MNI US OPEN - Trump Considers Talks with Venezuela's Maduro

EXECUTIVE SUMMARY

- JAPAN SEEKS TO CALM ESCALATING ROW WITH CHINA - RTRS

- TRUMP CONSIDERS TALKS WITH VENEZUELA’S MADURO AMID US MILITARY BUILDUP

- RESUMPTION OF FRANCE BUDGET NEGOTIATIONS KEY TO OAT PERFORMANCE

- JAPAN Q3 GDP DROPS 0.4% Q/Q; ANNUALISED -1.8%

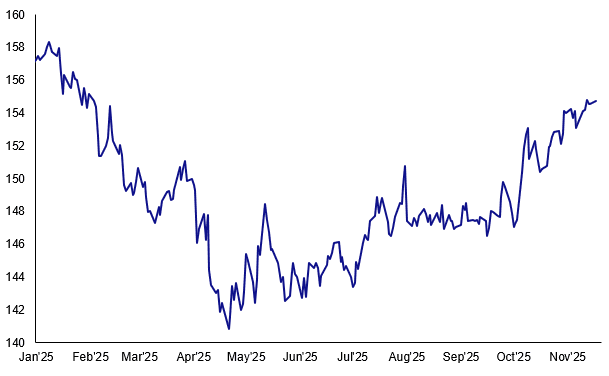

Figure 1: USD/JPY looks to make renewed test of 155.00

Source: MNI, Bloomberg

NEWS

CHINA/JAPAN (RTRS): Japan Seeks to Calm Escalating Row with China

Masaaki Kanai, the Japanese foreign ministry official in charge of Asia and Oceania affairs, arrived in the Chinese capital to meet his counterpart, Liu Jinsong, a video broadcast by the Kyodo news agency showed on Monday. Kanai is expected to explain that Japan's security policy has not changed, and urge China to refrain from actions that damage ties, media said.

US/VENEZUELA (WaPo): Trump Considers Talks With Venezuela’s Maduro Amid U.S. Military Buildup

President Donald Trump said Sunday he's considering talks with Venezuelan President Nicolás Maduro, as a buildup of U.S. forces in the region raises the prospect of military action in Venezuela. The suggestion of potential diplomatic outreach comes after weeks of escalating tensions in the Caribbean. The U.S. has deployed an armada of warships and thousands of American troops to the region, conducted lethal attacks on alleged drug-trafficking boats, authorized covert CIA actions and threatened land attacks in Venezuela. Speaking to reporters Sunday evening, Trump said that Venezuela “would like to talk” and that the United States “may be having some discussions” with Maduro, Venezuela’s strongman president, whom Trump has accused of leading a narcotics organization, the Cartel de los Soles, sending drugs to the United States.

US/RUSSIA (BBG): Trump Says He’d Back Bill to Sanction Russia’s Trading Partners

President Donald Trump said proposed Senate legislation to sanction countries conducting business with Russia would be “okay with me,” his strongest indication yet that he would support a monthslong push to strangle Moscow’s funding. “The Republicans are putting in legislation that is very tough sanctioning, etcetera, on any country doing business with Russia,” Trump told reporters before leaving Florida on Sunday to return to the White House.

FRANCE (MNI): Resumption of Budget Negotiations Key to OAT Performance

2026 Budget negotiations will once again be an important driver of OAT performance this week, with the National Assembly resuming talks on the revenue section today (after a weekend off to battle "fatigue" amongst policymakers). In an interview with Le Parisien over the weekend, Budget Minister Montchalin said that the current make-up of the budget implied a deficit of 5.0% GDP - three tenths above PM Lecornu's 4.7% target. A Le Parisien Senate source suggested the deficit may even be higher: "certainly 5.1 to 5.2%".

UK (BBG): Labour to Unveil UK Migration Crackdown in Bid to Blunt Farage

Keir Starmer’s Labour government plans to make it easier to remove migrants with no rights to stay in the UK, as the prime minister seeks to gain control of the political narrative after one of the most bruising weeks of his 16 months in power. Proposals to speed up the process, including by overhauling human-rights law, are set to be unveiled by Home Secretary Shabana Mahmood in Parliament on Monday as part of what she’ll call the most sweeping reforms to the UK asylum system in modern times.

BOJ (MNI EXCLUSIVE): BOJ Prefers to Wait in Dec, Barring Yen Weakness

MNI discusses the BOJ's policy rate strategy.- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (MNI): Japan Economy Not Weak Despite Q3 Contraction - Gov

The Japanese economy is not weak as a trend, although gross domestic product for the third quarter posted the first contraction in six quarters, a senior Cabinet Office official said. “The GDP contraction was due mainly to temporary factors, such as the drop of housing investment caused (by the government’s rules), and the reaction to the front-loaded export rise in Q2,” the official told reporters.

RBA (BBG): RBA Board Member Backs Flexible Approach to Price, Jobs Goals

The Reserve Bank of Australia pursues a flexible approach to its dual mandate of sustaining employment and reining in inflation, board member Renee Fry-McKibbin wrote in a column in the Australian Financial Review that pushed back at recent commentary. Fry-McKibbin joined the RBA’s monetary policy board in March after leading an independent review of the central bank in 2022-23 which recommended wholesale changes to its functioning including fewer policy meetings, press conferences following each rate decision and the creation of a governance board.

CHILE (MNI): Sunday's General Elections Reveals Expected Market-Friendly Pivot to Right

Chile’s presidential election will head to a second-round run-off on Dec 14, as expected, after no candidate secured an outright majority in yesterday’s first-round vote. Left-wing candidate Jeanette Jara won around 26.8% of the vote, broadly in line with polling, followed by hard-right Jose Antonio Kast, who secured a slightly-better-than-expected 23.9%. In a surprise to the pre-election polling, centrist candidate Franco Parisi came in third, with 19.6% of the vote. Jara and Kast will now head into next month’s run-off, where polling suggests that Kast is likely to win, as right-wing support coalesces around his candidacy. Centre-right candidate Evelyn Matthei (who received 12.6%) has already thrown her support behind Kast, as has libertarian candidate Johannes Kaiser (13.9%).

ECUADOR (BBG): Ecuador Referendum Voters Deliver Stinging Defeat to Noboa

Ecuador’s voters delivered a sharp and surprising repudiation of President Daniel Noboa’s attempt to consolidate power, defying the polls and rejecting his proposals for constitutional reform. In a nationwide referendum, Ecuadorians spurned Noboa’s proposals to create a new constitutional assembly, to allow the return of foreign military bases, to end a state fund for political parties and to slash the number of lawmakers. Surveys leading up to the vote had indicated all four measures would pass.

DATA

EUROPE DATA (MNI): EC Sees Inflation Hovering Around ECB Target

The European Commission's Autumn economic projections see the inflation outlook up slightly from its earlier forecasts in the Spring. Headline euro area inflation is now projected to decline from 2.4% in 2024 to 2.1% in 2025, ease to 1.9% and edge up again to 2.0% in 2027, although "on a quarterly basis, inflation is set to hover around the ECB’s 2% target throughout the forecast horizon," the Commission said. The forecasts assume that ETS2 will come into force in 2027, despite the Nov 5 decision of EU states to suspend the trading scheme for a year to 2028, a decision which the European Parliament has subsequently approved.

SWITZERLAND DATA (MNI): Q3 GDP Downwardly Surprises, Pharma Drags

Swiss GDP growth surprised to the downside in Q3, at -0.5% Q/Q (-0.1% consensus, 0.1% Q2), seeing its worst quarterly growth rate since Q1 2020. While undoubtedly weak, we do not see how the (singular) print should move the needle for the SNB, which views its monetary policy already as "accommodative". Downside pressure on inflation for continued headline CPI readings below 0% would likely be needed to put an SNB cut below 0% firmly on the table again.

ITALY OCT FINAL HICP 1.3% Y/Y (1.3% FLASH, 1.8% SEP) (MNI)

ITALY OCT FINAL HICP -0.2% M/M (-0.2% FLASH, 1.3% SEP) (MNI)

JAPAN DATA (MNI): Japan Q3 GDP Drops 0.4% Q/Q; Annualised -1.8%

Japan’s economy contracted 0.4% q/q, or an annualised -1.8%, in July-September, marking the first decline in six quarters as weak private consumption, housing investment and net exports weighed on activity, preliminary Cabinet Office data showed Monday. The Q3 fall was smaller than the MNI median forecast of -0.7% q/q, or an annualised -2.7%, indicating the pullback following Q2’s front-loaded demand was modest. Private consumption, about 60% of GDP, rose 0.1% q/q after an unrevised 0.4% increase in Q2.

CHINA DATA (MNI): China Fiscal Revenue Improves in October

MNI (Beijing) China’s national general public budget revenue reached CNY18.6 trillion during the first ten months of this year, up 0.8 percent year on year, an improvement from 0.5% rise during the first three quarters, the Ministry of Finance announced on Monday. National tax revenue hit CNY15.3 billion, up 1.7% y/y, an acceleration from the 0.7% from January to September, the data showed.

NEW ZEALAND DATA (MNI): Oct Services PMI Up But Still Sub 50, Pointing to Tepid Recovery

The Oct services PMI (via BNZ and Business NZ) edged up to 48.7 from 48.3 in Sep. We look to be on a steady improvement trend, but from depressed levels and the index hasn't been above the 50.0 expansion/contraction point since early 2024. The sub indices mostly ticked higher, but also remain under 50.0. Activity was 48.9, versus 48.0 prior, employment up to 48.8, versus 47.9 in Sep. The employment index eased back to 49.5 from 49.7 prior.

RATINGS: Greece Upgraded at Fitch, Belgium Downgraded at Scope

Sovereign rating reviews of note from after hours on Friday include:

- Fitch upgraded Greece to BBB; Outlook Stable

- Fitch affirmed Slovakia at A-; Outlook Stable

- Moody's affirmed Portugal at A3; Outlook Stable

- S&P affirmed Cyprus at A-; Outlook changed to Positive

- S&P upgraded South Africa to BB; Outlook Positive

- Morningstar DBRS confirmed the United Kingdom at AA, Stable Trend

- Scope Ratings downgraded Belgium to A+; Outlook Stable

FOREX: USDJPY Price Action Points Towards Renewed Test of 155.00

- The first session of the week provides some consolidation following Friday's volatility. The US dollar advanced against most others in G10 and SEK outperforms again, while the Euro and the likes of NZD and AUD weaken amid headline drivers remaining light.

- Amid reports on a fiscal easing package, price action in USDJPY points towards a renewed challenge to the 155.00 handle. The pair saw three highs around there recently ahead of Friday's temporary dip. Renewed upside would put sights on 155.53, a Fibonacci projection. Initial support to watch is 153.30, the 20-day EMA. Remember that Japanese authorities have recently stepped up their rhetoric on JPY valuations but stopped short of phrases historically associated with intervention for now.

- The extension of downward momentum in EURSEK is helping narrow the gap to an important support zone around 10.9000. A clear break of this level would expose 10.8000, which aligns closely with the April 4 low (10.7941). The case for continued SEK outperformance is largely tied to the growth differential channel. Recent domestic data have supported these arguments, with Swedish activity being supported by stimulative monetary policy, incoming fiscal stimulus and lower trade policy uncertainty.

- EURCHF closed last week at 0.9227, above a mid-term resistance zone after piercing 0.9200 for the first time since the withdrawal of the 1.20 floor in 2015. With today's price action lacking impetus following the weaker-than-expected Q3 Swiss flash GDP print, a few short-term signals suggest there may be scope for a bounce near-term for the cross.

- The trend is in oversold territory, and Friday's price pattern is a hammer candle - a potential short-term reversal signal. If the cross does recover, scope would be for a climb towards 0.9275, the 20-day EMA and 0.9298, the 50-day EMA. Key support lies at 0.9180, Friday's low and the bear trigger.

- Canada CPI, US empire manufacturing and construction spending highlight the data calendar for today alongside a set of Fed, ECB and BoE speakers.

EGBS: Bund Yields Hovering Around 2.70%; Global FI and Risk Cues to Set Tone

10-year Bund yields are down ~1.5bps today but remain just above the 2.70% figure for now. With this week’s Eurozone data calendar backloaded (flash PMIs and Q3 negotiated wages are due Friday), Bund yields will likely take cues from global FI peers and broader risk sentiment in the coming sessions. Nvidia’s earnings on Wednesday will be watched across global markets.

- Bund futures are +7 ticks at 128.73. A bear cycle remains in play, with RXZ5 having pierced support at 128.52 (76.4% retracement of the Sep 25 - Oct 17 bull leg) this morning. A clear break of this handle would signal scope for an extension towards 128.25, the Oct 7 low.

- BTPs outperform in the EGB space, with the 10-year spread to Bunds down 1.5bps to ~73.5bps. The OAT/Bund spread is marginally wider, with lingering political/fiscal risks holding French paper back versus peers.

- No material outperformance for GGBs on the back on Fitch's expected ratings upgrade on Friday (10-year GGB/Bund spread -1bps at ~61.5bps at typing).

- Italian final October HICP inflation confirmed flash estimates at 1.3% Y/Y.

- The European Commission’s Autumn forecasts saw 2026 inflation revised up to 1.9% (vs 1.7% prior), and GDP revised down to 1.2% (vs 1.4% prior).

- Canadian inflation headlines today’s North American data calendar, with any more details on US data releases following the Government reopening also in focus.

GILTS: Recovering But Yields Still Comfortably Higher Than Thursday

Gilts have rallied but yields are still 5-14bp above Thursday’s closing levels after Chancellor Reeves’ apparent u-turn when it comes to raising income taxes increased the fiscal risk premium in gilts.

- Weekend press reports were focused on smaller taxes and opinion pieces surrounding fiscal policy, nothing to really move the market.

- Futures +12 at 92.27.

- Initial support of note located at 91.82, while bulls ultimately need to close Friday’s opening gap lower (~93.35) to start turning the technical tide back in their favour.

- Yields 2.5-3.5bp lower, curve steepening.

- 2s10s trades less than 1bp from its October closing high (located at 74.26bp), while 5s30s is a little over 1bp off its October closing high (located at 140.12bp).

- Dovish adjustment in GBP STIRs given the move further out the curve. SONIA futures flat to +3.0. BoE-dated OIS little changed to 2bp more dovish on the day, showing 18bp of easing for December, 26.5bp through February and 34bp through March.

- BoE MPC member Mann will speak this afternoon (13:20 London). We have previously suggested that speeches from MPC members outside of Governor Bailey are likely to have less impact for markets in the run up to the December decision (given their entrenched views).

- CPI data (Wednesday) headlines this week’s UK calendar (see our gilt Week Ahead & morning STIR bullet for more on that release, our full preview will cross in due course).

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.788 | -18.2 |

Feb-26 | 3.704 | -26.6 |

Mar-26 | 3.628 | -34.2 |

Apr-26 | 3.537 | -43.3 |

Jun-26 | 3.499 | -47.1 |

Jul-26 | 3.457 | -51.3 |

Sep-26 | 3.445 | -52.5 |

EQUITIES: Eurostoxx Futures Trend Bullish Despite Latest Pullback

A medium-term bull trend in Eurostoxx 50 futures remains intact and last week’s gains reinforce bullish conditions. However, the latest pullback suggests the start of a corrective phase. Price has traded through the 20-day EMA. Attention is on support at the 50-day EMA, at 5604.85, and 5599.00, the base of a bull channel drawn from the Aug 1 low. These two price points represent key support. A break would highlight a stronger reversal. The trend condition in S&P E-Minis remains bullish and the latest selloff appears corrective - for now. Support at the 50-day EMA, at 6730.32, has been pierced, however, price is once again trading above the average. The next key support to watch is 6655.50, the Nov 7 low. Friday’s price pattern is a doji candle - a reversal signal. Initial firm resistance to watch is 6900.50, the Nov 12 high. A breach of this level would be bullish.

- Japan's NIKKEI closed lower by 52.62 pts or -0.1% at 50323.91 and the TOPIX ended 12.28 pts lower or -0.37% at 3347.53.

- Elsewhere, in China the SHANGHAI closed lower by 18.457 pts or -0.46% at 3972.035 and the HANG SENG ended 188.18 pts lower or -0.71% at 26384.28.

- Across Europe, Germany's DAX trades lower by 30.1 pts or -0.13% at 23846.65, FTSE 100 lower by 8.55 pts or -0.09% at 9689.9, CAC 40 down 7.69 pts or -0.09% at 8162.4 and Euro Stoxx 50 down 16.99 pts or -0.3% at 5676.78.

- Dow Jones mini up 63 pts or +0.13% at 47289, S&P 500 mini up 33 pts or +0.49% at 6787.75, NASDAQ mini up 192.5 pts or +0.77% at 25285.5.

Time: 10:00 GMT

COMMODITIES: Sell-Off in WTI on Nov 12 Strengthened a Bearish Theme

A sell-off in WTI futures on Nov 12 strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction. Gold is trading below last week’s high. The downleg between Oct 20 and 28, appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest that correction is over. Key support lies at the 50-day EMA, at $3927.5. Clearance of this EMA would signal scope for a deeper retracement. For bulls, a resumption of gains would pave the way for a test of $4381.5, the Oct 20 high and bull trigger.

- WTI Crude down $0.43 or -0.72% at $59.67

- Natural Gas down $0.08 or -1.71% at $4.49

- Gold spot down $0.54 or -0.01% at $4083.58

- Copper down $2.05 or -0.4% at $504.1

- Silver up $0.47 or +0.93% at $51.0467

- Platinum up $5.44 or +0.35% at $1550.71

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 17/11/2025 | 1315/0815 | ** | CMHC Housing Starts | |

| 17/11/2025 | 1320/1320 | BOE Mann on DMP and MonPol | ||

| 17/11/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/11/2025 | 1330/0830 | *** | CPI | |

| 17/11/2025 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/11/2025 | 1400/0900 | New York Fed's John Williams | ||

| 17/11/2025 | 1430/0930 | Fed Vice Chair Philip Jefferson | ||

| 17/11/2025 | 1445/1545 | ECB Lane Lecture on ECB MonPol | ||

| 17/11/2025 | 1500/1000 | * | Construction Spending | |

| 17/11/2025 | 1600/1700 | ECB Cipollone at ECON Digital Euro Hearing | ||

| 17/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/11/2025 | 1800/1300 | Minneapolis Fed's Neel Kashkari | ||

| 17/11/2025 | 2035/1535 | Fed Governor Christopher Waller | ||

| 18/11/2025 | 1000/1100 | ECB Elderson at Banking Supervision Press Conference | ||

| 18/11/2025 | 1300/1300 | BOE Pill Fireside Chat on MonPol | ||

| 18/11/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 18/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/11/2025 | 1415/0915 | *** | Industrial Production | |

| 18/11/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 18/11/2025 | 1500/1500 | BOE Dhingra on Income Growth and Consumption | ||

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1530/1030 | Fed Governor Michael Barr | ||

| 18/11/2025 | 1600/1100 | Richmond Fed's Tom Barkin | ||

| 18/11/2025 | 2100/1600 | ** | TICS | |

| 18/11/2025 | 2300/1800 | Dallas Fed's Lorie Logan | ||

| 19/11/2025 | 2350/0850 | * | Machinery orders |

Note: US Government data releases are still TBD pending an official release schedule.