MNI US OPEN - US CPI an Important Pre-FOMC Steer

EXECUTIVE SUMMARY

- MNI US CPI PREVIEW – AN IMPORTANT PRE-FOMC STEER

- MNI POLITICAL RISK ANALYSIS – UK SPENDING REVIEW PREVIEW

- US, CHINA OFFICIALS AGREE ON PLAN THAT AWAITS XI, TRUMP SIGN-OFF

- TRUMP TARIFFS CAN STAY IN EFFECT LONGER, APPEALS COURT SAYS

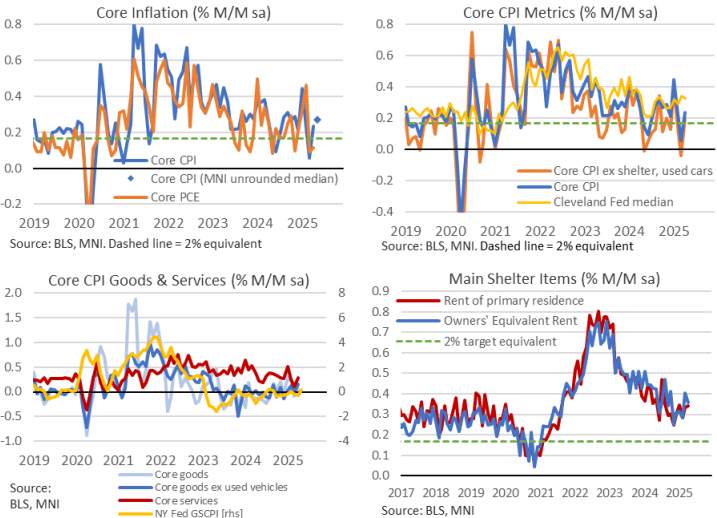

Figure 1: Recent US inflation developments

NEWS

MNI US CPI PREVIEW: An Important Pre-FOMC Steer

Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April. We’ve seen an unrounded range of 0.23-0.34% M/M, with some sizeable discrepancies in used cars and lodging away from home as well as a CPI-specific airfares. The broad assumption is that May could have started to see a greater tariff impact than April but that firmer increases are more likely to show in summer months. Both headline and core CPI Y/Y inflation should firm one to two tenths after lows since early 2021, whilst the six-month core rate should see a similar print after four months running hotter than the Y/Y.

US/CHINA (MNI): China VP - Two Sides Should Safeguard 'Hard Won Outcome' From Talks

MNI (London) Reuters reporting comments from Chinese Vice Premier He Lifeng, who led China's delegation in the talks with the US that took place in London over 9-10 June. VP says: "China's stance on trade issues with the US is clear and consistent." Says that the "Two sides should enhance consensus, strengthen cooperation, and jointly safeguard the hard-won outcome from the dialogues." He Lifeng: China and US "should maintain communication" and "push for table and long-term China-US trade and economic ties." The VP says "China is sincere in trade and economic consultations, but has its principles."

US/CHINA (BBG): US, China Officials Agree on Plan That Awaits Xi, Trump Sign-Off

The US and China capped two days of high-stakes trade talks with a plan to revive the flow of sensitive goods — a framework now awaiting the blessing of Donald Trump and Xi Jinping. After some 20 hours of negotiations in London, US Commerce Secretary Howard Lutnick said both sides had established a framework for implementing the Geneva consensus that last month brought down tariffs. “First we had to get sort of the negativity out,” he said. “Now we can go forward to try to do positive trade, growing trade.”

US (BBG): Trump Tariffs Can Stay in Effect Longer, Appeals Court Says

Donald Trump can continue to enforce his global tariffs for now, a federal appeals court held in a win for the president on one of his signature economic policies. The order Tuesday by the US Court of Appeals for the Federal Circuit extends an earlier, short-term reprieve for the administration as it presses a challenge to a lower court ruling last month that blocked the tariffs. The Justice Department had argued that US officials’ concerns about ongoing trade negotiations outweighed the economic harm claimed by the small businesses that sued.

US/EU (BBG): EU Aims for US Trade Talks to Extend Past Trump’s July Deadline

The European Union believes trade negotiations with the US could extend beyond President Donald Trump’s July 9 deadline, even as the speed of the talks has increased over the past week. The EU sees reaching an agreement on the principles of a deal by July 9 as a best-case scenario, which would allow further talks to work out the details, according to people familiar with the matter. The US is expected to respond to the latest round of negotiations in the coming days and provide clarity on the next steps.

US/IRAN (BBG): Iran Says Nuclear Deal ‘Within Reach,’ Can Be ‘Achieved Rapidly’

Iranian foreign minister says a nuclear agreement which “can ensure the continued peaceful nature of Iran’s nuclear program is within reach—and could be achieved rapidly,” Abbas Araghchi posts on X ahead of nuclear talks with the US Sunday. Says potential nuclear deal relies on Iran’s continued uranium enrichment, sanctions removal. Iran’s nuclear activities would be “under the full supervision of the IAEA.”

US (BBG): US Judge to Weigh Limiting Military Troops in LA on Thursday

California’s bid to limit military involvement in the Los Angeles immigration protests will be taken up by a judge Thursday, meaning that a pullback by the Trump administration before then is unlikely. The state is seeking a court order temporarily restraining the deployment of thousands of troops from the National Guard and the US Marines amid protests over President Donald Trump’s immigration raids. In their request for an emergency order by Tuesday afternoon, attorneys for the state argued that the military deployment “creates imminent harm to state sovereignty” and “escalates tensions.”

US (MNI): Musk Seeks to Repair Relations w/Trump Admin

Former special government employee Elon Musk posts on his X platform: "I regret some of my posts about President [Donald Trump] last week. They went too far." The spectacular explosion in the relationship between Trump and Musk, who set up the 'Department for Government Efficiency' (DOGE) and donated hundreds of millions of dollars to Trump's re-election campaign, became a major political talking point last week. After Musk criticised Trump's 'One Big Beautiful Bill', the two men traded barbs with Trump criticising Musk during an Oval Office meeting with German Chancellor Friedrich Merz and calling Musk 'crazy' on his Truth Social platform.

MNI POLITICAL RISK ANALYSIS: UK Spending Review June 2025

Chancellor of the Exchequer Rachel Reeves will engage in one of the major parliamentary set-pieces for HM Treasury at 12:30BST (07:30ET, 13:30CET) on Wednesday 11 June when she unveils the government’s latest Spending Review. In this article, we examine the political context and considerations around the Spending Review, with the incumbent Labour government facing the seemingly intractable demands of boosting growth and productivity, lowering the tax burden on workers, funding improvements in public services, and sticking to the chancellor’s fiscal rules.

UK (MNI): Cabinet Giving Final Sign-Off Before Spending Review at ~12:30BST

Prime Minister Sir Keir Starmer is holding a cabinet meeting to give final sign-off to Chancellor of the Exchequer Rachel Reeves' Spending Review. Ministers leading all gov't departments have now given their approval to their settlements, with Home Secretary Yvette Cooper seen to be the last holdout, likely indicating a sub-par settlement for the department in charge of policing, borders, and immigration (among other areas) in Cooper's view. The Mirror highlights the main announcements already known: 15.6 billion for public transport projects in England's city regions; 16.7 billion for nuclear power projects, including 14.2 billion for the new Sizewell C power plant in Suffolk; 39 billion over the next 10 years to build affordable and social housing; An extension of the 3 bus fare cap until March 2027; 445 million for upgrades to Welsh railways.

ECB (MNI): Further Currency Shifts May Strengthen Euro's Global Role

The ECB has published its annual report into the euro. President Lagarde's foreword notes that: "The euro continued to hold its position as the second most important currency globally" in 2024. "Further shifts may be underway in the landscape of international currencies. The tariffs imposed by the US Administration have led to highly unusual cross-asset correlations. This could strengthen the global role of the euro and underscores the importance for European policymakers of creating the necessary conditions for this to occur."

ECB (BBG): ECB’s Kazaks Says Some Fine-Tuning Rate Cuts ‘Quite Likely’

European Central Bank Governing Council member Martins Kazaks said further interest-rate cuts may be needed, according to Econostream Media. “We’ve done a lot in terms of rate cuts, and monetary policy will need to remain vigilant to ensure that inflation stays around 2%,” he was cited as saying in an interview conducted June 6. “Will it require some further cuts for fine tuning? Quite likely.”

FRANCE (MNI INTERVIEW): France Ready to Join SAFE Loan Facility

French Treasury Chief Economist Dorothee Rouzet talks about funding increased defence spending. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): Japan’s MOF Says Speculation of July JGB Buyback Unrealistic

Buying back of super-long government bonds from July is unrealistic and not envisioned, an official from Japan’s Ministry of Finance said in an email to Bloomberg News. It is not true that the MOF has established a policy to implement the buyback of super-long government bonds.

CHINA (BBG): PBOC Gauges Demand for Six-Month Outright Reverse Repos: Traders

China’s central bank has contacted some lenders to gauge demand for six-month outright reverse repos on Wednesday, according to traders at primary dealers. It wasn’t clear whether the gauging would eventually lead to actual liquidity operations by the People’s Bank of China, said the traders. The traders asked not to be named discussing private matters.

CHINA (MNI): China Trade VP Urges Free Trade Implementation

MNI (Beijing) Chinese authorities hope local governments, overseas business organisations and enterprises will do a good job implementing free trade agreements and promote the high-quality development of foreign trade, Li Chenggang, international trade negotiation representative and vice minister of the Ministry of Commerce said on Wednesday.

ISRAEL (MNI): Opposition Parties to Table Motion to Dissolve Knesset

The Times of Israel reports that opposition parties confirmed their intention to pull all draft legislation from parliamentary agenda and propose to dissolve the Knesset, noting that their decision was 'made unanimously and is binding on all factions.' Opposition leaders said this in a joint statement issued after a meeting today, pledging to 'concentrate all efforts on one goal: to overthrow the government.' The piece notes that 'the coalition is widely expected to seek to pack the agenda with its own bills in order to delay a preliminary vote on the measure.'

HONG KONG (MNI): HK Pensions Fund to Cut Tsy Holdings if US Lose Last AAA Rating

Hong Kong's pension plan are planning to cut Treasury holdings if the US loses its AAA rating, according to Bloomberg sources. Highlights from the piece: "Hong Kong’s pension fund managers have formed a preliminary plan to sell down their Treasury holdings within as soon as three months if the US loses its last recognized top credit rating", "Industry groups including the Hong Kong Investment Funds Association and the Hong Kong Trustees’ Association discussed the proposal with the pensions regulator on Wednesday."

S.KOREA (BBG): Korean President Visits Stock Exchange in Bid to Boost Market

South Korea’s newly elected President Lee Jae-myung made a high-profile visit to the main stock exchange, signaling a commitment to follow through on his pledges to boost the market. In discussions with traders Wednesday, Lee emphasized ways to curb abusive practices in the market, including share manipulation, as well as plans to change taxes to spur more dividends and other updates to support investors, according to a statement from his office.

DATA

ECB DATA (MNI): Small Upward Revision to Latest ECB Wage Tracker; Broader Trend Intact

There were slight upward revisions to the ECB's forward looking wage tracker compared to the April vintage, but the broader theme of softening compensation pressures remains intact. The tracker excluding one-off payments is seen at 3.082% in Q4 2024 (vs

3.024% in the April iteration). The ECB projects compensation per employee growth at 2.8% by the last quarter of this year, down from 3.8% in Q1. There were also upward revisions to the share of employees covered by the wage tracker (45% in Q4 2025 vs 43% in April).

JAPAN DATA (MNI): Japan May CGPI Rises 3.2% Y/Y; Import Price Drops

- JAPAN MAY CORP GOODS PRICE INDEX +3.2% Y/Y; APRIL +4.1%

- JAPAN MAY CORP GOODS PRICE INDEX -0.2% M/M; APRIL +0.3%

Japan’s corporate goods prices slowed in May but remained higher than Bank of Japan projections, supported by persistent cost pressures in labour, logistics and key commodities, data released by the BOJ on Wednesday showed. The Corporate Goods Price Index rose 3.2% y/y in May, decelerating from April’s revised 4.1%, as gains were tempered by weaker petroleum and coal product prices (+0.6% vs. +6.3%) and falling nonferrous metal prices (-2.1% vs. +4.2%). On a monthly basis, the CGPI fell 0.2%, marking the first drop since August 2024, after a 0.3% rise in April.

FOREX: Vols See Minimal Pre-CPI Premium, DXY Clear of Test of Downtrendline

- The USD Index is firmer, but well off session highs - keeping markets clear of any material test on the downtrendline resistance drawn off the early February high (today crossing at 99.462, just below the 100.004 50-dma). This level remains a key focus headed through the several inflation releases this week (CPI today, PPI tomorrow).

- Meanwhile, the front-end of the G10 FX vol curve remains subdued headed into today's CPI print, with vols sold on the back of confirmation that US and Chinese officials had agreed on an approach for trade negotiations - that now awaits sign-off from the Chinese, US Presidents. Statements from both sides show little substantive progress on the key issues, leaving an element of uncertainty on the table ahead.

- EUR/USD is well off lows, but spot remains inside the weekly range - the ECB's wage tracker saw a minor upward revision - leaving little ripple in ECB rates markets that price one further 25bps rate cut before year-end.

- With overnight USD/JPY vols briefly above 15 points today, either side of the post-Liberation Day average, which suggests the underlying spot downtrend remains intact for now, despite the bounce off last week's lows. As such, 142.12 / 145.29 remain the key parameters.

EGBS: Weaker Amid Light Regional Calendar; 10s30s Breaks Recent Range

Bund futures are off session lows but have weakened steadily through the session (-17 ticks at 130.66), but activity is fairly limited ahead of the UK spending review at 1230BST and the US CPI report at 1330BST. Supply-driven pressure alongside a recovery in European equity futures have seemingly driven this morning’s price action.

- The latest pullback in Bund futures still appears corrective - for now - and the trend condition remains bullish.

- The German curve sits steeper, with 2s10s and 10s30s each up 1.4ps. While 2s10s remains within this week’s 67-71bps range, 10s30s now trades at its steepest since last Thursday’s ECB decision at 46bps.

- Germany sold E3bln of the 10-year 2.50% Feb-35 Bund. Results were stronger than the last outing in May, albeit for a smaller auction size. Portugal also sold OTs this morning.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels.

- The ECB’s forward looking wage tracker update wasn’t a market mover. There were slight upward revisions compared to the April vintage, but the broader theme of softening compensation pressures remains intact.

- ECB’s Kazaks echoed prior remarks, saying some “fine-tuning” of rate cuts is likely. Markets continue to price one more full 25bp cut through year-end.

GILTS: Weaker & Steeper Ahead of Spending Review

Gilt futures have broken yesterday’s base, trading as low as 92.20.

- Bears look to close yesterday’s opening gap higher (92.00) after bulls forced their way through a cluster of resistance levels on Tuesday.

- The early weakness came as core global FI moved lower, which seemed to be based on a mix of global supply pressure (including a 10-Year gilt auction) and some optimism re: Sino-U.S. trade talks.

- 10-Year supply saw average demand metrics.

- Markets were unmoved by a Chinese statement that failed to reveal any meaningful trade commitments with the U.S.

- Yields 3-6bp higher, bear steepening after yesterday’s labour market data-driven bull steepening.

- 10-Year yields remain above long-term uptrend support drawn off the Dec ’21 lows (4.522% today).

- 30-Year yields closed below long-term uptrend support drawn off their own Dec ’21 lows yesterday (a redrawn support line to account for yesterday’s move comes in at 5.242% today).

- 2s10s nears 65bp, after failing to extend meaningfully below 60bp during breaks in recent sessions.

- 5s30s ~5bp off last week’s multi-week closing low, last ~123bp.

- SONIA futures flat to -3.0. BoE-dated OIS showing 47bp of cuts through year-end vs. closer to 50bp at yesterday’s close.

- Chancellor Reeves will present the spending review from ~12:30 London.

- The release will likely reaffirm the UK’s fiscal fragility (perhaps factoring into this morning’s weakness) and is laden with political risk.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.206 | -0.7 |

Aug-25 | 4.022 | -19.1 |

Sep-25 | 3.965 | -24.7 |

Nov-25 | 3.815 | -39.8 |

Dec-25 | 3.743 | -47.0 |

Feb-26 | 3.640 | -57.2 |

Mar-26 | 3.616 | -59.7 |

EQUITIES: E-Mini S&P Trading at Fresh Cycle High, Focus on $6057.00 Next

Eurostoxx 50 futures continue to trade at their recent highs. The trend condition is bullish - moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen the bull theme. Key support to watch lies at 5205.88, the 50-day EMA. A clear break of this average would signal a possible reversal. The trend condition in S&P E-Minis remains bullish and the contract has again traded to a fresh cycle high, today. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. Sights are on 6057.00 next, the Mar 3 high. Key support to watch lies at 5808.04, the 50-day EMA.

- Japan's NIKKEI closed higher by 209.68 pts or +0.55% at 38421.19 and the TOPIX ended 2.48 pts higher or +0.09% at 2788.72.

- Elsewhere, in China the SHANGHAI closed higher by 17.5 pts or +0.52% at 3402.316 and the HANG SENG ended 204.07 pts higher or +0.84% at 24366.94.

- Across Europe, Germany's DAX trades higher by 69.8 pts or +0.29% at 24056.77, FTSE 100 higher by 22.6 pts or +0.26% at 8875.77, CAC 40 up 33.89 pts or +0.43% at 7838.18 and Euro Stoxx 50 up 12.65 pts or +0.23% at 5427.91.

- Dow Jones mini down 38 pts or -0.09% at 42872, S&P 500 mini down 4.75 pts or -0.08% at 6040, NASDAQ mini down 8.75 pts or -0.04% at 21954.5.

Time: 09:50 BST

COMMODITIES: WTI Futures Extending Current Bull Cycle

WTI futures have traded higher this week, extending the current bull cycle. The contract has cleared the 50-day EMA, signalling scope for an extension towards $67.14 next, a Fibonacci retracement. It is still possible that the recovery since early May is a correction. MA studies are in a bear-mode position, highlighting a dominant M/T downtrend. Support to watch lies at $59.74, the May 30 low. A break would highlight a potential bearish reversal. A bullish theme in Gold remains intact and the latest pullback appears corrective. Medium-term trend signals remain bullish - moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would refocus attention on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, the next support to monitor is $3245.6, the 50-day EMA.

- WTI Crude up $0.17 or +0.26% at $65.19

- Natural Gas up $0.03 or +0.74% at $3.558

- Gold spot up $21.61 or +0.65% at $3346.06

- Copper down $4.25 or -0.87% at $485.7

- Silver down $0.02 or -0.06% at $36.5246

- Platinum up $42.47 or +3.48% at $1262.98

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | - | *** | Money Supply | |

| 11/06/2025 | - | *** | New Loans | |

| 11/06/2025 | - | *** | Social Financing | |

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI | |

| 11/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/06/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/06/2025 | 1800/1400 | ** | Treasury Budget | |

| 12/06/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 12/06/2025 | 0600/0700 | ** | Trade Balance | |

| 12/06/2025 | 0600/0700 | ** | Index of Services | |

| 12/06/2025 | 0600/0700 | *** | Index of Production | |

| 12/06/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/06/2025 | 0900/1100 | ECB Schnabel Visits "House of the Euro" | ||

| 12/06/2025 | 1200/1400 | ECB de Guindos At Financial Integration Conference | ||

| 12/06/2025 | 1220/1420 | ECB Schnabel At Financial Integration Conference | ||

| 12/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 12/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 12/06/2025 | 1230/0830 | * | Household debt-to-income | |

| 12/06/2025 | 1230/0830 | *** | PPI | |

| 12/06/2025 | 1400/1000 | * | Services Revenues | |

| 12/06/2025 | 1415/1615 | ECB Elderson At Senior Supervisors Conference | ||

| 12/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 12/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/06/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/06/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond |