MNI US OPEN - Miran Highlights Busy Fed Speak Calendar

EXECUTIVE SUMMARY

- US HOUSE GROUP MEETS PREMIER LI AS THEY KICK OFF CHINA VISIT

- CHINA LPR REMAINS UNCHANGED IN SEPTEMBER

- JAPAN’S LDP LEADERSHIP RACE KICKS OFF WITH FIVE CONTENDERS

- RBA’S BULLOCK SAYS BOARD WILL WEIGH STRONGER DATA NEXT WEEK

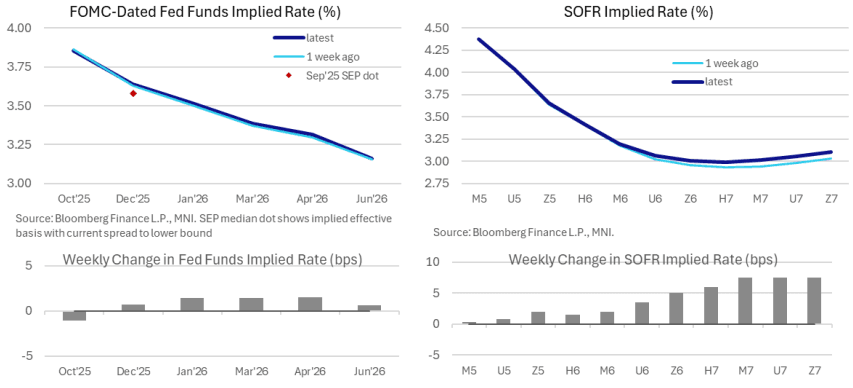

Figure 1: FOMC-Dated Fed Funds Implied Rate (%) and SOFR Implied Rate (%)

NEWS

US/CHINA (BBG): US House Group Meets Premier Li as They Kick Off China Visit

A group of senior US House representatives arrived in China on Sunday for talks with President Xi Jinping’s government — the first such official visit in six years — as the world’s largest economies edge closer to a trade deal. The US group, led by Democrat and former House Armed Services Committee chairman Adam Smith, kicked off the visit by meeting with Premier Li Qiang at the Great Hall of the People in Beijing.

US/SWITZERLAND (FT): Switzerland in Fresh Push to Woo Donald Trump on Tariffs

Switzerland is offering to buy more American weapons and energy products and make more investments in the US, in a fresh push to persuade the Trump administration to lower its tariffs on Swiss imports. The Swiss government has engaged in negotiations after President Donald Trump went ahead with his threat to impose an unexpected 39 per cent rate on the Alpine country — one of the highest levels applied to a western ally — because of the trade imbalance between the two countries.

US/INDIA (BBG): Trump’s $100,000 Visa Targets a $280 Billion India Success Story

Donald Trump’s move to curtail H-1B visas threatens to rewrite the rules for one of India’s biggest business success stories, a decades-old model that’s grown into a $280 billion industry and underpins much of the technology behind the world’s largest corporations. The US president’s order on Friday — which requires a $100,000 fee for H-1B applications — will force a rethink at Indian outsourcers led by Tata Consultancy Services Ltd. and Infosys Ltd., who use the program to deploy tens of thousands of engineers across American clients from Citigroup Inc. to Walmart Inc. The two Indian software exporters’ shares slid more than 3% on Monday.

ECB (MNI): Tariffs Push Inflation Expectations Up - ECB Bulletin

Tariffs were considered inflationary by around 40% of respondents in the ECB’s June Consumer Expectation Survey in June, raising that month's inflation expectations by 0.2 percentage points one year ahead, 0.13pp three years ahead and 0.06pp in the five years ahead horizon, the central bank's latest economic bulletin published on Monday. A quarter of European consumers surveyed believed that trade tensions will slow economic growth, cutting their expectations for growth over the next 12 months by 0.4 percentage points.

CHINA (MNI): China Sept LPR Remains Unchanged

MNI (Beijing) China's Loan Prime Rate held steady on Monday, in line with expectations, with more easing expected later in the year as the economy suffers stronger headwinds, according to a statement on the website of People’s Bank of China. The LPR remained unchanged at 3.0% for the one-year maturity and 3.5% for the five-year tenor and over. Both rates fell in May by 10bp after the PBOC lowered the 7-day reverse repo rate – its benchmark policy rate – 10bp to 1.4% on May 8, followed by a 50bp reduction to the reserve requirement ratio on May 15.

CHINA (MNI): China Sets 4% Steel Growth Goal, Bans New Capacity

MNI (Beijing) China has set targets of around 4% annual value-added growth for the steel sector in 2025 and 2026, along with strict prohibitions on expanding production capacity, according to a two-year plan unveiled by the Ministry of Industry and Information Technology on Monday. Policy tools will focus on capacity controls, differentiated management, and directing resources toward leading firms, while coordinating fiscal, taxation, and financial measures.

JAPAN (BBG): Japan’s LDP Leadership Race Kicks Off With Five Contenders

Japan’s ruling party leadership race formally kicked off Monday under close market scrutiny, with the outcome likely to determine who will lead the nation following Prime Minister Shigeru Ishiba’s decision to step down. The five candidates will face off in the party’s Oct. 4 presidential election, and the winner will face the urgent task of rebranding the party to stop a drift of supporters to rival populist parties that has stripped the LDP of its majorities in both chambers of parliament in recent elections.

JAPAN (BBG): BOJ Removes Japan Stocks Overhang With Slow ETFs Sell-Down

A large overhang that threatened the Japanese equity market is being removed with the central bank laying out a century-long plan to offload its massive holdings of exchange-traded funds. While benchmark stock gauges fell Friday in a knee-jerk reaction when the Bank of Japan said it would be selling its ¥75 trillion ($507 billion) stockpile, traders quickly pared much of the decline as focus turned to the very gradual nature of the program. The BOJ intends to reduce its holdings by about ¥620 billion by market value per year.

ASIA (BBG): Super Typhoon Lashes Philippines on Track Toward Hong Kong

Hong Kong is bracing for widespread damage and disruption from the approaching Super Typhoon Ragasa, which is currently churning off the northeast coast of the Philippines with tree-snapping winds. The powerful storm is packing maximum sustained winds of 230 kilometers (143 miles) per hour, according to the Hong Kong Observatory, equivalent to a Category 4 hurricane on the five-step Saffir-Simpson scale. The Philippines warned of life-threatening conditions.

RBA (BBG): RBA’s Bullock Says Board Will Weigh Stronger Data Next Week

Australia’s central bank Governor Michele Bullock said the interest rate-setting board will weigh recent evidence showing the economy has been performing in line or slightly stronger than anticipated at next week’s policy meeting. Inflation has fallen “substantially” to be inside the Reserve Bank’s 2-3% target and the labor market is “close to full employment,” Bullock said in her opening remarks to a parliamentary panel in Canberra on Monday.

CRYPTO (BBG): Cryptocurrencies Sink as $1.5 Billion in Bullish Bets Wiped Out

Cryptocurrency traders saw more than $1.5 billion in bullish wagers liquidated on Monday, triggering a sharp selloff that hit smaller tokens hardest. Ether slumped as much as 9% to $4,075 as nearly half a billion dollars of leveraged long positions in the second-largest token were liquidated, according to data from Coinglass. Bitcoin declined almost 3% to $111,998.

DATA

CHINA (MNI): Service Consumption Maintains Rapid Growth - MOFCOM

MNI (Beijing) China’s retail sales of services rose 5.1% y/y in the first eight months, easing slightly from 5.2% growth in January-July, the Ministry of Commerce said Monday, with the increase supported by strong summer demand for tourism and leisure sports. The 3.6% year-on-year growth in retail sales of goods last month was supported by the trade-in scheme, with sales of furniture, home appliances, stationery and office supplies, and communication equipment rising by 18.6%, 14.3%, 14.2% and 7.3% respectively.

RATINGS: Italy Upgraded at Fitch, France Downgraded at DBRS

Sovereign rating reviews of note from after hours on Friday include:

- Fitch upgraded Italy to BBB+; Outlook Stable

- Moody's affirmed Poland at A2; Outlook changed to Negative from Stable

- S&P affirmed Ireland at AA; Outlook Positive

- Morningstar DBRS upgraded Cyprus to A, Stable Trend

- Morningstar DBRS downgraded France to AA, Trend Changed to Stable

- Morningstar DBRS confirmed Norway at AAA, Stable Trend

- Morningstar DBRS confirmed Finland at AA (high), Stable Trend

- Morningstar DBRS confirmed the United States of America at AAA, Stable Trend

- Scope Ratings affirmed the Czech Republic at AA-; Outlook Stable

FOREX: USD Index Eases Off Recovery Highs, Fed Speakers Awaited

- The USD index tracks moderately lower on Monday, easing around 30 pips from the overnight peak that saw the index print a fresh recovery high at 97.82. Markets are trading with a subdued tone amid a lighter economic calendar to start the week, with central bank speakers dominating the schedule later today.

- The likes of EUR and GBP trade on a surer footing, rising around 0.15%. Large option expiries for EURUSD between the 1.17/18 mark might define the short-term range, following the post-Fed volatility last week that saw the pair reverse from 1.1919 cycle highs. Support to watch is 1.1667. the 50-day EMA.

- GBPUSD is broadly consolidating its solid bump lower last week, struggling to get back above the 1.35 mark. Fiscal concerns continue to be front and centre following last Friday’s borrowing data. The next support to watch lies at 1.3441, a trendline support drawn from the Aug 1 low.

- For NZDUSD, the sharp reversal from 0.6000 to current spot levels renews the focus on a significant pivot point at 0.5800, which coincides with the 50% retracement of the year’s range. Furthermore, the pair is currently trying to break a trendline drawn from the year’s lows, which may bolster the bearish momentum in coming sessions. Below 0.5800, 0.5728 and 0.5636 would be the most obvious targets for a deeper selloff.

- There are five Fed speakers in the calendar on Monday, with markets most likely to focus on further comments from Fed’s Miran, who is speaking at the Economic Club of New York. We may also have comments from Bank of England’s Bailey and Pill. Governor Bailey has a fireside chat on supervision culture.

EGBS: Bunds Move Away From Initial Support; Spreads Widen on Equity Downtick

Bund futures have moved away from previously noted support at 128.04, now +7 ticks at 128.26. Initial resistance is the 20-day EMA at 128.63.

- Bunds have found light support from a pullback in European equity and Brent crude futures this morning. Headline flow has otherwise been light.

- German yields are up to 0.5bps lower across the curve.

- The downtick in equities contributes to a modest widening of 10-year EGB spreads to Bunds (up to +1bp). OATs the marginal underperformer after the once-notch sovereign rating downgrade of France from Morningstar DBRS on Friday. BTPs don’t see much of a lasting tailwind after Italy received the (at least partially expected) one-notch rating upgrade from Fitch

- EGB supply is due from the EU and Belgium this morning. Note that this will be the first auction at which the EU will hold a second non-competitive round (at which a further 20% would be available the following day).

- No key regional data to start the week, with focus on tomorrow’s flash PMIs.

- ECB’s Lane and Nagel are scheduled to speak later. Broader GC commentary since the September decision suggests there is little appetite for another rate cut this cycle, with most officials deeming rates to be appropriate at current levels for now.

GILTS: Recovery From Lows Holds

Downticks in the major global equity benchmarks and a move away from session highs in crude oil allow wider core global FI markets to move away from session lows.

- Little of note on the local news front over the weekend, after Friday’s PSNB data revealed the latest instance of fiscal deterioration.

- Gilt futures traded through Friday’s lows & first support (90.65), before basing at 90.60 and recovering back to ~90.80.

- Initial support and resistance comes in at 90.31 & 91.14, risks to the recent bullish phase have increased despite the recovery from lows.

- Yields 1-2bp lower across the curve.

- GBP STIRs little changed, trading towards the hawkish end of their recent range.

- SONIA futures flat to +1.0.

- BoE-dated OIS shows just ~1.5bp of easing for November & ~6bp through year-end.

- We think that markets underprice the prospect of both a November and a December cut.

- We also look into the BoE’s APF decision in our BoE review.

- Comments from BoE chief economist Pill are due this afternoon (13:30 London), followed by comments from Governor Bailey (19:00 London). Expect Pill’s comments to be of greater interest for markets, as he speaks on monetary policy frameworks, while Bailey speaks on supervisory matters.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Nov-25 | 3.950 | -1.7 |

Dec-25 | 3.905 | -6.2 |

Feb-26 | 3.799 | -16.9 |

Mar-26 | 3.766 | -20.2 |

Apr-26 | 3.693 | -27.4 |

Jun-26 | 3.667 | -30.0 |

EQUITIES: E-Mini S&P Targets Fibonacci Projection Point at $6748.50 Next

Eurostoxx 50 futures recently traded through resistance around the 20-day EMA - a bullish development - and the subsequent rally reinforces a bullish theme. The move signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support has been defined at 5302.00, the Sep 2 low. Clearance of this level is required to reinstate a bearish theme. A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high on Friday. Price has breached the 6700.00 handle and this signals scope for an extension towards 6748.50, a Fibonacci projection point. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6602.01, the 20-day EMA.

- Japan's NIKKEI closed higher by 447.85 pts or +0.99% at 45493.66 and the TOPIX ended 15.49 pts higher or +0.49% at 3163.17.

- Elsewhere, in China the SHANGHAI closed higher by 8.487 pts or +0.22% at 3828.576 and the HANG SENG ended 200.96 pts lower or -0.76% at 26344.14.

- Across Europe, Germany's DAX trades lower by 107.8 pts or -0.46% at 23531.47, FTSE 100 higher by 6.99 pts or +0.08% at 9223.57, CAC 40 down 11.22 pts or -0.14% at 7842.68 and Euro Stoxx 50 down 8.52 pts or -0.16% at 5450.29.

- Dow Jones mini down 117 pts or -0.25% at 46534, S&P 500 mini down 14 pts or -0.21% at 6708.5, NASDAQ mini down 60.5 pts or -0.24% at 24806.25.

Time: 10:00 BST

COMMODITIES: Gold Trades to Fresh High, Remains in a Clear Bull Cycle

The trend condition in WTI futures is unchanged - a bear cycle remains intact and the latest recovery is considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would open $57.71, the May 30 low. Gold remains in a clear bull cycle and short-term pullbacks are for now, considered corrective. A fresh all-time high, once again last week, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3744.2, a Fibonacci projection. Initial firm support lies at $3577.9, the 20-day EMA. Note that MA studies are in a bull-mode position, highlighting a dominant uptrend.

- WTI Crude up $0.36 or +0.57% at $63.04

- Natural Gas up $0.04 or +1.49% at $2.931

- Gold spot up $35.04 or +0.95% at $3720.5

- Copper up $1.4 or +0.3% at $464.25

- Silver up $0.61 or +1.42% at $43.6868

- Platinum up $16.54 or +1.17% at $1425.4

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 22/09/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/09/2025 | 1230/1330 | BOE Pill At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/1545 | ECB Lane At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/0945 | New York Fed's John Williams | ||

| 22/09/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 22/09/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 22/09/2025 | 1600/1200 | Cleveland Fed's Beth Hammack | ||

| 22/09/2025 | 1600/1200 | Richmond Fed's Tom Barkin | ||

| 22/09/2025 | 1715/1315 | BOC Sr Deputy speaks at LSE panel on supervision | ||

| 22/09/2025 | 1800/1900 | BOE Bailey Fireside Chat On Supervision | ||

| 22/09/2025 | 1945/1545 | BOC Deputy Kozicki speaks at BIS panel on central bank frameworks | ||

| 23/09/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 23/09/2025 | - | Riksbank Meeting | ||

| 23/09/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/09/2025 | 0900/1000 | BOE Pill Fireside Chat At Pictet Research Institute Symposium | ||

| 23/09/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/09/2025 | 1230/0830 | * | Current Account Balance | |

| 23/09/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 23/09/2025 | 1300/0900 | Fed Governor Michelle Bowman | ||

| 23/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/09/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/09/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 23/09/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/09/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic | ||

| 23/09/2025 | 1420/1620 | ECB Cipollone In Bloomberg Fireside Chat | ||

| 23/09/2025 | 1635/1235 | Fed Chair Jay Powell | ||

| 23/09/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 23/09/2025 | 1815/1415 | BOC Governor Macklem speech in Saskatoon |