MNI US OPEN - Trade Talks Back at the Top of the Agenda

EXECUTIVE SUMMARY

- RBA BOARD VOTES 6-3 TO LEAVE RATE AT 3.85%

- BESSENT AIMS TO MEET WITH CHINESE OFFICIAL IN NEXT FEW WEEKS

- SOUTH KOREA VOWS TO REVIEW RULES FOLLOWING TRUMP’S TARIFF LETTER

- TRUMP PROMISES MORE WEAPONS FOR UKRAINE AND CRITICIZES PUTIN

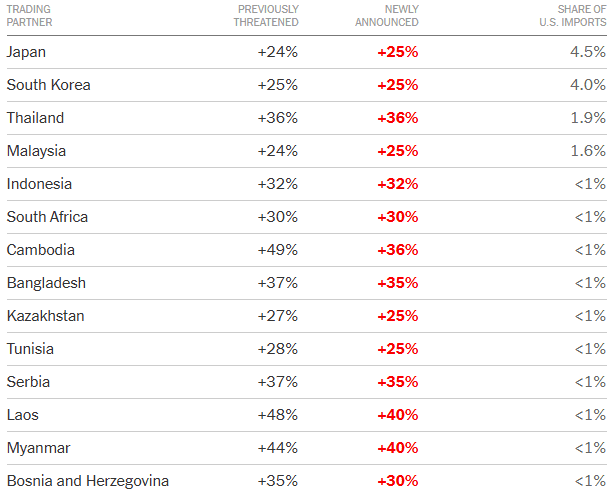

Figure 1: Tariff rates for select trade partners (includes country-specific “reciprocal” tariffs)

Source: New York Times

NEWS

RBA (MNI): RBA Board Votes 6-3 to Leave Rate at 3.85%

The Reserve Bank of Australia’s monetary policy board decided on Tuesday to leave the cash rate unchanged at 3.85%, citing the need for more data to confirm inflation is falling sustainably toward the 2.5% midpoint. The decision, which passed on a 6-3 vote, defied market expectations, which had fully priced in a 25 basis point cut. “The Board judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5% on a sustainable basis,” the board said in its statement. “It noted that monetary policy is well placed to respond decisively to international developments if they were to have material implications for activity and inflation in Australia.”

RBA (MNI): More Easing Likely to Come, Waiting on Q2 CPI Data - Bullock

RBA Governor Bullock's press conference is stressing that the direction of policy rates is still skewed lower. Today's decision reflected a need to wait for more data to cut rates further, particularly on inflation. The Governor stated that if Q2 inflation (which prints at the end of this month) comes in as the central bank forecast, it can ease further. This sets up for an August cut, although Bullock wouldn't be drawn on whether we could see a 50bps cut at that meeting.

US (RTRS): Trump Signs Executive Order Extending Tariff Deadline to August 1

U.S. President Donald Trump signed an executive order Monday extending the date on which so-called "reciprocal" tariffs will take effect to August 1. The previous deadline had been July 9.

US/CHINA (BBG): Bessent Aims to Meet With Chinese Official in Next Few Weeks

US Treasury Secretary Scott Bessent said that he expected to meet with his Chinese counterpart in the coming weeks to advance discussions on trade and other issues between the world’s two largest economies. “I’m going to be meeting with my Chinese counterpart at sometime in the next couple of weeks,” Bessent said in an interview Monday on CNBC. “We had good meetings in Geneva, in London. We both approached it with great respect”

US/S.KOREA (BBG): South Korea Vows to Review Rules Following Trump’s Tariff Letter

South Korea said it will review regulations flagged by the US while pressing for an easing of sectoral tariffs after President Donald Trump sent a letter with a new August deadline for imposing 25% across-the-board levies. The South Korean government didn’t elaborate on what rules and regulations would be looked at, but its trade officials have said restrictions affecting big US tech companies in the digital sector have emerged as a major topic in talks.

US/S.AFRICA (BBG): South Africa’s Ramaphosa Sees Scope to Lower US Tariff in Talks

South African President Cyril Ramaphosa said there’s the prospect that the US may lower a planned 30% tariff on goods in ongoing talks with Washington, as he challenged its calculation of the new levy. US President Donald Trump on Monday unveiled a wave of promised letters that threaten to impose higher duties on American trading partners while signaling that he’s open to discussions on the increased tariffs until at least Aug. 1. The announcement came hours after the US leader threatened to impose an additional 10% levy on all countries that form part of the BRICS economic bloc.

US/UKRAINE (BBG): Trump Promises More Weapons for Ukraine and Criticizes Putin

President Donald Trump said he’d ship more weapons to Ukraine, marking an apparent reversal after the Pentagon halted flows of some air-defense missiles and artillery shells to the country. “We’re going to send some more weapons,” Trump told reporters at the start of a dinner with Prime Minister Benjamin Netanyahu at the White House on Monday evening. “We have to. They have to be able to defend themselves. They’re getting hit very hard now.”

US/ISRAEL (NYT): Trump and Netanyahu Meet Amid Gaza Cease-Fire Negotiations

President Trump and Prime Minister Benjamin Netanyahu confronted several high-stakes issues when they met for dinner on Monday night, including the long-term future of Gaza and the prospect of Israel normalizing relations with its Persian Gulf neighbors. But first, they indulged in some self-congratulation. The two celebrated the U.S. airstrikes on Iran’s nuclear facilities, and Mr. Netanyahu used the occasion to further ingratiate himself to the American president by telling Mr. Trump he had nominated him for a Nobel Peace Prize.

US (BBG): Rubio Heads to Malaysia for Summit Under Shadow of Tariffs

Marco Rubio is making his first trip to Asia as the top US diplomat, heading to a summit in Malaysia a day after President Donald Trump again threatened to slam the region with high tariffs. The secretary of state flies to Kuala Lumpur, Malaysia, on Tuesday for a gathering of the Association of Southeast Asian Nations. While he’d prefer to keep the focus on security issues and competition with China, the trip will take place under the shadow of Trump’s latest tariff gambit.

UK/FRANCE (The Times): Keir Starmer to push Macron for last-minute migrant return deal

Sir Keir Starmer will urge President Macron to agree a “one in, one out” migrant returns deal on Tuesday, despite warnings that announcing it before it is ready will lead to a surge in crossings. The prime minister is pressing for the deal as the centrepiece of a new agreement between Britain and France that the two leaders will sign at an Anglo-French summit on Thursday. The arrangement would allow Britain to return small boat migrants to France in exchange for accepting asylum seekers with a family connection in the UK.

UK (MNI): Not a Lot New on Productivity in the OBR FRS Report

The assumption that debt could rise to "above 270% of GDP by the early 2070s" is a broad reaffirmation of 274% number from the September report baseline. "A low-productivity variant of our 2024 FRS long-term fiscal projections based on productivity growth of 0.5 per cent (1.0 percentage points below our central scenario) would increase net debt relative to our central projection by over 350 per cent of GDP by 2073-74, reaching 647 per cent of GDP."

MIDEAST (MNI): Houthis Ramp Up Attacks on Red Sea Shipping Amid Gaza Ceasefire Efforts

After a period of relative quiet, the Houthi rebels in Yemen have renewed their attacks on shipping in and around the Red Sea with a vengeance, claiming to have sunk the Liberian-flagged bulk carrier, the Magic Seas, over the weekend. Then on the night of 7 July, a ship in the Red Sea west of the Yemeni port of Hodeidah was struck by attacks from five rocket grenades, disabling its propulsion. A further UKMTO update this morning confirmed that the vessel is "surrounded by small craft and under continuous attack".

MNI RBNZ PREVIEW - JULY 2025: Likely on Hold

The sell-side consensus is for the RBNZ to remain on hold tomorrow, which is also consistent with market pricing. There are some sell-side forecasters looking for a rate cut tomorrow, whilst most of those who see the RBNZ on hold, see risks of further cuts as we progress through 2025. For this meeting, our own bias is for the central bank to hold policy rates steady. Recent inflation outcomes arguably provide the strongest signal that the RBNZ should hold pat at tomorrow’s policy meeting outcome.

AUSTRALIA/CHINA (MNI): Albanese to Visit China 12-18 July

MNI (London) Australian PM Anthony Albanese will visit China from 12-18 July. Earlier, the PM's office released a statement confirming Albanese would "hold the Australia-China Annual Leaders' Meeting with Premier Li in Beijing. The Prime Minister will also meet President Xi Jinping and Chairman Zhao Leji of the National People's Congress." During the visit, Albanese and Chinese leaders will attend the Australia-China CEO Roundtable, while Albanese will also visit Shanghai and Chengdu.

DATA

AUSTRALIA DATA (MNI): NAB Business Conditions Up Firmly in June, Wages Remain Benign

The Australia NAB survey of business conditions for June showed notable improvement. We rose to +9 from flat in May. This is the highest print since March last year. Business confidence also rose, up to +5, from +2 in May. In terms of the underlying conditions in the survey, trading rose to +15, from +5. Profitability improved to +4, from -5, while employment was +3, from +1 prior. Forward orders were flat, versus -2 in May. Capex rose to +10 from +6 prior. Exports and exporter sale conditions remained negative though.

FOREX: Tariff Letter Frenzy Caps USD/JPY Rally

- Trump's tariff letter-writing caught markets yesterday, prompting losses for equities and a negative close on Wall Street. Equity futures are yet to reverse, but are off the worst levels of the week headed into the crossover. The tariff headlines yesterday put paid to the USD/JPY rally that seems to have run out of steam into NY hours. That said, price remains in close proximity to 146.45, the weekly high and level above which the corrective move higher could resume. Through here, markets eye 148.03 for direction ahead of the Y149.73 200-dma.

- Triggers for a return higher in USD/JPY would be a re-widening of front-end US-Japan yield spreads or a corrective rally for the USD Index - which appears to be building a base at the recent pullback low of 96.377. While tariff uncertainties remain present, another likely delay to the installation of reciprocal tariffs to early August is keeping the USD downside argument intact, despite further warning signs over the pace of USD weakness this year - most recently via a PBOC survey issued to domestic banks earlier in the week.

- JPY is the poorest performer on the day, while AUD is the strongest. The RBA rate decision pushed back against building consensus for another rate cut by holding policy. AUD/USD trades back above 0.6500 as a result, and keeps the 50-dma support intact on any further downside.

- Following the data rush last week, there are no tier 1 releases due from the US Tuesday, although the NY Fed's latest survey on one-year inflation expectations could see some attention, expected to slow to 3.13% from 3.20%. The speaker schedule is similarly light, with just ECB's Nagel at 1500BST/1000ET.

EGBS: Under Pressure Amid Heavy Supply and Tariff Negotiation Extension

Bund futures have come under notable pressure this morning, a combination of regional issuance pressures, tariff deadline extensions and broader price action in the core FI space. Bunds are down 57 ticks at 129.49 at typing, having pushed through the July 2 low and bear trigger at 129.77. Initial support is 129.43 (equating to the May 14 high in the 10-year yield), with the May 22 futures low at 129.30 the next downside target.

- Futures volumes have been above average through the morning, even after taking into account hedging needs for this morning’s E6bln 2.20% Oct-30 Bobl launch.

- The auction saw another fairly subdued cover ratio (similar to last week’s 10-year Bund launch). Benchmark Bobl yields remain up 10bps on the session at 2.26%.

- Today has also seen supply from the Netherlands and Austria, while the EU is holding a dual tranche syndication.

- Overnight, US President Trump sent “tariff letters” to a number of trading partners. The EU did not receive a letter, and reports suggest officials are hopeful that tariffs won’t rise beyond the current 10% level. The negotiating deadline was pushed back to August 1, from July 9 prior.

- The selloff in EGBs has been quite uniform across countries, with 10-year spreads to Bunds within 1bp of yesterday’s closing levels.

- The remainder of today's regional calendar is light. German and French May foreign trade data were released this morning.

GILTS: Bear Steepening Extends

Weakness in wider core global FI markets has pushed gilt futures through lows from last Wednesday & Thursday, leaving bears focused on nearby Fibonacci support (91.50), followed by the Feb 2 low (91.16).

- A relatively heavy session for global sovereign supply, the EU escaping higher U.S. tariffs (at least for now), a delay of the broader U.S. tariff deadline, further steepening on the JGB curve and a hawkish RBA outcome have all factored into this morning’s weakness.

- Yields 3-7bp higher, curve steeper.

- 10-Year yields registered a fresh July high (4.640%), with focus now on the June 9 high (4.673%).

- 2s10s though the month-to-date closing high, last 74.5bp, ~10bp off April’s intraday year-to-date high.

- 5s30s set for a fresh year-to-date closing high, last 14.06bp. Focus on the April intraday high at 147.2bp.

- There was no immediate reaction to the OBR’s Fiscal Risks and Sustainability Report, although the details won’t do much to alleviate long-term worry surrounding the UK’s fragile fiscal state and well-documented productivity headwinds.

- This morning’s GBP900mln sale of the 1.875% Sep-49 I/L gilt passed smoothly.

- BoE-dated OIS shows 52bp of cuts through year-end after failing to push meaningfully beyond 55bp in recent weeks. Over 80% odds of a 25bp cut are still priced through the August MPC, with such a step still fully discounted come the end of the September MPC.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.003 | -21.4 |

Sep-25 | 3.948 | -26.9 |

Nov-25 | 3.781 | -43.7 |

Dec-25 | 3.696 | -52.2 |

Feb-26 | 3.566 | -65.1 |

Mar-26 | 3.535 | -68.2 |

EQUITIES: Eurostoxx 50 Futures Remain Close to Cycle Highs

Recent gains in Eurostoxx 50 futures from the Jun 23 low, still appears to be a potential reversal and the contract is holding on to its most recent gains. Price has pierced both the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme. This would open 5486.00, May 20 high and bull trigger. On the downside, a break of 5194.00, Jun 23 low, reinstates a bearish theme. The trend condition in S&P E-Minis is unchanged, the outlook remains bullish. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This has been followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6011.49.

- Japan's NIKKEI closed higher by 101.13 pts or +0.26% at 39688.81 and the TOPIX ended 4.82 pts higher or +0.17% at 2816.54.

- Elsewhere, in China the SHANGHAI closed higher by 24.348 pts or +0.7% at 3497.475 and the HANG SENG ended 260.24 pts higher or +1.09% at 24148.07.

- Across Europe, Germany's DAX trades higher by 18.14 pts or +0.08% at 24091.32, FTSE 100 higher by 7.3 pts or +0.08% at 8814.06, CAC 40 down 16.78 pts or -0.22% at 7706.69 and Euro Stoxx 50 down 4.98 pts or -0.09% at 5336.56.

- Dow Jones mini down 51 pts or -0.11% at 44626, S&P 500 mini up 5.75 pts or +0.09% at 6281.75, NASDAQ mini up 57.75 pts or +0.25% at 22942.5.

Time: 10:00 BST

COMMODITIES: WTI Futures Maintain Softer Tone, But Above 50-Day EMA Support

WTI futures maintain a softer tone following the reversal from the Jun 23 high, and recent gains appear corrective. Support to watch is the 50-day EMA, at $64.96. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high. A recent move lower in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5, May 29 low. Note that the latest recovery highlights a possible false trendline break. A resumption of gains would refocus attention on $3451.3, the Jun 16 high. The bear trigger lies at $3248.7, the Jun 30 low.

- WTI Crude down $0.49 or -0.72% at $67.46

- Natural Gas down $0.03 or -0.88% at $3.382

- Gold spot down $12.07 or -0.36% at $3324.58

- Copper up $1.2 or +0.24% at $503.85

- Silver down $0.01 or -0.03% at $36.761

- Platinum down $2.84 or -0.21% at $1372.65

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 08/07/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 08/07/2025 | - | ECB de Guindos At ECOFIN Meeting | ||

| 08/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 08/07/2025 | 1400/1000 | * | Ivey PMI | |

| 08/07/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 08/07/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/07/2025 | 1900/1500 | * | Consumer Credit | |

| 09/07/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 09/07/2025 | 0130/0930 | *** | CPI | |

| 09/07/2025 | 0130/0930 | *** | Producer Price Index | |

| 09/07/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 09/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/07/2025 | 0930/1030 | BOE Financial Stability Report | ||

| 09/07/2025 | 1000/1100 | BOE FSR Press Conference | ||

| 09/07/2025 | 1045/1245 | ECB Lane At House of the Euro | ||

| 09/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/07/2025 | 1100/1300 | EC De Guindos Closing Remarks At Conference | ||

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/07/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/07/2025 | 1800/1400 | *** | FOMC Minutes |