MNI US OPEN - Trump Makes Rare Earths Deal With Australia

EXECUTIVE SUMMARY

- TRUMP MAKES RARE EARTHS DEAL WITH AUSTRALIA TO FIGHT CHINA

- ECB’S LANE SAYS MONETARY POLICY IS BEING TRANSMITTED SMOOTHLY

- BOJ IS SAID TO BE CLOSER TO RATE HIKE WITH LITTLE NEED TO RUSH: BBG

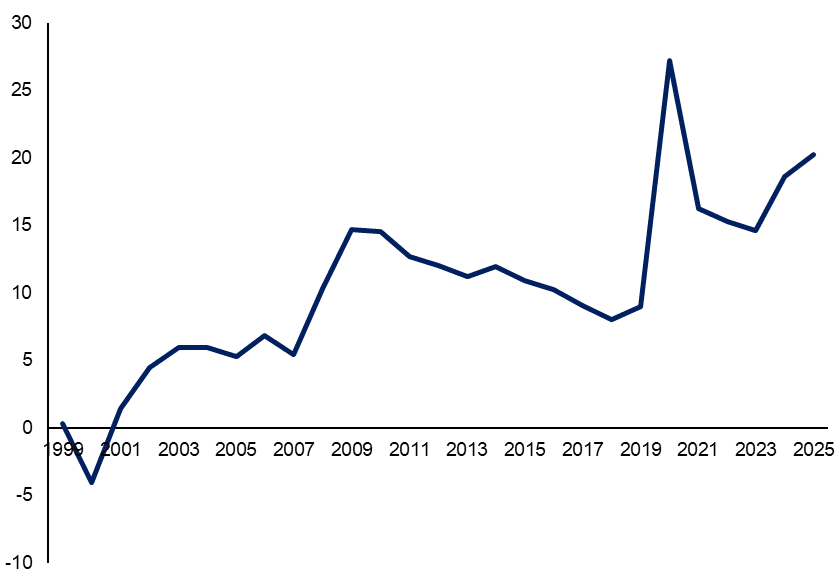

- UK GOVERNMENT'S SEPTEMBER BORROWING AT 5-YEAR

Figure 1: Highest SeptemberUK PSNB outside of COVID

Source: MNI, Bloomberg Finance L.P.

NEWS

US/CHINA/AUSTRALIA (BBG): Trump Makes Rare Earths Deal With Australia to Fight China

US President Donald Trump signed a landmark pact with visiting Australian Prime Minister Anthony Albanese to boost America’s access to rare earths and other critical minerals, an effort to counter China’s tight grip on the supply chains of key metals. The two governments will jointly invest in a swathe of mines and processing projects in Australia to boost production of commodities used in advanced technologies from electric vehicles to semiconductors and fighter planes. Australia has an $8.5 billion “pipeline that we have ready to go,” Albanese said at a meeting between the two leaders at the White House.

US (WSJ): U.S. Banks Are Hunting for Collateral to Back $20 Billion Argentina Bailout

A group of banks including JPMorgan Chase, Bank of America and Goldman Sachs is struggling to put together a $20 billion loan to Argentina without leaving themselves on the hook to the virtually-bankrupt South American country, people familiar with the matter said. The bank loans would be part of the Trump administration's plan to backstop the finances of libertarian President Javier Milei's government with a $40 billion package, including a $20 billion currency swap with the U.S. Treasury Department and the separate $20 billion bank-led debt facility.

ECB (BBG): ECB’s Lane Says Monetary Policy Is Being Transmitted Smoothly

European Central Bank monetary easing is proceeding well but must be constantly monitored in case changes require more action, Chief Economist Philip Lane said. “In overall terms, monetary policy transmission is progressing smoothly,” Lane said Tuesday. “It makes sense to maintain a meeting-by-meeting and data-dependent approach to assessing the strength of monetary transmission at any given point in time.”

UK (MNI): Red Tape Cuts to Save Businesses GBP 6bln - Reeves

Deregulation will save UK businesses nearly GBP 6bln per year in "pointless" administrative costs by the end of the Parliament, Chancellor of the Exchequer Rachel Reeves will announce on Tuesday. "A central part of our Industrial Strategy is slashing needless red tape that blocks business growth," Business & Trade Secretary Peter Kyle said. In March, a government action plan was published, with a then stated aim to save businesses 'billions' of pounds a year by removing 'red tape' from planning and business as part of the Plan for Change to kickstart economic growth.

RIKSBANK (MNI): Riksbank’s Head Sees Growth Pick-Up, Rates on Hold

There were a number of factors pointing to an acceleration in Sweden's growth from currently subdued levels, Riksbank Governor Erik Thedeen told lawmakers on the Finance CommitteeTuesday, adding that the most recent guidance that the bank's view was that "interest rates will remain at this level for some time." The Swedish central bank has been at the front of the pack in easing monetary policy this cylce, cutting the policy rate to just 1.75%. Thedeen said that while inflation has been somewhat elevated they felt more confident that it was coming down and had eased to support the economy.

BOJ (BBG): BOJ Is Said to Be Closer to Rate Hike With Little Need to Rush

Bank of Japan officials are of the view there’s no urgency to hike the benchmark rate next week even as the economy is making progress toward achieving their price target, according to people familiar with the matter. The officials see the likelihood has continued to rise gradually for their outlook to be achieved as the economy and inflation develop more or less in line with their expectations, according to the people.

JAPAN (MNI): Cabinet Ministers Confirmed w/New PM to Deliver Presser at 22:00JST

Following the election of Liberal Democratic Party (LDP) President Sanae Takaichi as Japan's first-ever female prime minister earlier today, the incoming Chief Cabinet Secretary (CCS) Minoru Kihara is announcing the identity of those who will serve in her first Cabinet. As expected, outgoing CCS and third-placed challenger in the LDP leadership contest Yoshimasa Hayashi becomes Internal Affairs and Communications Minister. The runner-up in the leadership contest, Shinjiro Koizumi, becomes Minister of Defence. Reuters reports that Takaichi will hold a presser at 09:00ET/14:00BST/15:00CET/22:00JST.

JAPAN (MNI): New Fin Min: Not Unnatural to Push for Abenomics v.2025

Newly-appointed Finance Minister Satsuki Katayama has been speaking to the press. Says that she is committed to cooperation on tax within the governing coalition. The libertarian-federalist Japan Innovation Party (Ishin), which sits alongside PM-designate Sanae Takaichi's conservative Liberal Democratic Party (LDP) in gov't, laid out the elimination of sales tax on food for two years as one of its key demands to support Takaichi's gov't. Katayama expresses commitment to openly discussing the prospect of a reduction with Ishin.

CHINA (MNI EXCLUSIVE): Relaxed Policy to Drive PBOC Over Next Five Years - Advisors

Advisors share their outlook for monetary policy ahead of China's Five-Year Plan reveal. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA

UK DATA (MNI): UK Government's Sept Borrowing at 5-Year High - ONS

- UK SEP PSNB GBP+20.25 BN

- UK SEP PSNB-X GBP+20.25 BN

- UK SEP CGNCR GBP15.77 BN

- UK SEP PSNCR GBP-10.86 BN

UK government borrowing was GBP20.2 billion in September, GBP1.6 billion (or 8.6%) more than the same period last year and the highest September borrowing since 2020, the Office for National Statistics said Tuesday. Borrowing in the financial year-to-date was GBP99.8 billion, GBP11.5 billion (or 13.1%) more than in the same six-month period of 2024. It is the second-highest April to September borrowing since monthly records began in 1993, after that of the early Covid period in 2020. These will be the last numbers that will be incorporated in the OBR's EFO forecasts which will be used for the Budget. The numbers aren't as bad as had been expected, but the continued tracking above OBR forecasts - mainly due to local authority and public corporation borrowing - will be a concern and likely need upward revisions to the in-year 2025/26 forecasts.

AUSTRALIA DATA (MNI): Improved Q3 Job Ads May Signal Better Q4 Labour Market

SEEK data show that labour demand improved over Q3 while supply remains positive it slowed. With Q3 employment rising only 0.2% q/q down from Q2's 0.6%, SEEK job ads may be signalling some possible improvement over Q4. A stabilisation of the labour market would be helpful for monetary policy decision makers if inflation prints to the upside.

FOREX: JPY Weaker, Anticipating Takaichi Policy Set

- The USD sits higher against most others in G10 early Tuesday, although price action is generally contained, despite moderately lower equities from the off.

- JPY is in focus on the confirmation for Takaichi as prime minister, with Katayama taking the finance minister role, reinforcing expectations for a fiscal phase prioritizing an Abenomics-like policy set. Resultantly, JPY is weaker against all others in G10, helping USD/JPY to make light work of Y151.50 and reverse a large part of last week's late weakness. Finance Minister Katayama stopped well short of any critique of the Bank of Japan, instead referring to the currency, which should: "move stably, reflecting fundamentals".

- The recovery from last Friday’s low in USDJPY is beginning to highlight a stronger bullish signal. The pair has found support below the 20-day EMA and note that Friday’s price pattern is a hammer candle formation. If correct, the pattern signals the end of a corrective pullback that started Oct 10, and highlights the fact that support at the 50-day EMA, at 148.94, remains intact. The bull trigger is at 153.27, the Oct 10 high.

- AUD, NZD naturally underperform as a function of cautious risk sentiment and lower equity markets today. AUDUSD continues to trade both sides of the 0.6500 handle, retaining the phase of consolidation. A breach of 0.6440, the Oct 14 low, would cancel any reversal signal and reinstate a bear threat.

- Three CPI prints, Canada scheduled for today, the UK for tomorrow, and the US for Friday, provide the highlights for this week, with the UK release standing out in particular as a downside surprise could bring the potential for a notable BoE repricing. Elsewhere, we watch for fiscal policy signals in Takaichi's press conference later today. A set of ECB speakers is expected to mostly reiterate previous "rates are in a good place" rhetoric, while the Fed remains inside the media blackout.

BONDS: 30-Year Gilt/Bund Spread Down 1bp Following UK Fiscal Data

The 10-year Gilt/Bund spread is 0.5bps tighter at ~192bps, approaching the September 2024 closing low of 191.9bps. Gilts see slightly more outperformance further out the curve though, with the 30-year Gilt/Bund spread 1bp narrower at 213bps. Both the UK and German curves have bull flattened on the session.

- This morning’s UK September public sector finance data was better than expected (PSNB at GBP20.2bln vs 20.8bln cons), contributing to today's moves in Gilt yields. However, September PSNBex was still GBP0.1bln higher than the OBR’s forecast. The current YTD tracking error with the OBR has fallen, but remains at GBP7.2bln.

- Today’s 1.50% Jul-53 Green Gilt auction was soft, with another 0.8bp tail and the lowest accepted price below the pre-auction mid.

- The impact on Gilt futures was limited though. Futures are currently +18 ticks at 92.85, off opening highs of 92.92. A bull cycle remains intact, with initial resistance at last Friday's 93.17 high. This shields the 1.236 proj of the Sep 3 - 11 - 26 price swing at 93.30.

- Bund futures are +14 ticks at 130.07. Small resistance remains at 130.18, with better seen at Friday’s 130.59 high.

- Germany sold Green Bobl/Bunds this morning.

- 10-year EGB spreads to Bunds are biased up to 1bp wider, with European equity futures down 0.2%. Finland will sell 7/10-year RFGBs at 1100BST, while Estonia is holding a E500mln syndicated tap today.

- Eurozone Q2 fiscal data wasn’t a market mover. We’ll provide more commentary on that in due course.

- We don’t expect much from today’s ECB/BOE speakers, with regional focus on tomorrow’s UK CPI report.

EQUITIES: Monday's Gains Reinforce Bullish Eurostoxx Futures Theme

The trend direction in Eurostoxx 50 futures is up and Monday's gains reinforce this theme. The breach of 5689.00, the Oct 2 and bull trigger, confirms a resumption of the uptrend. This maintains the price sequence of higher highs and higher lows and note that MA studies are in a bull-mode position, highlighting a dominant M/T uptrend. Sights are on 5727.18, a Fibonacci projection. First support lies at 5585.83, the 20-day EMA. A bullish theme in S&P E-Minis remains intact and the contract is trading above support at the 50-day EMA. The average, currently at 6621.98, has been pierced but remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. Clearance of this level would undermine a bull theme. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high.

- Japan's NIKKEI closed higher by 130.56 pts or +0.27% at 49316.06 and the TOPIX ended 1.05 pts higher or +0.03% at 3249.5.

- Elsewhere, in China the SHANGHAI closed higher by 52.439 pts or +1.36% at 3916.332 and the HANG SENG ended 168.72 pts higher or +0.65% at 26027.55.

- Across Europe, Germany's DAX trades lower by 13.06 pts or -0.05% at 24245.81, FTSE 100 higher by 19.3 pts or +0.21% at 9422.99, CAC 40 up 5.54 pts or +0.07% at 8211.61 and Euro Stoxx 50 down 4.1 pts or -0.07% at 5676.83.

- Dow Jones mini down 99 pts or -0.21% at 46815, S&P 500 mini down 9.5 pts or -0.14% at 6764.5, NASDAQ mini down 38.75 pts or -0.15% at 25267.

Time: 10:00 BST

COMMODITIES: Gold Falls From Recent Highs But Overall Bullish Theme Intact

A bearish theme in WTI futures remains intact and the move down last week reinforces current conditions. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. Sights are on $54.89 next, the May 5 low, where a break would open $54.10, the Apr 9 low and a key support. Initial firm resistance is seen at $61.76, the 50-day EMA. Key resistance has been defined at $66.42, the Sep 26 high. A bull cycle in Gold remains intact. The latest climb maintains the price sequence of higher highs and higher lows. Sights are on the $4400.00 handle next, and $4404.9, a Fibonacci projection point. Note that the trend is in overbought territory. A move down - a correction - would allow the overbought set-up to unwind. Support to watch lies at $4021.6, the 20-day EMA.

- WTI Crude down $0.15 or -0.26% at $57.37

- Natural Gas up $0.01 or +0.32% at $3.408

- Gold spot down $84.4 or -1.94% at $4271.27

- Copper down $5.65 or -1.12% at $497.95

- Silver down $2.6 or -4.96% at $49.8773

- Platinum down $49.89 or -3.06% at $1583.29

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 21/10/2025 | 1030/1130 | BOE Bailey & Breeden on Private Markets at Financial Services Regulation Committee | ||

| 21/10/2025 | 1100/1300 | ECB Lagarde Keynote at Norges Bank Climate Conference | ||

| 21/10/2025 | 1230/0830 | *** | CPI | |

| 21/10/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 21/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 21/10/2025 | 1300/0900 | Fed Governor Christopher Waller | ||

| 21/10/2025 | 1915/2015 | BOE Mann Fireside Chat at Lazard | ||

| 22/10/2025 | 0600/0700 | *** | Consumer inflation report | |

| 22/10/2025 | 0600/0700 | *** | Producer Prices | |

| 22/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 22/10/2025 | 1100/1300 | ECB de Guindos at Barcelona Real Assets Meeting | ||

| 22/10/2025 | 1225/1425 | ECB Lagarde Keynote at Frankfurt Finance & Future Summit | ||

| 22/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 22/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 22/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 22/10/2025 | 2000/1600 | Fed Governor Michael Barr |

Note: Due to U.S. government shutdown, some data may be unavailable.