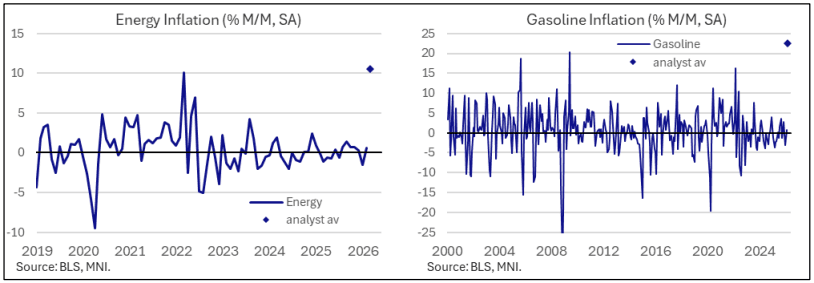

Figure 1: Recent US inflation developments

NEWS

MNI US CPI PREVIEW: A Crude Shift Further From Target

Released Friday at 0830ET, headline CPI is expected to have surged in March with a 0.9-1.0% M/M increase due to a historically large energy price increase on the US-Israel-Iran war. Core CPI is seen increasing a more modest 0.27% M/M in March after 0.22% M/M, with much more limited initial spillover from the energy shock. Within core, expect transportation-related categories to be in focus plus broader indications of supply chain pressures which ticked up to a fresh high since early 2023 according to the NY Fed.

MNI POLITICAL RISK ANALYSIS: Hungary Election Preview

For the first time since the governing Fidesz party took power in 2010, the government faces a serious electoral challenge on 12 April, which could see Prime Minister Viktor Orbán ousted after an unbroken 16-year period in office. In this preview, we provide a background to the election race, an explainer of the electoral system for the National Assembly and identities of the main political parties, a chartpack of the latest opinion polling and predictions market odds, analysis of various post-election scenarios with assigned probabilities, a financial market overview, and views from sell-side analysts.

MNI POLITICAL RISK ANALYSIS: Peru Election Preview

Peru holds its general election on 12 April in a contest that follows five years of political chaos in the aftermath of the 2021 vote. Voters will determine the next president and vice president, as well as all members of Congress (130 seats in the Chamber of Deputies, 60 in the Senate), following a return to a bicameral legislature. In this preview, we provide a background to the election race, an explainer of the electoral system and identities of the main presidential candidates, a chartpack of the latest opinion polling and predictions market odds, analysis of various post-election scenarios with assigned probabilities, a financial market and EM credit overview, and views from sell-side analysts.

RUSSIA/UKRAINE (BBG): Zelenskiy’s Top Aide Sees Ukraine Nearing a Deal With Putin

Ukraine’s top negotiator with Russia said he sees progress toward a potential peace deal with the Kremlin, adding that a resolution to the war may not take long to achieve. While negotiations to end Europe’s bloodiest conflict since World War II have publicly yielded few results, Kyrylo Budanov expressed optimism that the talks are evolving toward a settlement. Ukraine’s former top military spy said he believes Russia also wants to stop the war. “They all understand the war needs to end. That’s why they are negotiating,” Budanov said in an April 4 interview with Bloomberg. “I don’t think it will be long.”

US/IRAN (BBG): Trump Demands Reopening of Hormuz as US-Iran Peace Talks Near

President Donald Trump demanded Iran reopen the Strait of Hormuz, raising pressure on Tehran before talks to turn a fragile ceasefire into lasting peace. The truce remains shaky, with Kuwait reporting large-scale drone attacks on “vital” facilities overnight into Friday and accusing Iran and its proxy groups of violating the ceasefire announced by Washington and Tehran two days earlier. The war has already killed thousands of people and damaged energy infrastructure across the oil-rich Persian Gulf. US and Iranian delegations are set to meet in Pakistan on Saturday, with shipping through Hormuz — which handled about a fifth of the world’s oil and liquefied natural gas before the war — a central sticking point.

US/EU (BBG): EU and US Near Critical Minerals Deal to Combat Chinese Control

The European Union and US are nearing an agreement to coordinate on producing and securing critical minerals, part of a push to break reliance on Chinese supplies. The potential deal would create incentives, such as minimum prices, that could advantage non-Chinese suppliers, according to a draft of an “action plan” seen by Bloomberg. The EU and US would also cooperate on standards, investments and joint projects, as well as coordinate on any supply disruptions by countries like China.

US/UK (Telegraph): Starmer Says He Is ‘Fed Up’ With Trump

Sir Keir Starmer has said he is “fed up” with Donald Trump and appeared to compare him to Vladimir Putin. During a trip to the Gulf, the Prime Minister said he was unhappy with the impact of the Iran war on the domestic cost of living. Sir Keir told ITV’s Robert Peston: “I’m fed up with the fact that families across the country see their bills go up and down on energy, businesses’ bills go up and down on energy because of the actions of Putin or Trump across the world.” He also split with the US president over Israel’s attacks on Lebanon, saying the strikes “shouldn’t be happening.”

UK (MNI): Def Sec Promises Investment Plan, but Sky Reports Situation a “Fiasco”

Speaking at the London Defence Conference, Secretary of State for Defence John Healey says that the gov't is planning to "publish a defence investment plan as soon as we can". However, Sky News reported earlier today that, according to defence sources, the "multimillion-pound push by the defence secretary to transform how the UK rearms and fights is a "fiasco", with too much focus on changing structures instead of preparing for war..." The Defence Investment Plan had been due in Autumn 2025, with a Whitehall source now telling Sky it may come in June. Sky: "The delay is understood to be largely because of the need for more money to be made available faster by the Treasury. If that is not granted, then difficult choices on cutting programmes will have to be taken - even as Sir Keir Starmer says the military is moving to a war footing."

CHINA (MNI EXCLUSIVE): Robust Exports to Support China's 5% Growth - Advisors

China advisors share their GDP outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com: mailto:sales@marketnews.com

BOJ (MNI INTERVIEW): BOJ April Rate Hike Difficult - Ex-Chief Econ

The BOJ's former chief economist shares his policy rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

BOJ (MNI): BOJ to Manage Policy Timely on Stagflation - Mimino

Bank of Japan Deputy Governor Ryozo Himino said on Friday that the BOJ will manage monetary policy appropriately while remaining mindful of the risk of stagflation, with a focus on achieving its 2% price target. Himino told lawmakers the bank will assess policy at each meeting based on the data available at the time. He said Japan is not currently in stagflation, noting that CPI is moving close to the 2% target and GDP is growing above its potential rate.

S.KOREA (MNI): BOK Keeps Policy Rate at 2.50%

The Bank of Korea’s board on Friday decided to keep its base interest rate unchanged at 2.50% for a seventh straight meeting, adopting a wait-and-see approach amid uncertainty over the economic and inflation outlook, Wowkorea reported. However, the bank remains vigilant over currency weakness and its upward pressure on inflation, which is converging toward the 2% target, as well as elevated housing prices. The bank is expected to keep the policy rate at 2.50% for the time being unless the economy shows clear signs of deterioration.

PERU (BBG): Peru Holds Key Rate at 4.25% as Inflation Tops Target Band

Peru left interest rates unchanged as policymakers judge that last month’s surge in inflation will prove to be temporary. The central bank held its benchmark rate at 4.25% for the seventh straight month on Thursday, as expected by all 11 analysts surveyed by Bloomberg. “It is projected that both year-on-year inflation and inflation excluding food and energy will return to the target range toward the end of the year and settle around 2% in 2027, as the effects of supply shocks gradually dissipate,” the bank said in its statement.

CORPORATE (BBG): TSMC’s Sales Beat Estimates After War Fails to Dent AI Demand

Taiwan Semiconductor Manufacturing Co. reported a 35% increase in quarterly revenue, suggesting global AI chip demand remained intact during the first weeks of war in the Middle East. Revenue for the three months through March rose to NT$1.13 trillion ($35.6 billion), the main chipmaker for Nvidia Corp. and Apple Inc. said Friday in a statement. Analysts estimated NT$1.12 trillion on average. Sales in March rose 45%.

DATA

GERMANY DATA (MNI): German HICP Confirms Flash, Transport the Main Upward Driver

- GERMANY MAR FINAL HICP 2.8% Y/Y (2.8% FLASH, 2.0% FEB)

- GERMANY MAR FINAL HICP 1.2% M/M (1.2% FLASH, 0.4% FEB)

German final HICP confirmed the flash estimate, rising 2.8% Y/Y (2.0% prior) and 1.2% M/M (0.4% prior) in March. The rate of inflation is the highest since December 2024, following February's 2.01%, and looks broadly unchanged from the flash estimate. Looking at the details, the data appears little changed from the flash estimate: in terms of ECOICOP 2 divisions, a likely energy-driven 4.4ppt pickup in transport HICP (now 6.6% Y/Y vs 2.2% prior) is the main upward driver of headline inflation.

UK DATA (MNI): BRC Footfall Rises Y/Y on Easter Timing Boost, Likely to Be Short-Lived

UK footfall grew 2.4% Y/Y in March, up from February's notably weak -4.7% (following -0.6% Jan). Although the figure is the strongest (and first positive reading) since last April, it is distorted by the Easter weekend falling partly in March's reporting period this year (vs entirely in April last year), and we note that March 2025 saw footfall drop around -5% Y/Y for a favourable base effect. It's hard to interpret this print without waiting for context from April's data. The press release notes that "Without the final week's Easter bump, March would likely have remained in negative territory".

ITALY DATA (MNI): IP Surprisingly Dips on Reversals in Energy/Consumer Durables

Italy industrial production disappointed as it slipped further in February, with a still tepid trend as strength in transport and computer & electronic equipment is countered by weakness in materials. It leaves all of the big four Eurozone countries with a montlhly drop in IP before the Middle East conflict. Industrial production rose a modest 0.1% M/M (SA) in February, below consensus of a stronger 0.5% M/M rebound from January's -0.6% decline. Sharp reversals lower in energy and consumer durables production were partially offset by a rebound in capital goods, with more modest moves elsewhere.

SWEDEN DATA (MNI): Soft Activity Backdrop Ahead of Iran War Inception

Swedish GDP was unchanged in February, according to latest monthly activity readings. This was below the three-analyst consensus of 0.5%, and leaves 3m/3m growth tracking at a soft -0.9% (vs -0.2% in Jan, 0.5% in Dec). Potential negative growth effects stemming from the Iran war may limit the scope for a rebound in March. While the data is lagged, it provides a snapshot of the economy before the Iran war started. Overall, it supports our view that any tightening from the Riksbank in response to the energy shock should be less aggressive than the likes of the ECB. Indeed, had it not been for the latest shock, data outturns would have strengthened the case for a Riksbank cut.

NORWAY DATA (MNI): March CPI-ATE in Line With Norges Forecast, Keeps Hikes on the Table

- NORWAY MAR CPI-ATE 3.0% Y/Y (3.0% FEB)

- NORWAY MAR CPI-ATE 0.1% M/M (0.7% FEB)

Norwegian CPI-ATE inflation was 3.03% Y/Y in March, unchanged from February. This was a tenth below the Bloomberg median forecast, but in line with Norges Bank's March MPR projection. Given the hawkish signals from the March decision/rate path, the reading keeps hikes firmly on the table - even if Middle East ceasefire hopes are realised. Underlying services inflation remains sticky. The deadline for union wage mediation is Sunday, and the agreement relative to Norges Bank's 4.5% 2026 wage growth forecast could be key in determining whether a May hike is warranted. On a seasonally adjusted basis, CPI-ATE inflation rose 0.20% M/M, the lowest rate in four months. That left 3m/3m momentum unchanged - and still elevated - at 3.74% Y/Y (vs 3.75% prior).

JAPAN DATA (MNI): Japan March CGPI Rises 2.6% Y/Y; Import Price Rises

- JAPAN MARCH CORP GOODS PRICE INDEX +2.6% Y/Y; FEB +2.1%

- JAPAN MARCH CORP GOODS PRICE INDEX +0.8% M/M; FEB +0.1%

Japan's corporate goods price index rose 2.6% y/y in March, accelerating from February’s 2.1%, while import prices rose for a fourth straight month, data released by the Bank of Japan showed on Friday. The March index was boosted by petroleum and coal products (-7.3% vs. -11.7%) and chemical and related products (-0.4% vs. -2.5%). The CGPI rose 0.8% m/m in March, marking a seventh consecutive increase, following a 0.1% rise in February.

CHINA DATA (MNI): China's March PPI Turns Positive After 41-Month Drop

China’s Producer Price Index rose 0.5% y/y in March, reversing February's 0.9% drop and marking the first rise since Sept 2022, driven by a rapid rise in international commodity prices, according to data from the National Bureau of Statistics released Friday. The figure outperformed the median forecast of 0.4%. On a monthly basis, PPI rose 1.0%, up from February's 0.4%, marking the sixth month of positive change and the largest increase in 48 months, mainly driven by the prices of oil and gas extraction, fuel processing, and chemicals, which rose by 15.8%, 5.8%, and 3.6%, respectively, expanding by 10.7, 5.4 and 2.3 percentage points from the previous month.

RATINGS: Moody’s on France & S&P on UK Due After Hours

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Moody’s on France (current rating: Aa3; Outlook Negative)

- S&P on the United Kingdom (current rating: AA; Outlook Stable)

- Morningstar DBRS on Lithuania (current rating: A (high), Stable Trend) & Malta (current rating: A (high), Stable Trend)

- Scope Ratings on Hungary (current rating: BBB; Outlook Stable) & Luxembourg (current rating: AAA; Outlook Stable)

Please use this link to access the indicative 2026 sovereign rating review schedules across the five most prominent rating agencies (Fitch, Moody's, S&P, Morningstar DBRS & Scope Ratings). Note that the schedules are indicative only and ratings can be reviewed on an ad-hoc basis. Rating agencies may also adjust their schedules during the year.

FOREX: Dollar Index Consolidating 1% Losses This Week, US CPI Awaited

- Modest upward pressure on crude futures has tilted the dollar index into positive territory early Friday, but net adjustments for the major pairs remain very contained. Overall, the DXY is consolidating a 1% slide this week, as cautious optimism surrounding the ceasefire in the Middle East takes away some of the safe haven demand for the greenback.

- AUD, NZD and SEK are the worst performers on Friday, eroding around 0.3% of their solid rallies this week, with potential profit taking dynamics at play as we approach the weekend and markets remain nervous over the upcoming negotiations in Pakistan.

- For NZDUSD specifically, the risk on impulse and the hawkish tilt to the RBNZ meeting this week keeps the pair around 2.7% off the week’s lows, and a weekly close back above the 50-day EMA at 0.5844 will be closely eyed.

- The Japanese yen is a touch weaker today amid the higher core yields, helping USDJPY re-establish itself back above 159.00 and EURJPY above 186.00. This week’s EURJPY climb has resulted in a breach of key short-term resistance at 184.77, the Feb 25 high, highlighting a bullish reversal and a recent false break of a bull channel support drawn from the Feb 28 ‘25 low. 186.36 is the next level on the topside (the Feb 9 high), before 186.87, the Jan 23 high and a key medium-term resistance.

- All focus turns to today’s release of US CPI. Other scheduled data points include Canada employment and prelim readings of UMich sentiment and inflation expectations.

EGBS: Bunds Off Lows on Russia-Ukraine News, But Iran Ceasefire Concerns Remain

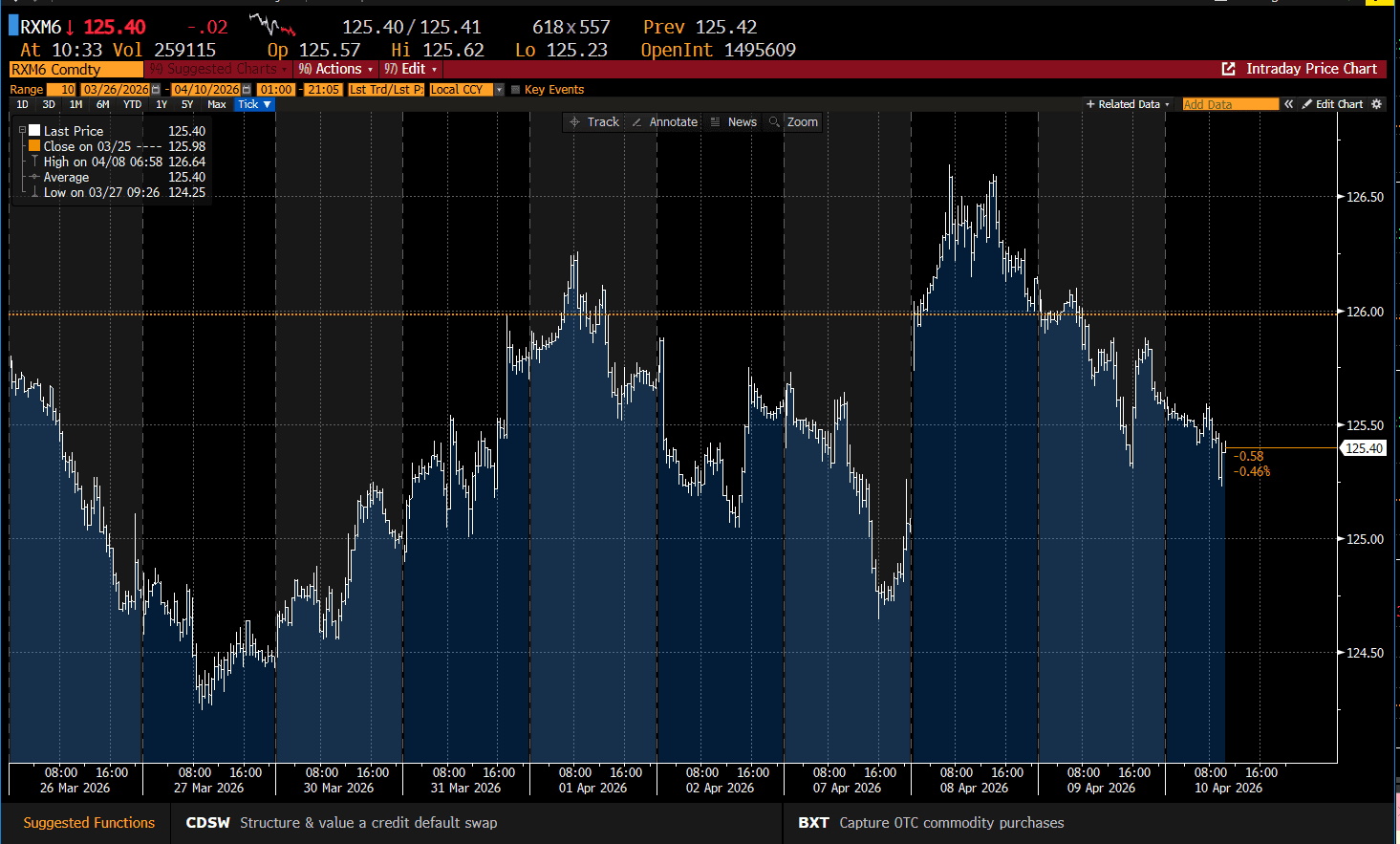

Reports of a potential Russia-Ukraine peace deal generated a small bid in Bund futures, but RXM6 remains a touch below yesterday’s settlement levels. Zooming out, Bunds have continued to retrace Tuesday night’s gap higher, with the fragility of the reported US-Iran ceasefire agreement becoming increasingly apparent. Futures are currently -2 ticks at 125.40, down from a high of 126.64 early Wednesday. Trend signals remain bearish.

- Reports from the Middle East suggest the Iranian negotiating team has not yet arrived in Pakistan for talks, amid continued disagreements around whether Lebanon is included in the ceasefire agreement.

- Meanwhile, the Russia-Ukraine news comes with caveats, with the source declining to “say how a possible compromise would look like on territory, the thorniest issue at the talks”.

- The German curve has seen a fairly parallel 3.5-4.0bp shift higher today. 2s10s and 10s30s are off late-March lows, but still remain much flatter than pre-Iran war levels.

- This morning’s Italian supply was well digested, but the 10-year BTP/Bund spread remains 3.5bps wider on the session at 78.5bps.

- In data, Italian February industrial production was weaker than expected, meaning all four major Eurozone economies saw soft prints before the Iran war started.

Figure 2: Bund futures since March 26

Source: Bloomberg Finance L.P.

GILTS: Holding Lower, Futures Within Yesterday's Range

Gilts trade lower this morning alongside moves in wider core global FI markets, with ongoing questions surrounding the longevity/viability of the U.S.-Israel-Iran ceasefire countering some of yesterday’s late rally.

- Gilt futures flat at 88.83, with yesterday’s low in the contract untouched.

- Bears pierced the 20-day EMA yesterday and will look to close Wednesday’s opening gap higher (88.03) next. Conversely, bulls will look to clear Thursday’s high (90.21) to strengthen the short-term bullish technical theme.

- Yields 5-6bp higher across the curve.

- Bulls need to force clean breaks below the March 18 yield lows across the curve to signal the potential for a more meaningful bullish move.

- 2s10s and 5s30s haven’t retested March highs.

- BoE-dated OIS pricing 5bp of tightening for this month, 17bp through June, 27bp through July and 38.5bp through year-end. Dec pricing has traded in a 30-42bp range since Wednesdays open.

- SONIA futures little changed to +1.5, off yesterday’s recovery highs alongside gilts.

- Expect positioning for the weekend talks between Iran and the U.S. to dominate today, with U.S. CPI data providing the major datapoint of note ahead of the weekend.

- Little of note on the domestic calendar.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Apr-26 | 3.777 | +4.8 |

Jun-26 | 3.898 | +16.9 |

Jul-26 | 3.998 | +26.9 |

Sep-26 | 4.078 | +35.0 |

Nov-26 | 4.104 | +37.5 |

Dec-26 | 4.114 | +38.5 |

Feb-27 | 4.119 | +39.0 |

Mar-27 | 4.123 | +39.4 |

Apr-27 | 4.120 | +39.2 |

EQUITIES: EuroStoxx Futures Holding Onto Gains, Bull Trigger at 6143.00

EuroStoxx 50 futures are holding on to their recent gains. The contract has traded through both the 20- and 50-day EMAs, paving the way for a climb towards 5945.47, a Fibonacci retracement point. Note that a break of 5945.47 would expose the key resistance and bull trigger at 6143.00, the Feb 26 high. First key support to watch lies at 5525.00, the Apr 2 low. A move lower and a breach of this support would highlight a reversal. A strong rally in S&P E-Minis this week highlights an extension of the reversal that started Mar 31. Note that trend signals remain bearish and for now, this suggests that gains are corrective. A continuation higher would open 6921.09 next, a Fibonacci retracement point. Key medium-term resistance and the bull trigger is far off at 7096.50, the Jan 28 high. Initial firm support to watch lies at 6567.00, the Apr 6 low.

- Japan's NIKKEI closed higher by 1028.79 pts or +1.84% at 56924.11 and the TOPIX ended 1.62 pts lower or -0.04% at 3739.85.

- Elsewhere, in China the SHANGHAI closed higher by 20.054 pts or +0.51% at 3986.225 and the HANG SENG ended 141.14 pts higher or +0.55% at 25893.54.

- Across Europe, Germany's DAX trades higher by 38.41 pts or +0.16% at 23846.16, FTSE 100 higher by 23.21 pts or +0.22% at 10626.87, CAC 40 up 16.92 pts or +0.21% at 8262.06 and Euro Stoxx 50 up 14.84 pts or +0.25% at 5910.73.

- Dow Jones mini down 101 pts or -0.21% at 48319, S&P 500 mini down 9.5 pts or -0.14% at 6854.25, NASDAQ mini down 36 pts or -0.14% at 25217.

Time: 10:00 BST/05:00 ET

COMMODITIES: This Week's Sharp WTI Pullback Still Considered Corrective

A sharp pullback in WTI futures this week is for now, considered corrective. The contract has traded through the 20-day EMA and this exposes a key support around the 50-day EMA, at $85.87. A clear break of the 50-day average is required to highlight a stronger short-term reversal. On the upside key resistance and the bull trigger has been defined at $117.63, the Apr 7 high. Clearance of this hurdle would confirm a resumption of the uptrend. Recent gains in Gold appear to be corrective, however for now, the short-term bull cycle remains intact. The metal has pierced the 50-day EMA, at $4782.5. This signals scope for an extension towards $4914.9, a Fibonacci retracement point. Clearance of this level would open the $5000.0 handle. Initial firm support to watch lies at $4554.2, the Apr 2 low. Clearance of this level would be bearish.

- WTI Crude up $2.09 or +2.14% at $99.94

- Natural Gas up $0.01 or +0.19% at $2.675

- Gold spot down $26.27 or -0.55% at $4741.08

- Copper up $0.75 or +0.13% at $577.2

- Silver down $0.4 or -0.54% at $74.9095

- Platinum down $55.76 or -2.65% at $2045.09

Time: 10:00 BST/05:00 ET

| Date | GMT/Local | Impact | Country | Event |

| 10/04/2026 | 1000/1200 | ECB de Guindos Remarks at Development Event | ||

| 10/04/2026 | 1200/0800 | ** | Brazil Final CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | Labour Force Survey | |

| 10/04/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 10/04/2026 | 1400/1000 | ** | Factory New Orders | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1800/1400 | ** | Treasury Budget | |

| 10/04/2026 | - | *** | New Loans | |

| 10/04/2026 | - | *** | Money Supply | |

| 10/04/2026 | - | *** | Social Financing |