MNI US OPEN - Ukraine Peace Negotiations Continue Today

EXECUTIVE SUMMARY

- ZELENSKY OFFERS COMPROMISE FOR NEW ROUND OF UKRAINE PEACE TALKS

- FRENCH SENATE TO VOTE ON 2026 PLF TODAY, BUT NATIONAL ASSEMBLY SUPPORT UNLIKELY

- BOJ SURVEY SHOWS SOLID WAGE GROWTH FOR FY26

- CHILE RIGHT-WING CANDIDATE KAST COMFORTABLY WINS PRESIDENTIAL ELECTION

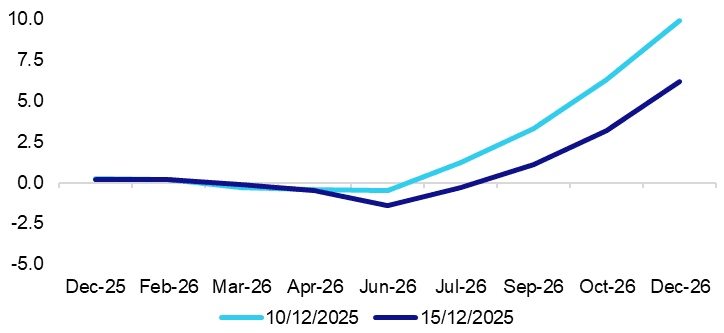

Figure 1: ECB-dated OIS shows only 6bps of hikes priced through December 2026

Source: MNI, Bloomberg Finance L.P.

NEWS

US/RUSSIA/UKRAINE (NYT): Zelensky Offers Compromise for New Round of Ukraine Peace Talks

President Volodymyr Zelensky of Ukraine met in Germany on Sunday with President Trump’s negotiators in what was viewed as a critical round of talks to try to agree on a plan to end the war with Russia. As Mr. Trump pushes Mr. Zelensky to take a deal, saying Ukraine is losing, Mr. Zelensky made it clear that the country was willing to compromise on certain issues. He reiterated before the meeting that Ukraine would give up on its hopes to join NATO, at least for now, as long as it won strong security guarantees from the United States to prevent Russia from again invading if a peace deal was reached. But Mr. Zelensky also repeated that Ukraine did not want to cede territory that it now controls, as the Trump administration has suggested.

US (WSJ): JPMorgan Steps Further Into Crypto With Tokenized Money Fund

JPMorgan Chase is joining the list of traditional financial firms seeking to bring blockchain technology to an investing staple: the money-market fund. The banking giant’s $4 trillion asset-management arm is rolling out its first tokenized money-market fund on the Ethereum blockchain. JPMorgan will seed the fund with $100 million of its own capital, and then open it to outside investors on Tuesday.

US (WSJ): SpaceX Starts a Wall Street Bake-Off to Hire Banks for Possible IPO

SpaceX executives are starting the process to select Wall Street bankers to advise it on its initial public offering, according to people familiar with the matter. Investment banks are scheduled to make their initial pitches this coming week in what is known as a bake-off, according to people familiar with the matter, representing the most concrete steps the rocket maker has taken toward what would be a blockbuster IPO.

FRANCE (MNI): Senate to Vote on 2026 PLF Today, But National Assembly Support Unlikely

French politics remains a focus, with the year-end deadline for passing a 2026 budget nearing. The 2026 State budget (PLF) is being voted on by the Senate today. Assuming the Senate's amended version of the PLF is passed, a Joint Committee (formed of seven parliamentarians and seven senators) will be convened on Friday to try and reach an upper/lower house compromise. This seems unlikely - on November 21, the National Assembly voted 404 to 1 (with 84 abstentions) against adoption of the first draft of the PLF.

SWITZERLAND (BBG): Switzerland Boosts Growth Outlook for Next Year After Trade Deal

Switzerland lifted the growth outlook for next year on the back of its trade deal with the US, while lowering expectations on inflation after the central bank refrained from further easing. The State Secretariat for Economic Affairs sees gross domestic product adjusted for large sports events expanding 1.1% in 2026, up from its September projection of 0.9%. That almost matches the growth seen before outsized American tariffs took effect. In its first estimate for the year after, the agency known as SECO penciled in 1.7%.

CHINA (MNI): CPI Showed Positive Upward Signs - NBS

MNI (Beijing) China will continue to implement consumer stimulus to expand domestic demand, control capacity in key industries, and regulate market competition order to promote price rises, Fu Linghui, spokesman of National Bureau of Statistics, told reporters on Monday. Prices have shown positive changes over the past two months as the CPI rose by 0.7% year-on-year in November, marking the highest increase since the beginning of the year, while the Producer Price Index recorded growth on a monthly basis for two consecutive months, continuing the overall trend of narrowing year-on-year declines observed since August, he noted.

CHINA (MNI): Measures Taken for Consumption and Investment - NBS

MNI (Beijing) China will further improve the investment environment, leverage the guiding role of government investment and stimulate private investment, while focusing on stabilising employment and promoting income growth to enhance consumption capacity and boost consumer confidence, Fu Linghui, spokesperson for the National Bureau of Statistics, said on Monday.

JAPAN (MNI): BOJ Survey Shows Solid Wage Growth for FY26

Japanese wage growth in fiscal 2026 is expected to remain solid, supported by high corporate profits and persistent labour shortages, according to a Bank of Japan survey released Monday. “It seems that the number of firms expecting a clear improvement in their profits is not large, partly owing to the impact of U.S. tariff hikes; however, most firms appear to consider it necessary to raise wages in fiscal 2026 by as much as in fiscal 2025, or to a similar extent to prevailing wage levels at other firms, in order to retain staff and improve motivation amid ongoing, severe labour shortages,” the BOJ said.

BOJ (BBG): BOJ Is Said to Start Selling ETF Holdings as Soon as January

Bank of Japan officials are likely to start selling the central bank’s pile of exchange-traded funds as early as next month, according to people familiar with the matter, a process expected to take decades to complete. The bank will offload the assets little by little to avoid roiling markets as was decided at a September policy board meeting, the people said. The holdings had a market value of ¥83 trillion ($534 billion) at the end of September and a book value of ¥37.1 trillion, according to the central bank.

RBNZ (MNI): Financial Conditions Have Tightened More Than Expected - RBNZ Governor

The RBNZ has released some remarks from new Governor Breman, as she is making several media appearances this week. The Governor states that the economy has evolved broadly in line with the conditions laid out in the Nov policy review: "We continue to see signs that growth is recovering after having stalled in the middle of this year. The labour market is still weak but is expected to recover as demand in the economy strengthens. We remain confident that annual headline consumers price index inflation will decline towards the 2 per cent target mid-point by the middle of next year."

S.KOREA (BBG): Korean Pension Fund to Take Flexible Approach to FX Hedging

South Korea’s National Pension Service said it will conduct its strategic foreign-exchange hedging in a “flexible” manner in accordance with market conditions while extending the duration to the end of 2026. “The Committee also decided to establish flexible implementation measures to allow strategic hedging to be carried out adaptively in response to market conditions,” it said in a statement on Monday.

CHILE (MNI): Markets Should React Positively to Kast’s Expected Presidential Election Win

As was widely expected, right-wing candidate Jose Antonio Kast comfortably won yesterday’s second-round presidential election run-off, securing 58% of the vote against 42% for left-wing candidate Jeanette Jara. His victory should provide further medium-term support to the peso, which closed at a 14-month high against the dollar last week, buoyed by optimism for a pro-market pivot to the right, as well as support from higher copper prices. Kast campaigned on market friendly policies, including tax and public spending cuts, and promises to clamp down on crime and illegal immigration. In a victory speech yesterday, he promised an emergency government when he takes office in March to improve security. He said he plans to form a unity government, including in Congress.

THAILAND (BBG): Thailand to Curb Baht’s Strength as Currency Hits Four-Year High

Thai authorities are ramping up efforts to curb the baht’s strength after the currency climbed to a four-year high amid record gold prices and peak tourist season. The government plans to ask state-owned firms to accelerate imports and repay foreign debts, Finance Minister Ekniti Nitithanprapas said Monday, adding he is discussing the currency’s rally with Bank of Thailand Governor. The central bank is also tightening oversight on gold traders’ currency transactions.

DATA

EUROZONE OCT IP +0.8% M/M, +2.0% Y/Y (VS +0.2% M/M, +1.2% Y/Y SEP) (MNI)

CHINA DATA (MNI): China's Nov Investment, Sales Slow

- CHINA JAN-NOV FIXED-ASSET INVESTMENT -2.6% Y/Y VS MEDIAN -2.3%

MNI (Beijing) China’s fixed-asset investment growth fell further by 2.6% y/y in the first 11 months, expanding from the 1.7% fall in the Jan-Oct period and missing the -2.3% median forecast, also hitting the lowest level since Jun 2020, National Bureau of Statistics data showed Monday. Property investment fell further by 15.9% in the first 11 months, after a 14.7% decline in Jan-Oct, marking the second sharpest drop in record following a 16.3% fall in the first two months of 2020.

CHINA DATA (MNI): November Retail Sales in Surprise Drop

- CHINA NOV RETAIL SALES +1.3% Y/Y VS MEDIAN +2.9% Y/Y

China's November retail sales had the smallest expansion since 2022. Rising just 1.3% it was a marked downturn from 2.9% in October. The YTD YoY figure was marginally lower than October at 4.0% but consistent with recent trends. The rapid decline in consumer goods, clothing, household electronics, food and services are worrying signs for the outlook for domestic demand and for some domestic commentators, point to the need for further policy response. Recent comments from the government suggest that any policy response may not be imminent and that given China is on track to hit its 5% GDP target, may not be forthcoming.

CHINA DATA (MNI): Property Investment and Sales Fall Further, No End in Sight

- CHINA YTD PROPERTY INVESTMENT -15.9% Y/Y VS MEDIAN -15.4% Y/Y

Following on from the release of further price decrease in new and used homes, November property Investment and Property Sales fell to lows of the year. Property Investment YTD YoY fell -15.9%, the lowest in more than 3-Years. New home sales value fell -11.2% YoY, new property construction fell -20.5% YoY. The fall in Residential Property sales accelerated in November to -11.2%, from -9.4% YoY, the largest drop in 2025. The combined result is the worst in 5-years.

CHINA NOV INDUSTRIAL OUTPUT +4.8% Y/Y VS MEDIAN +5.0% Y/Y: NBS (MNI)

CHINA NOV UNEMPLOYMENT RATE +5.1% VS OCT +5.1%: NBS (MNI)

JAPAN DATA (MNI): Business Inflation Expectations Solid - BOJ Tankan

Inflation expectations of one, three and five years ahead at Japanese firms that Bank of Japan officials closely monitor were largely unchanged from September and remained solid, supporting the bank’s inflation outlook, the BOJ’s December Tankan survey released Monday showed. Bank officials were encouraged by the stability of inflation expectations and sales prices, having been concerned that firms’ favourable inflation views could be undermined by trade policy uncertainty and weak global demand.

NEW ZEALAND DATA (MNI): Services PMI Weakens Further, Remains Entrenched Sub 50.0

The New Zealand services PMI lost momentum for Nov, printing at 46.9, versus 48.4 in Oct. The index has remained sub 50.0 since the early parts of 2024, although we are above 2025 lows (44.2 seen in May). This comes after Friday's manufacturing PMI remained above 50.0, while card spending for Nov showed a firmer trend. Overall, the data reinforces the patchy nature of the current economic recovery in NZ, which is yet to establish a firm footing.

FOREX: Negative Dollar Bias Dominates, USDJPY Returns to 155.00

- Approaching the busy central bank slate and US data calendar this week, the dollar is starting the week on the back foot once again. Moves for the dollar index have been relatively contained, with the DXY just 0.1% lower on the session, although we remain within 20 pips of last week’s pullback lows. The softer dollar backdrop has allowed the likes of gold and silver to extend higher, rising 1% and 3% respectively, while the Japanese Yen outperforms across the G10.

- USDJPY has been pressured by lower core yields on Monday and the monthly Tankan survey / wage report reinforcing the expectations for a BOJ hike this week. USDJPY has exhibited a 105-pip range, with the latest dip below 155 now probing last week’s lows. Below here, the December 05 low at 154.35 and the 50-day EMA at 153.95 represent an important support area as we navigate both the US data releases and BOJ meeting.

- At the other end of the G10 leaderboard, NZD has notably declined amid comments from the newly appointed RBNZ Governor. Breman said the forward path for the OCR published in the November policy statement “indicates a slight probability of another rate cut in the near term”, pushing back against any expectations for a hike in 2026. NZDUSD is 0.35% lower on the session and back below 0.58, while AUDNZD briefly rose to a recovery high of 1.1520.

- Elsewhere, USDKRW has extended session losses to nearly 1% after South Korea’s National Pension Service said it will conduct its strategic FX hedging in a “flexible” manner. USDKRW gathered downside momentum through the overnight lows at 1470 and notably, we are now below 20-day EMA support – a close below this average would be the first since September.

- Fed's Miran and Williams are scheduled to appear later today, while US empire manufacturing and the NAHB housing market index are on the calendar in terms of data.

EGBS: German 5s30s Flattens Intraday But Several Risk Events to Come This Week

- The German 5s30s curve has flattened 1.5bps today, with the 5-year yields down 0.5bps and 30-year yields down 2bps. This week’s regional calendar is heavy, with focus not only on incoming data (December flash PMIs on Tuesday) and monetary policy decisions (ECB on Thursday), but also 2026 issuance plans. Germany’s issuance plan is due on Thursday, and the maturity skew may determine whether 5s30s can break out of the 93-111bp range seen since September.

- Bund futures are in consolidation mode. A bear-mode cycle is intact and the contract is trading closer to its recent lows. Initial resistance is the Dec 8 high at 128.08.

- 10-year EGB spreads to Bunds are up to 1.5bps narrower on the session, led by BTPs. The BTP/Bund spread is now at 67.5bps, narrowing the gap to the 2009 low of ~65.4bps.

- In France, focus remains on political headline flow surrounding the 2026 State budget, which is expected to be passed in the Senate today. A Joint Committee of senators and National Assembly parliamentarians will then try and find an (unlikely) compromise on Friday.

- Eurozone October industrial production was in line with consensus at 0.8% M/M (vs 0.2% prior).

GILTS: Bull Flattening to Start Heavy Event Risk Week

Gilts have followed core global FI peers away from Friday lows, with futures rallying to ~91.30

- Initial technical parameters remain unchanged

- Recent price action in futures highlights 90.53, the Nov 25/26 low, and 91.93, the Nov 27 high, as the important short-term directional triggers.

- Yields 1.5-3.5bp lower, curve flattens after 2s10s and 5s30s rallied ~8bp from their respective post-Budget closing lows.

- Multi-week ranges in the short end remain intact.

- 22bp of easing priced for Thursday’s BoE decision, with 63bp of cumulative cuts priced through the end of ’26.

- December ’26 meeting pricing extends the dovish rebound after failing to break below 50bp of easing during recent rounds of hawkish repricing.

- SONIA futures flat to +2.5, SFIZ6 pierces Friday’s high.

- CPI (Tuesday) & labour market (Wednesday) data are due ahead of the BoE decision.

- The Bank will receive both of the releases this morning and as long as there are no notable surprises, we expect Governor Bailey to join the four dovish dissenters from the November meeting, which would mean that the Bank would deliver a 25bp cut.

- Expect our full suite of previews and reviews around those events.

- Some early focus on an article noting that Indeed wage tracking points to slower wage growth for lower paid workers (the cohort’s wage growth had been fairly resistant to BoE tightening), although wage growth only slowed to +5.9% Y/Y in October from a 7-month high of +6.6% in September.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.758 | -21.7 |

Feb-26 | 3.690 | -28.5 |

Mar-26 | 3.595 | -38.0 |

Apr-26 | 3.485 | -49.0 |

Jun-26 | 3.439 | -53.6 |

Jul-26 | 3.378 | -59.7 |

Sep-26 | 3.365 | -61.0 |

Nov-26 | 3.347 | -62.8 |

Dec-26 | 3.345 | -63.0 |

EQUITIES: Short-Term Cycle Highs for E-Mini S&P Last Week Strengthens Bull Theme

A bull cycle in Eurostoxx 50 futures remains intact and the contract is trading closer to its recent highs. Price is also trading above the 20- and 50-day EMAs, and has cleared 5742.40, 76.4% of the Nov 13 - 21 bear leg. The breach of this price point paves the way for an extension towards 5825.00, the Nov 13 high and the bull trigger. First key support to watch lies at 5641.23, the 50-day EMA. A bull cycle in S&P E-Minis remains intact and a fresh short-term cycle high last week strengthens the bull theme. Sights are on 7014.00, the Oct 30 high and bull trigger. Clearance of this hurdle would confirm a resumption of the primary uptrend. This would open the 7044.82 area, a Bollinger band resistance. Initial firm support to watch lies at 6828.90, the 50-day EMA. Key support and a reversal trigger is at 6583.00, the Nov 21 low.

- Japan's NIKKEI closed lower by 668.44 pts or -1.31% at 50168.11 and the TOPIX ended 7.64 pts higher or +0.22% at 3431.47.

- Elsewhere, in China the SHANGHAI closed lower by 21.425 pts or -0.55% at 3867.921 and the HANG SENG ended 347.91 pts lower or -1.34% at 25628.88.

- Across Europe, Germany's DAX trades higher by 63.96 pts or +0.26% at 24251.62, FTSE 100 higher by 62.85 pts or +0.65% at 9712, CAC 40 up 63.45 pts or +0.79% at 8132.47 and Euro Stoxx 50 up 27.24 pts or +0.48% at 5748.43.

- Dow Jones mini up 199 pts or +0.41% at 48673, S&P 500 mini up 29.5 pts or +0.43% at 6860.25, NASDAQ mini up 109.25 pts or +0.43% at 25322.75.

Time: 10:00 GMT

COMMODITIES: MA Studies for WTI Highlights a Dominant Medium-Term Downtrend

A bearish theme in WTI futures remains intact and the move down last week reinforces this theme. Note that moving average studies are in a bear-mode position, highlighting a dominant medium-term downtrend. A continuation of the bear leg would open key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. Gold traded higher last week, reinforcing a bullish theme. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4069.6. Clearance of this EMA would signal scope for a deeper retracement. Attention is on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude up $0.08 or +0.14% at $57.48

- Natural Gas up $0.01 or +0.32% at $4.126

- Gold spot up $45.3 or +1.05% at $4343.61

- Copper up $5.8 or +1.08% at $542.15

- Silver up $1.77 or +2.86% at $63.6921

- Platinum up $23.27 or +1.33% at $1770.67

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 15/12/2025 | 1315/0815 | ** | CMHC Housing Starts | |

| 15/12/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 15/12/2025 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 15/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 15/12/2025 | 1330/0830 | *** | CPI | |

| 15/12/2025 | 1430/0930 | Fed Governor Stephen Miran | ||

| 15/12/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 15/12/2025 | 1530/1030 | New York Fed's John Williams | ||

| 15/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/12/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 16/12/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | Italy Final HICP | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI (f) | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Services PMI (f) | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Composite PMI (f) | |

| 16/12/2025 | 1000/1100 | * | Trade Balance | |

| 16/12/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 16/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 16/12/2025 | 1000/1100 | Foreign Trade | ||

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (f) | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Services Index (f) | |

| 16/12/2025 | 1500/1000 | * | Business Inventories | |

| 16/12/2025 | 1730/1230 | BOC Gov Macklem speech in Montreal | ||

| 17/12/2025 | 2350/0850 | * | Machinery orders |