MNI US OPEN - Trump-Putin Meeting Set for 1500ET

EXECUTIVE SUMMARY:

- TRUMP-PUTIN MEETING SET TO START FROM 1500ET

- CEASEFIRE, SANCTIONS AND FUTURE OF UKRAINE SET TO BE DISCUSSED

- WHITE HOUSE COULD TAKE STAKE IN INTEL

- CHINA INDUSTRIAL PRODUCTION, RETAIL SALES SLOWING FASTER THAN EXPECTED

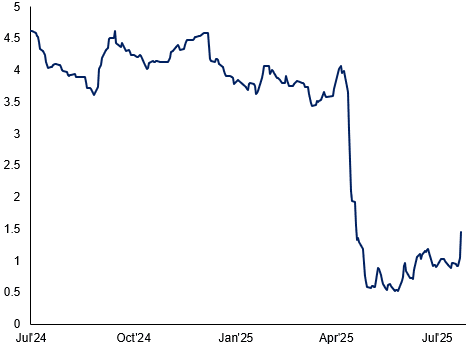

Figure 1: Hong Kong's 1m HIBOR fixes higher as tighter liquidity grips local market

NEWS

US-RUSSIA (MNI): Trump-Putin Summit Schedule:

The high-profile summit between US President Donald Trump and his Russian counterpart, Vladimir Putin, gets underway later today in Anchorage, Alaska. Trump is set to leave the White House at 06:45ET (11:45BST/12:45CET/19:45JST) and arrive at around 11:00 local time (15:00ET/20:00BST/21:00CET/04:00JST). He will then depart for Washington, D.C., at 17:45 local time (21:45ET/02:45BST/03:45CET/10:45JST), giving the two leaders just under seven hours together.

US (BBG): Trump Administration Said to Discuss Taking Stake in Intel

The Trump administration is in talks with Intel Corp. to have the US government take a stake in the beleaguered chipmaker, according to people familiar with the plan, in the latest sign of the White House’s willingness to blur the lines between state and industry.

NEW ZEALAND (MNI): MPC Likely To Cut 25bp To 3%

The Reserve Bank of New Zealand is likely to cut the Official Cash Rate by 25 basis points to 3% next Wednesday, as unemployment rises and economic growth remains sluggish.

CHINA (MNI): China Consumption Confidence Needs Improvement

China’s domestic consumption confidence needs to be improved and enhanced, after July’s economic data showed total retail sales increased 3.7% year-on-year, lower than the 5.0% rise during H1, Fu Linghui, spokesperson for the National Bureau of Statistics, told reporters on Friday.

TAIWAN (BBG): Taiwan Lifts 2025 Growth Forecast, Defying US Tariff Worries

Taiwan raised its estimate for growth in 2025, easing some concern over the impact of US duties on an economy that has roared on tech exports. Gross domestic product is set to expand 4.45% this year, the statistics bureau in Taipei said in a statement on Friday – its first estimate since the Trump administration hit the archipelago’s shipments with 20% tariffs. The new figure is up from the 3.1% predicted in May.

DATA

China’s consumption and production slowed to their weakest pace this year in July, while investment growth hit a near five-year low, National Bureau of Statistics data showed Friday. Retail sales rose 3.7% y/y, down from June’s 4.8% and missing the 4.6% forecast. Industrial output grew 5.7% y/y, the lowest reading this year, compared with June’s 6.8% and below the 6.0% forecast.

JAPAN (MNI): Japan Q2 GDP Rises 0.3% Q/Q; Annualised +1.0%

Japan’s economy grew 0.3% q/q, or an annualised 1.0%, over Q2, supported by strong capital investment, solid private consumption and a positive contribution from net exports, preliminary Cabinet Office data showed Friday. The result marked the fifth straight quarter of growth and exceeded the MNI median forecast of +0.1% q/q, or +0.2% annualised, suggesting limited impact from U.S. trade policy in Q2.

SWITZERLAND (MNI): Q2 Flash GDP Stronger Than Expected

Swiss Q2 flash GDP (seasonally- and sport event-adjusted) was stronger than expected, at 0.1% Q/Q (vs -0.1% consensus). "The negative performance in industry has been counterbalanced by gains in the services sector", SECO comments. This follows the strong 0.8% in Q1 which was underpinned by US tariff front-running but also showed wider strength, for example in services. A final Q2 print with drivers by expenditure component and industry is scheduled to be released on August 28.

EGBS: Bear Steepening Trend Persists

The German 10s30s curve is another 1bp steeper this morning at 56bps, nearing the 2021 high of 57bps. It’s more a continuation of this year’s trend, rather than in response to any fresh catalyst. Key drivers of long-end bear steepening through 2025 include increased fiscal/issuance pressure in Germany and Dutch pension fund reform.

- Since January, Buxl ASWs (vs 3-month Euribor) are essentially unchanged at -36bp. That’s likely because increased issuance pressures push rates higher via the bond leg, while pension fund reforms impact the swap leg.

- As noted above, 30-year yields are up 3bps today and looking to retest Tuesday’s 14-year high of 3.308%.

- Bund futures are -34 ticks at 129.17. Initial support is the 129.00 figure, which shields key support and the bear trigger at 128.84 (Jul 25 low).

- 10-year EGB spreads to Bunds are between -0.5 and +1.0bps today. BTPs are surprisingly a little wider despite today’s 0.6% rally in European equity futures.

- There may be some interest in Ireland after hours, with Moody’s potentially providing a ratings update (current rating: Aa3; Outlook Positive).

- However, primary focus remains on this afternoon’s US data and the outcome of today’s Trump-Putin meeting in Alaska.

GILTS: Bear Steepening On Global Cues

Core global FI markets remain on the defensive this morning.

- European/London participants were quick to fade the Asia recovery in wider core global FI, reversing an opening rally in gilts.

- Ongoing spill over from yesterday’s U.S. PPI data and some focus on the impending Trump-Putin meeting in Alaska is noted, but it’s probably a stretch to deem either of those factors a meaningful driver of this morning’s moves.

- Short-term technicals in futures screen bearish, with the break of yesterday’s base and the August 1 low (91.44) deepening that picture.

- The contract has traded as low as 91.37.

- The next downside target resides at the July 18 base/bear trigger (91.08).

- Yields are flat to +2.5bp, curve biased steeper.

- 5s30s is on for a fresh cycle closing high and is testing the mid-July intraday top (145.77bp). A break there would expose the April intraday high (147.22bp).

- SONIA futures are little changed to -2.5.

- 14bp of BoE cuts priced into OIS through year-end, with the next 25bp move still virtually fully discounted through the February MPC.

- U.S. retail sales and the UoM survey headline the broader data calendar ahead of the weekend.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.973 | +0.6 |

Nov-25 | 3.886 | -8.2 |

Dec-25 | 3.829 | -13.8 |

Feb-26 | 3.722 | -24.5 |

Mar-26 | 3.679 | -28.8 |

Apr-26 | 3.603 | -36.5 |

FOREX: USD/JPY Remains Weaker After Conclusion of Consolidation Phase

- The USD Index trades rangebound and inside the Thursday range after the PPI print yesterday helped prompt a minor recovery in the greenback. This keeps prices either side of the 50-dma which, notably, has begun to flatten out after maintaining a solid downtrend throughout 2025.

- JPY is the strongest currency in G10, extending the breakout and bearish conclusion of the consolidation phase in USD/JPY. Recent weakness puts the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition, keeping the downside argument in focus.

- Anticipation ahead of the Putin-Trump meeting will likely continue to dominate sentiment, particularly after Putin's positivity in comments earlier this week helped support the e-mini S&P to a new record high.

- We noted yesterday the pressure building on USD/HKD, with price action not matching the pattern of HKMA intervention. That move extended overnight, and is still building at typing, putting spot down to new pullback lows of 7.8119 shortly after the European open. Overnight swap rates have surged further still Friday (hitting 1.7% at typing), well ahead of the 0.3% prevailing rate mid-week and should continue to support a recovery in HIBOR fixes ahead. Today's 1m HIBOR fixed higher by 41bps, hitting 1.45% for the highest fix since mid-May. It's these factors that should work against the HKD carry trade (selling HKD, buying USD), evident in the further tightening of the HKD forward discount today: down 975 points from as high as 1270 this month.

- Just ahead of today's close, Presidents Trump and Putin are set to meet in Alaska. The meeting is set to continue for an indeterminate period of time before, reportedly, the Presidents will hold a joint press conference (however Trump stated that a joint appearance would be contingent on results of the meeting itself). Any appearance is likely to be well after the market close, leaving any reaction to Monday trade.

EQUITIES: New Highs for E-mini S&P

This morning saw new record highs in the e-mini S&P, extending gains on the clearance of resistance through the 6477.31 mark. This cements the underlying uptrend, exposing projection levels into 6523.63 next. The bounce off post-NFP lows in global equity indices persists, with the Eurostoxx 50 future recovering back above the 50-day EMA. Markets look to build a base above this level, through which additional strength refocuses attention on 5486.00, the May 20 high and bull trigger.

- Japan's NIKKEI closed higher by 729.05 pts or +1.71% at 43378.31 and the TOPIX ended 49.73 pts higher or +1.63% at 3107.68.

Elsewhere, in China the SHANGHAI closed higher by 30.328 pts or +0.83% at 3696.771 and the HANG SENG ended 249.25 pts lower or -0.98% at 25270.07. - Across Europe, Germany's DAX trades higher by 91.87 pts or +0.38% at 24468.68, FTSE 100 lower by 6.39 pts or -0.07% at 9170.84, CAC 40 up 56.25 pts or +0.71% at 7926.59 and Euro Stoxx 50 up 22.3 pts or +0.41% at 5457.

- Dow Jones mini up 311 pts or +0.69% at 45308, S&P 500 mini up 4.25 pts or +0.07% at 6494.75, NASDAQ mini down 46.75 pts or -0.2% at 23883.5.

COMMODITIES: Gold Prices Hold Above Weekly Low

Gold prices are off the weekly low, however bounces appear shallow at these levels, keeping price within the mid-point of the recent range. The phase of weakness into the end of July supported the view that short-term pullbacks are corrective - for now. WTI futures traded poorly into the Wednesday close, extending losses on the clearance of the 50-day EMA and bear trigger. Markets have built on this S/T momentum lower, with support breaking at $62.77.

- WTI Crude down $0.7 or -1.09% at $63.27

- Natural Gas up $0.02 or +0.81% at $2.863

- Gold spot up $6.21 or +0.19% at $3341.42

- Copper up $1.4 or +0.31% at $455.6

- Silver down $0.08 or -0.21% at $37.948

- Platinum down $6.15 or -0.45% at $1353.47

| Date | GMT/Local | Impact | Country | Event |

| 15/08/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/08/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/08/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/08/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/08/2025 | 1315/0915 | *** | Industrial Production | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 15/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 2000/1600 | ** | TICS |