MNI US OPEN - Tariffs, Mideast on Agenda as G7 Leaders Meet

EXECUTIVE SUMMARY

- TRUMP SAYS ISRAEL, IRAN MAY NEED TO ‘FIGHT IT OUT’ BEFORE DEAL

- TARIFFS, ISRAEL AND TRUMP LIKELY TOPICS AS ANTSY G-7 LEADERS MEET IN CANADA

- ECB’S NAGEL SAYS HIGH UNCERTAINTY LEAVES NO ROOM FOR EASING

- JAPAN’S KATO SAYS TALKS WITH MARKETS KEY FOR BOND ISSUANCE

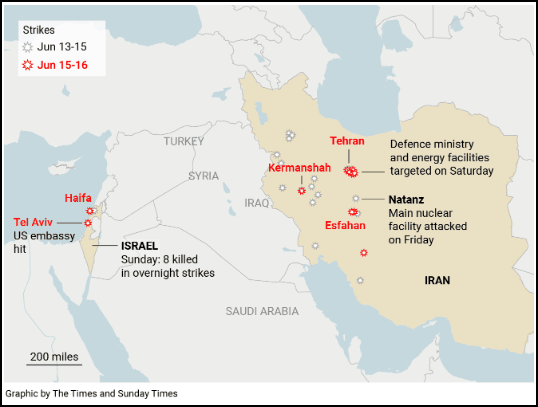

Figure 1: Tehran reportedly uses hypersonic missiles in latest strikes on Israel

NEWS

US/MIDEAST (BBG): Trump Says Israel, Iran May Need to ‘Fight It Out’ Before Deal

President Donald Trump said he believed it’s possible Israel and Iran could reach an agreement to end their conflict, though the two sides may need to continue fighting before they’re ready to broker a peace deal. “Sometimes they have to fight it out, but we’re going to see what happens,” Trump told reporters at the White House on Sunday as he departed for the Group of Seven leaders’ summit in Canada. “I think there’s a good chance there’ll be a deal,” the president added.

MIDEAST (MNI): Tasnim-Tehran Uses Hypersonic Missiles in Latest Strikes on Israel

Semi-official Iranian outlet Tasnim reports that the Islamic Revolutionary Guards Corps (IRGC) Aerospace Force is using hypersonic missiles in its attacks on Israel. Tasnim claims that "In this morning's operation, several images were recorded of hypersonic missiles hitting targets in Tel Aviv and Haifa, showing that these missiles easily passed through Israel's anti-ballistic defense systems and hit the target. [These missiles] are equipped with a solid-fuel spherical engine warhead with a movable nozzle and the ability to maneuver and change course." Previously, the Israeli military has denied that Iran possesses hypersonic missiles or manoeuvrable warheads.

G7 (WaPo): Tariffs, Israel And Trump Likely Topics as Antsy G-7 Leaders Meet in Canada

Leaders of the world's major economies will gather here Monday hoping to persuade a mercurial U.S. president to preserve long-standing alliances and calm a jittery global landscape but, in some cases, are willing to go their own way if they do not succeed. President Donald Trump will attend this year's Group of Seven summit in the foothills of the Canadian Rockies amid deep anxiety among the United States' traditional economic allies. These nations hope to persuade him to continue scaling back the punishing tariffs he has imposed across the world, but they also aim to avoid the kind of confrontation that some world leaders have set off while meeting with Trump in his first and second terms.

US (NYT): ‘Golden Share’ in U.S. Steel Gives Trump Extraordinary Control

To save its takeover of U.S. Steel, Japan’s Nippon Steel agreed to an unusual arrangement, granting the White House a “golden share” that gives the government an extraordinary amount of influence over a U.S. company. New details of the agreement show that the structure would give President Trump and his successors a permanent stake in U.S. Steel, significant sway over its board and veto power over a wide array of company actions, an arrangement that could change the nature of foreign investment in the United States.

ECB (MNI): High Uncertainty Leaves No Room for Easing - Nagel

There is currently no for the European Central Bank to further relax its monetary policy stance, Bundesbank president Joachim Nagel said in a speech on Monday. But policymakers must remain alert, despite having accompanied their mission of getting inflation back to 2%. “Even though inflation in the eurozone is back at around 2% and is likely to remain there in the medium term after a dip, there is no reason for monetary policy to ease,” Nagel said.

ECB (MNI): Risk of Undershooting Very Limited - Guindos

The fact that inflationwill be around 1.4% in Q1 2026 is not going to be enough to unanchor inflation expectations and modify the wage bargaining process, ECB Vice-President Luis de Guindos said in an interview with Reuters published Monday, adding that in his view the risk of inflation undershooting the 2% target is “very limited.” “We clearly see that wage dynamics are cooling. But, even when you take all these factors into consideration, compensation per employee will be around 3% over time,” he noted.

UK (FT): Rachel Reeves to Set Out 10-Year UK Infrastructure Plan

Rachel Reeves will this week announce what she claims will be a £725bn ten-year infrastructure plan for Britain, starting with a new programme to repair crumbling bridges, flyovers and tunnels. Allies of the chancellor say she will commit to increasing the infrastructure budget to at least £725bn over the next decade, pre-committing part of the capital budget ahead of the next spending review in 2027. A priority for Reeves will be to accelerate projects that bring quick results, as she attempts to leverage an increase in capital spending into political dividends ahead of the next election, which must be held by summer 2029.

SWITZERLAND (MNI): Government Downwardly Revises Growth Forecasts

"The Federal Government Expert Group on Business Cycles has revised down its forecast for Swiss economic growth. GDP adjusted for sporting events is expected to grow by 1.3% in 2025, followed by 1.2% in 2026 (March forecasts: 1.4% and 1.6% respectively). This would mean the Swiss economy growing at a significantly below-average rate in both years. The forecast assumes no further escalation of the international trade conflict." Despite the downward revision, the forecasts would represent reasonable

growth momentum for the Swiss economy, and would thus not warrant an outsized 50bp SNB cut into negative territory at Thursday's meeting.

MNI BOJ PREVIEW - JUNE 2025: Focus on Future Rate Hikes & QT

The Bank of Japan (BoJ) is set to hold its Monetary Policy Meeting (MPM) on June 16–17, and although no changes are expected to the current policy rate of 0.50%, the meeting may still prove impactful for both domestic and global markets. The key area of interest will be Governor Kazuo Ueda’s post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes. If the BoJ begins to hint at stronger underlying inflationary trends or shows greater optimism about the economy, it could stoke expectations of a rate hike in the autumn.

JAPAN (BBG): Japan’s Kato Says Talks With Markets Key for Bond Issuance

Japan’s finance minister said discussions with market participants are a key factor for ensuring government bonds are bought and sold stably ahead of a closely watched ministry meeting with investors. “We are engaged in thoughtful and careful dialogue with the market, and it is incumbent upon us to make sure that government bonds are being bought,” Finance Minister Katsunobu Kato said in an interview with Bloomberg TV on Friday. As the Bank of Japan steps back from bond purchases, the government needs to find other investors to fill the gap, he said.

JAPAN (BBG): Polls Show Support for Japan’s Ishiba Recovering Before Election

Public support for Japan’s prime minister is holding up after the government moved to address high rice prices, according to new opinion polls, a positive sign for Shigeru Ishiba as he heads into an election and tries to reach a trade agreement with the US. A survey conducted over the weekend by Kyodo News showed the approval rating for Ishiba’s cabinet at 37.0%, up from 31.7% in a survey in May. A separate poll by the Asahi newspaper showed support at 32%, little changed from 33% in a May survey.

CHINA (MNI): China to Continue Active Macro Policies

MNI (Beijing) Beijing will continue implementing active macro policies to enhance economic momentum, according to Fu Linghui, spokesperson for the National Bureau of Statistics on Monday. "China's policy tool box has sufficient reserves," Fu said, adding the economy had showed resiliance despite external uncertainty. Speaking to reporters, Fu noted falling commodity prices had driven the 3.8% year-on-year drop in import performance so far this year. Fu added that China's import performance was adversely impacted by some countries increasing restrictive trade measure. However, the import of industrial goods had expanded 6% year-on-year between January and May, Fu said.

CHINA (BBG): Xi Takes Push for Global Sway to Central Asia With Kazakh Visit

Chinese President Xi Jinping has arrived in Kazakhstan for talks with Central Asian leaders, providing a counterpoint to a Group of Seven summit by visiting a vast region at the nexus of competing interests from Washington to Beijing. Xi, who’s making only his third overseas trip this year, will meet with Kazakh President Kassym-Jomart Tokayev on Monday and attend the second gathering of the leaders of Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan the following day.

BOK (BBG): BOK Calls for Close Monitoring of Yuan as Anchor for Won Moves

South Korea should closely monitor the yuan as China’s currency may influence the won during periods of global uncertainty spurred by the trade war, the Bank of Korea said in a study Monday. The Chinese and Korean currencies already have a strong correlation, averaging around 0.6 since 2018, according to the study. The BOK said the linkage was tighter during certain periods, such as between 2018 and 2019 when there was heightened US-China trade friction, the Federal Reserve’s rate hikes from February 2022 to April 2023, and US President Donald Trump’s re-election last year.

DATA

EUROZONE DATA (MNI): Q1 Labour Cost Index Moderates, But Less Than First Indicated

The Eurozone hourly labour cost index (LCI) moderated to 3.4% Y/Y in Q1 2025, the lowest since Q3 2022 (Q4 2024 was 3.8%) although stronger than the 3.2% Eurostat indicated in "early estimates" released 20 May 2025. Costs of hourly wages & salaries and the non-wage costs increased by 3.4% each. The data confirms more forward-looking wage indicators such as the ECB wage tracker, which also moderated recently and which the Governing Council appears to be more focused on due to its forward-looking nature. The LCI is calculated as the ratio of total labour costs (wages and salaries plus non-wage costs) and hours worked.

UK DATA (FT): UK Property Asking Prices Post Unusual Fall in June

Asking prices for UK homes fell in June, bucking the trend for rises at this time of year, according to data that showed the biggest declines in London and the south of England where more properties were put up for sale. Average new seller asking prices dropped 0.3 per cent to £378,240 between May and June, Rightmove said on Monday, after a 0.6 per cent increase between April and May. Prices have risen by an average of 0.4 per cent in June for the past 10 years, according to the property portal.

ITALY DATA (MNI): Downward Revision to Italy May HICP Driven by Food Component

Italian May headline HICP was revised down two tenths on a rounded basis to 1.7% (vs 1.9% flash, 2.0% prior), driven by the food component. Excluding food, energy, alcohol and tobacco ("core"), HICP inflation was unchanged from the flash at a rounded 1.9% (vs 2.2% prior). On an unrounded basis, headline HICP was 1.71% Y/Y (vs 2.04% prior) while core inflation was 1.90% Y/Y (vs 2.17% prior).

NORWAY DATA (MNI): Lower Crude Prices Weighs on May Trade Surplus, Import Demand Steady

The Norwegian trade surplus narrowed to NOK46.1bln in May, down from NOK54.6bln in April and NOK53.2bln a year ago. Total exports fell to NOK138.2bln (vs NOK146.1bln in April, NOK149.2bln in May '24). Statistics Norway highlights lower oil prices as the main driver of this decline, but crude oil exports measured in barrels were also down 7% Y/Y. Norges Bank monetary policy is mostly ineffective at responding to swings in the goods trade balance, which is heavily dictated by global demand and broader uncertainty. However, the relatively stable development of goods imports (NOK92.1bln vs NOK91.5bln prior) is consistent with domestic data indicating a relatively resilient mainland demand backdrop.

CHINA DATA (MNI): China's May Consumption Hits Over One-Year High

- CHINA MAY RETAIL SALES +6.4% Y/Y VS MEDIAN +4.9% Y/Y

- CHINA JAN-MAY INDUSTRIAL OUTPUT +6.3% Y/Y VS JAN-APR +6.4% Y/Y

- CHINA MAY UNEMPLOYMENT RATE +5.0% VS APR +5.1%

- CHINA YTD PROPERTY INVESTMENT -10.7% Y/Y VS MEDIAN -10.5% Y/Y

- CHINA YTD FIXED-ASSET INVESTMENT +3.7% Y/Y VS MEDIAN +4.0% Y/Y

China's retail sales, a gauge of consumption, quickened to 6.4% y/y in May from April's 5.1% growth, hitting the highest level since December 2023, beating the 4.9% forecast, according to data released Monday by the National Bureau of Statistics. Industrial production increased 5.8% y/y in May to record a six-month low, down from April's 6.1% growth, and missing the expected 6.0%. Fixed-asset investment decelerated for the third month to 3.7% y/y in the first five months from the previous 4.0% result, underperforming expectations of 4.0%.

RATINGS: Belgium Downgraded at Fitch, Affirmations Elsewhere

Sovereign rating reviews of note from after hours on Friday included:

- Fitch downgraded Belgium to A+; Outlook Stable

- Fitch affirmed Norway at AAA; Outlook Stable

- S&P affirmed Germany at AAA; Outlook Stable

- S&P affirmed Sweden at AAA; Outlook Stable

- Scope Ratings affirmed Poland at A, Outlook Stable

EGBS: Bunds Off Session Lows With Oil Down 1%; Key Support Untested

Bund futures have recovered from earlier session lows of 130.17, now -29 ticks at 130.49. Brent crude futures are down ~1% today, easing near-term concerns around the inflationary impact of an extended conflict between Israel and Iran. The pullback in Bunds from Thursday’s high is considered corrective for now, with key support at 130.12 (June 5 low).

- The German curve has steepened, with 30-year yields up 3bps and Schatz yields up 1bp.

- The 10-year OLO/Bund spread has seen a fairly contained impact from Fitch's rating downgrade on Friday, currently 0.5bps wider at 57bps. While still slightly underperforming EGB peers on the session, a downgrade did not come as a large surprise given Fitch had held Belgium on a negative outlook since March 2023.

- The 10-year BTP/Bund spread has unwound 1.5bps of Friday's 2bp widening, now back to 93.5bps with equity sentiment supported this morning despite continued Middle East tensions.

- Comments from ECB’s de Guindos and Nagel had limited impact on front-end EUR rates.

- Italian May headline HICP saw a downward revision to 1.7% (vs 1.9% flash) due to the food component, while Eurozone Q1 labour costs were revised up to 3.4% Y/Y (vs 3.2% flash).

- The remainder of today’s calendar is light, leaving focus on geopolitical headline flow.

GILTS: Off Lows, Curve Twist Steepens

Gilts recover from session lows with oil moving further away from Asia-Pac highs (albeit holding comfortably above late Thursday levels) and with the recovery from overnight lows in the major global equity index futures stalling a little.

- More widely, attention remains on the Israel-Iran situation, with rhetoric not signalling de-escalation in the immediate term.

- Gilt futures trade as low as 92.23, breaking Friday’s low, before a recovery to 92.50, -15 on the day.

- The recent uptrend had taken the contract into overbought territory.

- Bears now target the 20-day EMA (92.04), which provides the first firm support level.

- Yields 1.5bp lower to 1.5bp higher, curve twist steepens.

- 2s10s in multi-week range, ~63.5bp last.

- 5s30s back above 120bp after Friday’s close below.

- Domestically, focus is on Wednesday’s CPI data (we have already flagged downside risks to that release) and Thursday’s BoE decision (softer economic growth and labour market data shouldn’t result in a cut at this stage, which will leave focus on the vote split).

- BoE-dated OIS back to pricing ~47bp of BoE cuts through year-end, little changed on the day after briefly showing ~45bp post-gilt open. 0.5bp priced for this week, 19bp through August, 24.5bp through September, 40bp through November.

- SONIA futures +1.5 to -1.5, strip twist steepens.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.208 | -0.5 |

Aug-25 | 4.021 | -19.0 |

Sep-25 | 3.965 | -24.6 |

Nov-25 | 3.812 | -39.9 |

Dec-25 | 3.740 | -47.1 |

Feb-26 | 3.629 | -58.2 |

Mar-26 | 3.602 | -60.9 |

EQUITIES: E-Mini S&P Back Above 20-Day EMA, Pullback Considered Corrective

The latest pullback in the Eurostoxx 50 futures contract has resulted in a breach of the 50-day EMA at 5297.58. Price has also pierced 5255.00, the May 23 low. A clear break of both support points would highlight a short-term top and signal scope for a deeper retracement. This would open 5178.00, the May 6 low and 5081.16, a Fibonacci retracement. Initial resistance to watch is 5365.98, the 20-day EMA. The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high last Wednesday, reinforcing current bullish conditions. For now, the most recent pullback is considered corrective. The contract has pierced support at 5990.75, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5882.88. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

- Japan's NIKKEI closed higher by 477.08 pts or +1.26% at 38311.33 and the TOPIX ended 20.66 pts higher or +0.75% at 2777.13.

- Elsewhere, in China the SHANGHAI closed higher by 11.733 pts or +0.35% at 3388.729 and the HANG SENG ended 168.43 pts higher or +0.7% at 24060.99.

- Across Europe, Germany's DAX trades higher by 83.31 pts or +0.35% at 23599.84, FTSE 100 higher by 28.18 pts or +0.32% at 8878.8, CAC 40 up 51.83 pts or +0.67% at 7736.8 and Euro Stoxx 50 up 24.5 pts or +0.46% at 5315.14.

- Dow Jones mini up 197 pts or +0.47% at 42408, S&P 500 mini up 33.75 pts or +0.56% at 6013, NASDAQ mini up 141 pts or +0.65% at 21785.25.

Time: 09:55 BST

COMMODITIES: Continuation Higher for WTI Futures Would Expose $80 Handle

WTI futures traded sharply higher last week and Friday’s early rally marked an acceleration of the current bull phase. Price action is likely to remain volatile and from a technical standpoint, the trend is currently in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted $68.49, the Jun 13 low. A breach of this level would signal scope for a deeper retracement. A bullish theme in Gold remains intact and this week’s gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3262.2, the 50-day EMA.

- WTI Crude down $0.22 or -0.3% at $72.92

- Natural Gas up $0.11 or +2.99% at $3.687

- Gold spot down $16.91 or -0.49% at $3415.42

- Copper up $1.45 or +0.3% at $488.45

- Silver up $0.12 or +0.32% at $36.4139

- Platinum up $17.77 or +1.45% at $1245.79

Time: 09:55 BST

| Date | GMT/Local | Impact | Country | Event |

| 16/06/2025 | 1030/1230 | ECB Cipollone At Osservatorio Banca Impresa 2030 Meeting | ||

| 16/06/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/06/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 16/06/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/06/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 16/06/2025 | - | FOMC Meetings with S.E.P. | ||

| 17/06/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 17/06/2025 | 0600/0800 | ** | Unemployment | |

| 17/06/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 17/06/2025 | 1315/0915 | *** | Industrial Production | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note |