MNI US OPEN - Trump, Takaichi Sign Key Minerals Deal

EXECUTIVE SUMMARY:

- TRUMP, TAKAICHI SIGN MINERAL DEAL AND FORMAL INVESTMENT PLEDGE

- FT SEES £20BLN PRODUCTIVITY HIT TO UK PUBLIC FINANCES

- CHINA VOWS TO SIGNIFICANTLY BOOST ROLE OF HOUSEHOLD CONSUMPTION

- TIGHTER CREDIT STANDARDS, LOWER INFLATION EXPECTATIONS SEEN IN ECB SURVEYS

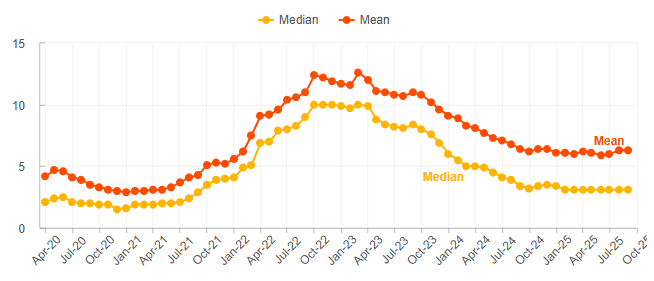

Figure 1: ECB inflation expectations survey won't shut door on another rate cut

Source: ECB

NEWS:

US-JAPAN (MNI): Trump & Takaichi Sign Mineral Deal And Formalise Investment Pledge

US President Donald Trump and Japanese Prime Minister Sanae Takaichi have signed a critical mineral framework: 2025 and formalised the implementation of

a Japanese investment pledge from Tokyo to ease a Memorandum of Understanding on trade that would cap tariffs on Japanese exports at 15% - including on autos -, signed on September 4. At 06:00 ET 10:00 GMT 19:00 JST, Trump will participate in a reception with Japanese business leaders, where Toyota is expected to announce a plan to manufacture cars in the US.

US-JAPAN (BBG): Bessent Avoids Pressing Hard on BOJ Policy in Tokyo Visit

US Treasury Secretary Scott Bessent refrained from weighing deeply into Bank of Japan monetary policy in talks, according to his Japanese counterpart Satsuki Katayama, despite having previously describe the BOJ as “behind the curve” on inflation. Japan’s new Finance Minister Katayama told reporters that the two officials didn’t make the BOJ’s policy a main talking point at their first meeting in Tokyo. The two spoke for more than an hour, with Bessent noting that Japan’s stock market is welcoming Katayama as the Nikkei 225 stock index crested 50,000 for the first time Monday, she said.

UK (BBG): UK Wealth Fund Unlikely to ‘Shift Dial’ on Growth, MPs Warn

Chancellor of the Exchequer Rachel Reeves’ attempt to boost growth by luring in private investment through the National Wealth Fund will be held back by its limited size, an influential group of British lawmakers said. The Treasury Committee warned on Tuesday that ambitions for the fund to deliver significant economic benefits are “very challenging” after hearing that its size pales in comparison to similar efforts in France and Germany.

UK (MNI): FT Sees £20bn Hit to UK Public Finances From Productivity Downgrade

The FT reported yesterday evening that the OBR is expected to cut its trend productivity forecast by 0.3pp, larger than the 0.1-0.2pp that had been

expected by most analysts/independent forecasters. The IFS' Green Budget estimated that each 0.1pp downgrade to productivity would increase 2029-2030

PSNB by GBP7bln, so this downgrade implies a GBP21bln hit to public finances. A reminder that the YTD tracking error with existing OBR projections is also

GBP7.23bln.

CHINA (MNI): China Signs Upgraded ASEAN 3.0 FTA

China has officially signed an upgraded Free Trade Agreement (FTA) with ASEAN nations, according to the Ministry of Commerce on Tuesday. The FTA 3.0 upgrade encompasses nine key areas such as the digital economy, green economy, supply chain connectivity and customs procedures and trade facilitation. The upgraded agreement reflects a shared resolve among members to collaborate on addressing global trade and economic challenges, the ministry said.

CHINA (BBG): China Vows to Significantly Boost Household Consumption Rate

China pledged to significantly boost the rate of consumption growth in the next five-year planning period starting from 2026. The Communist Party made the pledge Tuesday in a detailed communique that followed its fourth plenum held last week in Beijing.

US/CHINA (BBG): China Advisor Expects US to Ease Export Curbs for Magnet Relief

An adviser to the Chinese government expects the US to make export control concessions in exchange for winning relief on Beijing’s most potent trade weapon this week when presidents Xi Jinping and Donald Trump meet. Top trade negotiators have teed up a deal for their leaders to finalize Thursday in South Korea on issues spanning tariffs, shipping fees, fentanyl and export controls. As part of that, US Treasury Secretary Scott Bessent said China would delay its latest rare-earth rules “for a year.”

PHILIPPINES (BBG): Philippines Allowing Market to Determine FX as Peso Slumps

The Philippine central bank is letting market forces set the dollar-peso exchange rate, saying that strong remittances and economic growth will support the local currency which hit a record low on Tuesday. “The Bangko Sentral ng Pilipinas allows the exchange rate to be determined by market forces,” it said in a statement. “When we do participate in the market, it is largely to dampen inflationary swings in the exchange rate over time rather than to prevent day-to-day volatility.”

DATA:

EUROZONE (MNI): Tighter Credit Standards Seen In Q3 - ECB Survey

Euro area banks reported a small net tightening of credit standards for loans or credit lines to enterprises in Q3 2025, the ECB's Bank Lending Survey showed on Tuesday. Credit standards for loans to households for house purchases were seen unchanged, although there was moderate net tightening for consumer credit and other lending to households.

EUROZONE (MNI): EZ Inflation Expectations Inch Lower In September

Eurozone consumer inflation expectations for the next 12 months decreased to 2.7% in September from 2.8% in August, according to an ECB survey on Tuesday.

Expectations for inflation three years ahead were unchanged at 2.5%, the Consumer Expectations Survey showed, as were those for five years ahead, which remained unchanged at 2.2%.The perceived rate of inflation over the previous 12 months was unchanged at 3.1% for the eighth consecutive month, versus Eurostat's headline inflation measure of 2.2% in September.

JAPAN (MNI): Japan Sept Trimmed Mean Rises 2.1%; Aug 2.0%

Japan’s trimmed-mean measure of underlying inflation rose 2.1% y/y in September, up from 2.0% in August, marking the eighth straight month above 2%, data released by the Bank of Japan showed on Tuesday. This suggests that cost pass-throughs — such as the impact of high rice prices and elevated labour costs — continued, though they appear to be slowing.

MNI: GERMANY NOV GFK CONSUMER CLIMATE -24.1 (OCT -22.5)

FOREX: Yen Snaps Losing Streak Following Sharp Rebound

- Japanese yen volatility has been the key feature for G10 FX markets on Tuesday, following details emanating surrounding the discussions between US and Japanese administrations. The US Treasury provided a read out of the Treasury Secretary and Japan FinMin meeting, with Bessent emphasizing the need for sound monetary policy to keep inflation expectations anchored and avoid FX volatility.

- USDJPY is currently down 0.65%, with the 151.76 session lows marking a 1% correction from yesterday’s highs of 153.26. First important support to watch lies at 151.09, the 20-day EMA.

- Weakness for GBP in early trade puts GBPUSD through yesterday’s lows of 1.3311 on decent volumes: GBP futures volumes suggest a flow-driven move rather than a headline or news trigger spell of weakness. The fiscal picture remains the key driver more broadly, particularly given the increasing signs that the Chancellor will have to raise income tax at this month’s budget to fill a widening fiscal hole. The GBPUSD bear trigger remains 1.3249, the October 14 low.

- NOK meanwhile also underperforms on pressured oil prices as fears around how much crude is actually coming off the market from earlier Russia sanctions have somewhat subsided. Expect global developments to continue dictating NOK price action in the near-term, with little in the way of market moving domestic data due ahead of Norges Bank's November decision. EURNOK stands at 11.67, with next resistance at 11.83, the Oct 17 high.

- Attention turns to central banks for the remainder of the week, with the Bank of Canada and FOMC both firmly seen to deliver cuts tomorrow, while the BoJ and ECB are expected to hold rates in their respective meetings on Thursday. Australian CPI and Spanish GDP are due Wednesday.

BONDS: Interaction With Key Trendline Support Key For 10-year Gilt Yields

10-year Gilt yields are hovering just above a key support zone. A clear break of trendline support drawn from the November 2022 low (around 4.35% today) would set the stage for a deeper pullback in yields. Gilts are outperforming German bonds across the curve, with the 10-year Gilt/Bund spread down 2bps on the session and below the year-to-date low of 177.5bps seen in March.

- There are increasing signs that UK Chancellor Reeves will have to raise income tax at the November 26 budget to fill a widening fiscal hole, and potentially increase headroom above the ~GBP10bln seen at previous fiscal events. The FT reported yesterday evening that the OBR is expected to cut its trend productivity forecast by 0.3pp.

- The Gilt curve has bull steepened, with 2-year yields down 3bps and 30-year yields down 2.5bps. Meanwhile, the German curve has seen a horizontal shift lower, with yields down 0.5-1bp across tenors.

- In futures, Bunds are +10 ticks at 129.67, while Gilts are +23 at 93.88. A bullish theme in Gilt futures remains intact.

- There’s plenty of EGB supply due today, which is likely containing rallies at the short-end. Germany will come to the market today with E4bln of the 2.20% Oct-30 Bobl, while Italy is holding a BTP Short Term auction. Slovakia and Finland are also holding syndications today, the latter a USD issue.

- The ECB’s Q3 BLS broadly echoed the signals from yesterday’s September credit data and SAFE survey. ECB 1/3/5-year consumer expectations were steady at 2.7%, 2.5% and 2.2% respectively.

- Focus remains on Thursday’s ECB decision, alongside the Eurozone flash Q3 GDP and October inflation readings. In the UK, fiscal headline alongside any UST spillovers will be in focus.

EQUITIES: Trend Condition for Equities Remains Bullish

The trend condition in S&P E-Minis remains bullish and the contract traded higher Monday, as it started the week on a bullish note. The fresh cycle high confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. The 6900.00 handle has been cleared, opening 6953.25 next, a Fibonacci projection. Initial firm support to watch lies at 6748.48, the 20-day EMA. The trend structure in Eurostoxx 50 futures is bullish. Monday’s fresh cycle high reinforces a bull theme and maintains the rising price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 5727.18, a Fibonacci projection. First support lies at 5625.31, the 20-day EMA.

- Japan's NIKKEI closed lower by 293.14 pts or -0.58% at 50219.18 and the TOPIX ended 39.18 pts lower or -1.18% at 3285.87.

- Elsewhere, in China the SHANGHAI closed lower by 8.721 pts or -0.22% at 3988.224 and the HANG SENG ended 87.56 pts lower or -0.33% at 26346.14.

- Across Europe, Germany's DAX trades lower by 74.47 pts or -0.31% at 24233.55, FTSE 100 higher by 5.5 pts or +0.06% at 9659.08, CAC 40 down 18 pts or -0.22% at 8221.18 and Euro Stoxx 50 down 15.51 pts or -0.27% at 5695.55.

- Dow Jones mini up 8 pts or +0.02% at 47720, S&P 500 mini down 0.5 pts or -0.01% at 6907.75, NASDAQ mini up 9.75 pts or +0.04% at 25973.25.

COMMODITIES: Gold Extends Bear Cycle

The latest recovery in WTI futures appears corrective for now, however, note that price has traded through resistance at the 50-day EMA, at $61.14. The breach of this average signals scope for a stronger recovery. A resistance at $62.34, the Oct 8 high, has been pierced. A clear break of it would expose key resistance at $65.77, the Sep 26 high. Key support and the bear trigger has been defined at $55.96, the Low Oct 20. Gold is trading lower as it extends the bear cycle that started Oct 20. Note that the trend is overbought and a deeper retracement is allowing this condition to unwind. Support at the 20-day EMA, at $4045.9, has been breached, signalling scope for a deeper retracement, towards the 50-day EMA, at $3838.2. Key resistance and the bull trigger has been defined at $4381.5, the Oct 20 high. Initial resistance is at $4161.4, the Oct 22 high.

- WTI Crude down $1.2 or -1.96% at $60.07

- Natural Gas down $0.15 or -4.21% at $3.295

- Gold spot down $84.78 or -2.13% at $3901.9

- Copper down $6.85 or -1.32% at $510.1

- Silver down $1.18 or -2.51% at $45.7186

- Platinum down $54.93 or -3.46% at $1536.07

| Date | GMT/Local | Impact | Country | Event |

| 28/10/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 28/10/2025 | - | FOMC Meeting | ||

| 28/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/10/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 28/10/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/10/2025 | 1400/1000 | ** | housing vacancies | |

| 28/10/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 28/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/10/2025 | - | Bank of Japan Meeting | ||

| 29/10/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 29/10/2025 | 0030/1130 | *** | CPI Inflation Monthly | |

| 29/10/2025 | 0030/1130 | *** | CPI inflation | |

| 29/10/2025 | 0700/0800 | Flash Quarterly GDP Indicator | ||

| 29/10/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 29/10/2025 | 0800/0900 | *** | GDP (p) | |

| 29/10/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 29/10/2025 | 0930/0930 | ** | BOE M4 | |

| 29/10/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 29/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 29/10/2025 | 1100/1200 | ** | PPI | |

| 29/10/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/10/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 29/10/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 29/10/2025 | 1430/1030 | BOC press conference | ||

| 29/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 29/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/10/2025 | 1800/1400 | *** | FOMC Statement |