MNI US OPEN - Netenyahu, Trump Meet as US Pushes Gaza Truce

EXECUTIVE SUMMARY

- NETANYAHU TO MEET TRUMP AS US INTENSIFIES GAZA TRUCE PUSH

- REEVES STILL DOESN’T RULE OUT VAT RISE; WORDING STRONGER THAN WEEKEND

- BOJ’S NOGUCHI SEES FLEXIBLE POLICY; UNDERLYING CPI FOCUS

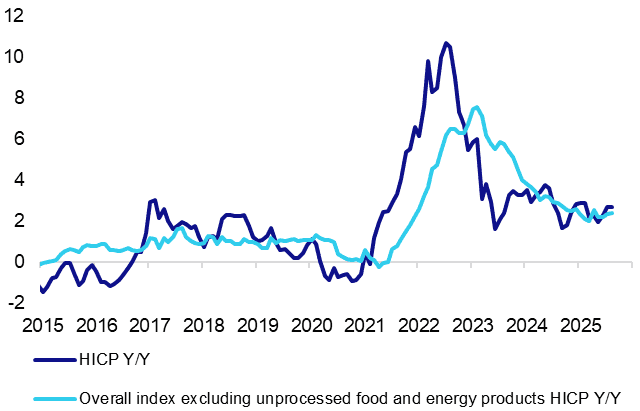

- SPANISH HICP INLINE, ENERGY UPWARD DRIVER AS EXPECTED

Figure 1: Spanish flash September HICP inline with consensus on a rounded basis at 3.0% Y/Y

Source: MNI, INE

NEWS

US/ISRAEL (BBG): Netanyahu to Meet Trump as US Intensifies Gaza Truce Push

Israeli Prime Minister Benjamin Netanyahu is set to hold a crucial White House meeting with US President Donald Trump on Monday amid assertions from Washington that an ambitious plan to end the war in Gaza is nearly complete. The meeting — the fourth between the two allies since Trump took office in January — comes after the US leader shared a 21-point proposal aimed at concluding the Israel-Hamas conflict with other regional heads in New York last week.

US (FT): Wall Street Regulator Vows Light Touch and End to Quarterly Reporting

Wall Street’s top watchdog has pledged to pursue a minimum “dose” of regulation and fast-track President Donald Trump’s proposal to scrap quarterly corporate reporting, underlining an abrupt loosening of financial regulations by the Securities and Exchange Commission. SEC chair Paul Atkins, appointed by Trump in the spring, said in an opinion article for the Financial Times on Monday that he would look at the option of semi-annual corporate reporting in place of the current requirement that listed companies report results every three months.

US (MNI): Trump to Meet Congressional Leaders in Last-Ditch Bid to Avert Govt Shutdown

15:00 ET 20:00 BST, President Donald Trump will meet Senate Majority Leader John Thune (R-SD), House Speaker Mike Johnson (R-LA), Senate Minority Leader Chuck Schumer (D-NY), and House Minority Leader Hakeem Jeffries (D-NY) at the White House in a last-ditch attempt to avert a government shutdown at 00:01 ET 05:01 BST on Oct. 1. While the meeting keeps the possibility of a deal open, neither Schumer nor Thune has indicated flexibility. Moreover, it is unclear if Trump intends to propose a deal or press Democrats to accept the GOP funding package. Schumer told NBC if Trump is going to "just yell at Democrats... We won't get anything done."

ECB (BBG): ECB Is ‘Near the Bottom’ of Rate-Cutting Cycle, Makhlouf Says

European Central Bank Governing Council member Gabriel Makhlouf said the cycle of interest-rate reductions is near its end. “Relatively speaking, we are near the bottom,” the Irish official told the Financial Times. But “we’re not on a pre-determined path,” he said. “I am pleased with where we are, but we need to pay pretty close attention to what’s going on.” Satisfied that inflation will remain close enough to its 2% target, the ECB left borrowing costs unchanged for a second straight meeting this month.

UK (MNI): Reeves Still Doesn’t Rule Out VAT Rise; Wording Stronger Than Weekend

Reeves does sound a little more committed to not raising VAT than the comments over the weekend in her interview on Sky News this morning. She has explicitly noted that a rise in VAT would hit working people - and again made the commitment to improve living standards for working people. It's still not a promise not to increase VAT but seems stronger wording than over the weekend. However, caveat all of this with the Treasury having not yet received the first draft of OBR forecasts - they don't come until Friday. So if those are worse than the c. GBP30bln gap than media sources have stated that the Treasury is expecting, the VAT question could come up again.

SNB (MNI): SNB Lowers Minimum Reserve Requirement Thresholds

The Swiss National Bank said on Monday it is lowering the threshold factor for the remuneration of sight deposits of account holders subject to minimum reserve requirements from 18 to 16.5, effective as of Nov 1. Sight deposits up to the threshold are remunerated at the SNB policy rate, while sight deposits above the threshold are remunerated at the SNB policy rate minus a discount. Sight deposits which are held to meet minimum reserve requirements are not remunerated.

RIKSBANK (MNI): Seim Is Confident in Household Consumption Impulse

In the Riksbank September minutes, Seim appears confident that the proposed food VAT tax cut, alongside other policies such as the easing of mortgage-based macro-prudential measures, will stimulate household consumption going forward. This is the main rationale for her dissenting vote, alongside the risk that potential output has been lowered by developments in the globalisation/tariff backdrop. It's worth noting that she still believes "It is very difficult to assess the current situation and it is possible that the cut of 0.25 percentage points advocated by a majority of the Executive Board is well balanced".

CHINA (MNI): China to Unveil 15th Five-Year Plan Next Month

MNI (Beijing) China will unveil its 15th Five-Year Plan at the Fourth Plenary Session of the 20th Central Committee of the Communist Party of China, scheduled for Oct. 20-23, Xinhua News Agency reported Monday following the latest Politburo meeting. Covering 2026 to 2030, the plan will set the overall strategy for social and economic development, stressing high-quality growth, the cultivation of new productive forces suited to local conditions, and balanced progress across the economy and society, the meeting stated.

CHINA (MNI): China Provides CNY500bln More for Investment - NDRC

MNI (Beijing) China will provide an additional CNY500 billion to support investment as the economy faces challenges, National Development and Reform Commission spokesperson Li Chao told a briefing on Monday. The CNY500 billion in new policy-based financial instruments will be used to supplement project capital, and efforts will be made to channel these funds into specific projects in a bid to push local governments to speed up their completion, she said.

BOJ (MNI): BOJ Noguchi Sees Flexible Policy; Underlying CPI Focus

Bank of Japan board member Asahi Noguchi said on Monday that the Bank's monetary policy is entering a phase requiring careful assessment. “I personally believe that the Bank needs to flexibly adjust its monetary policy while examining price developments, in response to economic developments at home and abroad at the time,” Noguchi told the Sapporo Chamber of Commerce and Industry. He downplayed the prospect of an imminent rate hike, emphasising the need to assess underlying inflation carefully.

BOJ (MNI): BOJ Decisions Inconsistent - Ex-BOJ's Yamamoto

A former BOJ official calls for greater consistency in policy rate decisions. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): Japan Polls Split on Whether Koizumi or Takaichi Leads LDP Race

With less than a week until Japan’s ruling party is set to elect a new leader, opinion polls are split over whether political scion Shinjiro Koizumi or right-leaning Sanae Takaichi has the most backing among the party’s supporters. The polls show that while Koizumi and Takaichi are still the two frontrunners, none of the five candidates taking part in the race is likely to win a majority in the first round of voting, an outcome that would trigger a runoff between the two leading candidates.

MOLDOVA (MNI): Moldova's Pro-EU Party Succeeds in Fending Off Pro-Russian Challenge

The Central Electoral Commission of Moldova (CEC) has confirmed that the pro-EU Party of Action and Solidarity (PAS) founded and de facto led by President Maia Sandu secured 50.2% of the vote in Sunday's elections, retaining its majority in parliament for another term. The elections were held amid accusations of Russian meddling and heightened geopolitical tensions in eastern Europe. The PAS was up against several pro-Russian parties advocating rapprochement with Moscow. The pro-Russian Patriotic Electoral Bloc (BEP) led by ex-President Igor Dodon came second, garnering 24.2% of the vote. Dodon cried foul and said that 'if anything is falsified (...), we won't recognise the parliamentary elections'.

DATA

UK DATA (MNI): BOE Credit Data Broadly In Line, Weaker Mortgage Lending, Higher M4

- UK AUG M4 MONEY SUPPLY +0.4% M/M, +3.4% Y/Y

- UK BOE AUG MORTGAGE APPROVALS 64,680

- UK BOE AUG SECURED LENDING GBP4.31 BLN

- UK BOE AUG CONSUMER CREDIT GBP1.69 BLN

BOE money and credit data for August came in broadly in line with expectations, though there were slight drops in secured lending and mortgage approvals. Mortgage rates fell due to the August rate cut, though the bar for future base rate cuts appears high. M4 money supply increased on the year at a faster rate than in July. Despite steady and in-line mortgage approvals data (64.7k vs 64.6k cons, 65.4k July), net lending on dwellings came in slightly below expectations at GBP4.31bn (vs 4.8bn cons, 4.52bn July).

SPAIN DATA (MNI): HICP Inline, Energy Upward Driver as Expected

- SPAIN SEP FLASH HICP +0.1% M/M, +3.0% Y/Y

- SPAIN SEP FLASH CPI -0.4% M/M, +2.9% Y/Y

- SPAIN SEP FLASH CORE CPI +2.3% Y/Y

Spanish flash September HICP was inline with consensus on a rounded basis at 3.0% Y/Y (vs 3.0% cons, 2.7% prior). On a monthly basis, HICP was 0.1% (0.2% cons). Core HICP (excluding energy and unprocessed foods) was estimated softer than before, at 2.4% Y/Y (vs 2.7% prior), the lowest rate in the category since March. National-level flash CPI was lower than expected, meanwhile, at 2.9% Y/Y (vs 3.1% cons, 2.7% prior), with core CPI at 2.3% Y/Y (vs 2.5% cons, 2.4% prior). The headline CPI Y/Y uptick is mainly due to "fuel and electricity prices falling less than in September 2024", INE notes.

SPAIN DATA (MNI): Retail Sales Momentum Remains Solid

Spanish retail sales momentum remains solid, and will contribute positively to household consumption growth going forward. Resilient growth momentum has been a key argument in favour of recent positive ratings action (e.g. Fitch and Moody's upgrades on Friday), and analysts expect Spain's sequential GDP outperformance to continue in the quarters ahead. In August, SWDA retail sales rose 0.4% M/M, rebounding from July's -0.4% fall. This left 3m/3m growth at 1.5% for the second consecutive month. 3m/3m momentum has been above 1% for the last five months.

SWITZERLAND DATA (MNI): GDP Revisions Mean Q2 Q/Q Growth Marginally Revised Up

Swiss GDP benchmark revisions yielded a "largely unchanged" overall economic interpretation of the figures. For Q2 2025, "the revised GDP figures confirm the slight increase in Switzerland's GDP adjusted for sporting events in the second quarter of 2025 (+0.2%, before revision: +0.1%). This reflects the expected correction following the previous quarter's above-average growth (+0.8%, beforerevision: +0.7%)."

NORWAY DATA (MNI): Retail Sales Volumes Remain on Steady Upward Trend

Norwegian retail sales excluding motor vehicles rose 0.2% M/M SA in August. Since June 2024, retail sales volumes have been on a steady upward trend and have underpinned household consumption. On a 3m/3m basis, sales grew 0.9% after 1.1% in July. Annual sales growth was 5.0% Y/Y (vs 5.1% prior). Similar trends can be seen in retail sales excluding motor vehicles and fuel. The Q3 Regional Network survey saw retail trade expected output at 0.4% this quarter and 0.5% Q/Q in Q4.

RATINGS: Upgrades for Spain, Negative Outlook Action for France

Sovereign rating reviews of note from after hours on Friday include:

- Fitch upgraded Spain to A; Outlook Stable

- Fitch affirmed Sweden at AAA; Outlook Stable

- Moody's upgraded Spain to A3, outlook stable

- Morningstar DBRS confirmed Croatia at A, Stable Trend

- Scope Ratings affirmed Croatia at A-; Outlook changed to Positive

- Scope Ratings affirmed France at AA-; Outlook changed to Negative

FOREX: USD weaker, Reeves Eyed

- The USD is slipping against most others in G10 early Monday, keeping the USD Index closely glued to the 50-dma of 98.038 - a level that's helped dictate price action well since the beginning of August. The inability of the USD to build on last week's gains does suggest those looking for a near-term greenback bounce may need more support before progress toward a more sustained recovery and the stress on the labor market remains the key near-term driver.

- The JPY, AUD are the firmest performers in G10 - with the JPY adding to gains as the Japanese government confirm an upgraded near-term view on the economy and economic conditions.

- Much market focus on UK Chancellor Reeves' appearance at the Labour Party Conference later today, at which she'll defend the government's record on the economy and potentially set out further clues for her intentions into the Autumn Budget as pressure grows on how to close the fiscal gap without breaching manifesto commitments of higher income tax, VAT or national insurance.

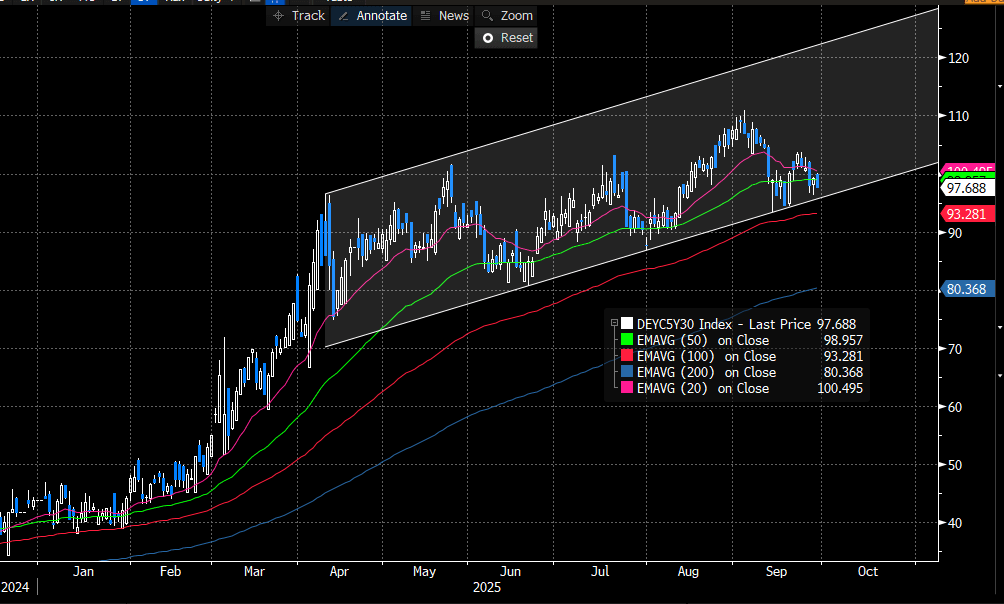

EGBS: German Curve Bull Flatter Amid Russia/Ukraine and US Shutdown Risks

The German curve is bull flatter, but trendline support in 5s30s remains intact for now. Yields are 1 to 3bps lower across the cure, with 5s30s down 1.5bps at 97.7bps. Trendline support resides at 95.7bps today.

- This morning’s headline flow has been relatively light, but markets have been digesting ongoing Russia/Ukraine tensions, increased US government shutdown risks and semi-core/peripheral EGB ratings action since Friday’s close.

- Bund futures are +19 ticks at 128.45, off session highs of 128.57. Resistance at the 20-day EMA (128.45) has been pierced, exposing the Sep 17 high at 129.13.

- 10-year EGB spreads to Bunds are biased up to 1bp tighter with the exception of OATs. Diverging ratings action are playing a part. France’s sovereign rating outlook was moved to negative at Scope Ratings on Friday, while Spain received one-notch upgrades at both Fitch & Moody’s. European equities are off session highs, but remain up 0.35% today.

- In data, Spanish flash September core HICP was a little softer-than-expected, but had a limited market impact. Eurozone September sentiment was a touch above consensus at 95.5 (vs 95.3 cons and prior).

- ECB’s Makhlouf suggested the bank was “near the bottom” of its easing cycle. These were Makhlouf’s first comments since the September decision. Overall, we’d say they are broadly in line with the Governing Council median. ECB Chief Economist Lane is scheduled to speak at 1300BST.

Figure 1: German 5s30s Curve

GILTS: Bull Flattening, Ramsden & Reeves Eyed

Gilts have rallied alongside global core FI peers to start the week, with U.S. government shutdown risk in focus (despite the equity uptick).

- Lower crude oil prices provide some background support as well.

- Futures traded as high as 90.82 before easing back to ~90.70.

- The bearish technical structure in the contract remains evident, with initial support and resistance located at 90.26 & 91.28, respectively.

- Yields 1.5-3.0bp lower, curve flatter.

- Chancellor Reeves has spoken with several local media outlets before her ~12:00 London address at the Labour Party conference.

- Reeves reiterated the government’s election pledge not to lift the 3 major taxes, while pushing back against the idea of a wealth tax.

- The UK’s ongoing fiscal deterioration is well-documented (limiting gilt rallies and keeping bearish/steepener technical setups in place), as such, pre-Budget comms from Reeves are set to provide the focal point of her address.

- Elsewhere, BBG sources have suggested that Reeves “is debating whether to get rid of the Office for Budget Responsibility’s annual March outlook to strengthen her commitment to holding just a single fiscal event a year and bring greater stability to economic policy making”.

- SONIA futures -1.0 to +2.0, strip twist flattens.

- BoE-dated OIS little changed, showing 4.5bp of easing through year-end and fully discounting the next cut through the end of the April MPC.

- BoE Deputy Governor Ramsden is set to speak from 13:00 London. We view him as the most dovish MPC member that didn’t vote for a rate cut earlier this month.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Nov-25 | 3.960 | -0.8 |

Dec-25 | 3.924 | -4.4 |

Feb-26 | 3.819 | -14.8 |

Mar-26 | 3.788 | -18.0 |

Apr-26 | 3.709 | -25.9 |

Jun-26 | 3.690 | -27.8 |

EQUITIES: EuroStoxx 50 Futures Breach Key Resistance and Bull Trigger at 5525.00

Eurostoxx 50 futures have started the week on a bullish note. Today’s gains have resulted in a breach of key resistance and the bull trigger at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend and paves the way for a climb towards 5564.82, a Fibonacci projection. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Initial firm support lies at 5433.67, the 20-day EMA. A bull cycle in S&P E-Minis remains intact and the latest pullback is considered corrective. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, the contract has recently pierced initial support at the 20-day EMA, currently at 6640.59. A clear breach of this average would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6526.11.

- Japan's NIKKEI closed lower by 311.24 pts or -0.69% at 45043.75 and the TOPIX ended 55.45 pts lower or -1.74% at 3131.57.

- Elsewhere, in China the SHANGHAI closed higher by 34.426 pts or +0.9% at 3862.532 and the HANG SENG ended 494.68 pts higher or +1.89% at 26622.88.

- Across Europe, Germany's DAX trades higher by 56.9 pts or +0.24% at 23795.84, FTSE 100 higher by 46.28 pts or +0.5% at 9330.91, CAC 40 up 20.97 pts or +0.27% at 7890.84 and Euro Stoxx 50 up 16.56 pts or +0.3% at 5516.02.

- Dow Jones mini up 180 pts or +0.39% at 46736, S&P 500 mini up 34 pts or +0.51% at 6730.5, NASDAQ mini up 163.25 pts or +0.66% at 24889.5.

Time: 10:00 BST

COMMODITIES: WTI Futures Holding Onto Recent Gains, Key Resistance at $68.43

WTI futures are holding on to their recent gains. The contract has breached resistance at $65.43, the Sep 2 high and this has improved the short-term condition for bulls. However, the next key resistance is at $68.43, the Jul 30 high, where a break is required to signal scope for a stronger recovery. For bears, a reversal lower would refocus attention on key support at $60.85. A break of this level would reinstate a bearish theme. The trend condition in Gold is unchanged and a bull cycle remains in play. The yellow metal has started the week on a bullish note, trading to a fresh cycle high, confirming a resumption of the primary uptrend. Note that MA studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3831.4, a Fibonacci projection. On the downside, support to watch lies at $3646.3, the 20-day EMA. A pullback would be considered corrective.

- WTI Crude down $0.73 or -1.11% at $64.92

- Natural Gas down $0.02 or -0.53% at $3.188

- Gold spot up $58.88 or +1.57% at $3819.13

- Copper up $4 or +0.84% at $481.05

- Silver up $0.9 or +1.95% at $46.9881

- Platinum up $26.98 or +1.71% at $1606.7

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 29/09/2025 | 1130/0730 | Fed Governor Christopher Waller | ||

| 29/09/2025 | 1200/1400 | ECB Lane In Policy Panel At Inflation Conference | ||

| 29/09/2025 | 1200/0800 | Cleveland Fed's Beth Hammack | ||

| 29/09/2025 | 1200/1300 | BOE Ramsden On ECB Inflation Panel | ||

| 29/09/2025 | 1330/0930 | NY Fed's Roberto Perli | ||

| 29/09/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/09/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 29/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 29/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 29/09/2025 | 1730/1330 | St. Louis Fed's Alberto Musalem | ||

| 29/09/2025 | 1730/1330 | Ex-St. Louis Fed's James Bullard | ||

| 29/09/2025 | 1730/1330 | New York Fed's John Williams | ||

| 29/09/2025 | 2200/1800 | Atlanta Fed's Raphael Bostic | ||

| 30/09/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 30/09/2025 | 2350/0850 | ** | Industrial Production | |

| 30/09/2025 | 2350/0850 | * | Retail Sales (p) | |

| 30/09/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 30/09/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 30/09/2025 | 0130/1130 | * | Building Approvals | |

| 30/09/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 30/09/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 30/09/2025 | 0600/0800 | ** | Retail Sales | |

| 30/09/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/09/2025 | 0600/0800 | ** | Retail Sales | |

| 30/09/2025 | 0600/0700 | * | Quarterly current account balance | |

| 30/09/2025 | 0600/0700 | *** | GDP Second Estimate | |

| 30/09/2025 | 0645/0845 | *** | HICP (p) | |

| 30/09/2025 | 0645/0845 | ** | PPI | |

| 30/09/2025 | 0645/0845 | ** | Consumer Spending | |

| 30/09/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/09/2025 | 0755/0955 | ** | Unemployment | |

| 30/09/2025 | 0800/1000 | ** | PPI | |

| 30/09/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/09/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/09/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/09/2025 | 0900/1100 | *** | HICP (p) | |

| 30/09/2025 | 1000/0600 | Fed Vice Chair Philip Jefferson | ||

| 30/09/2025 | 1100/1300 | ECB Cipollone In Panel At Sibos | ||

| 30/09/2025 | 1150/1250 | BOE Lombardelli Panel On MonPol, Bank of Finland | ||

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1250/1450 | ECB Lagarde Keynote at MonPol Conference, Bank of Finland | ||

| 30/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 30/09/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/1500 | ECB Elderson In Panel On Climate Action | ||

| 30/09/2025 | 1300/0900 | Boston Fed's Susan Collins | ||

| 30/09/2025 | 1325/1425 | BOE Mann Fireside Chat At FT | ||

| 30/09/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/09/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 30/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 30/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 30/09/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 30/09/2025 | 1530/1630 | BOE Breeden Speech At Cardiff University | ||

| 30/09/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 30/09/2025 | 1600/1200 | ** | USDA GrainStock - NASS |