MNI US OPEN - Large Benchmark Payrolls Revisions Expected

EXECUTIVE SUMMARY

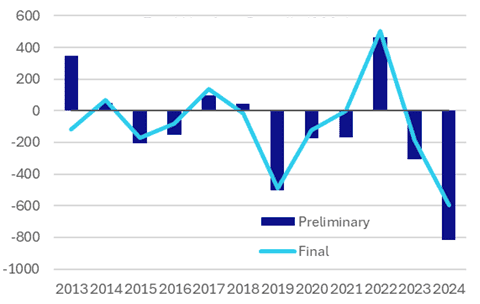

- MNI US PAYROLLS PRELIMINARY BENCHMARK REVISION PREVIEW

- THE RENEWED BID TO END QUARTERLY EARNINGS REPORTS: WSJ

- WHITE HOUSE PREPARING REPORT CRITICAL OF BUREAU OF LABOR STATISTICS: WSJ

- BOJ IS SAID TO SEE CHANCE OF HIKE THIS YEAR DESPITE POLITICS: BBG

- MACRON LOOKS FOR A NEW PRIME MINISTER AFTER BAYROU’S OUSTER

Figure 1: Level changes in preliminary and final benchmark revisions - total nonfarm payrolls (000s)

Source: MNI/BLS

NEWS

MNI US Payrolls Preliminary Benchmark Revision Preview

Tuesday’s preliminary annual payrolls benchmark revision is widely expected to imply large downward revisions to nonfarm payrolls growth through the twelve months to March 2025. We’ve seen estimates for a downward revision of at least 500k (using mid-point estimates when analysts quote a range) with a central guess of around -750k. History suggests the actual benchmark revision due with the Jan 2026 payrolls report will be smaller than what’s reported this week, but downward revisions could still be significant.

US (WSJ): The Renewed Bid to End Quarterly Earnings Reports

Public companies in the U.S. have dutifully shared financial results with investors every three months for the past 50-plus years. A new proposal hopes to change that. The Long-Term Stock Exchange plans to petition the Securities and Exchange Commission to eliminate the quarterly earnings report requirement and instead give companies the option to share results twice a year, the group told The Wall Street Journal.

US (WSJ): White House Preparing Report Critical of Bureau of Labor Statistics

Five weeks after President Trump fired the chief of the agency that gathers the country's labor and price data, his advisers are preparing a report laying out alleged shortcomings of the Bureau of Labor Statistics' jobs data, according to people familiar with the matter. The report takes a critical look at the BLS and lays out a historical overview of the agency's jobs-data revisions, they said. The administration is considering publishing the study, authored by the Council of Economic Advisers, in the coming weeks, according to these people.

FRANCE (BBG): Macron Looks for a New Prime Minister After Bayrou’s Ouster

French President Emmanuel Macron will appoint a new prime minister within days, after the current premier lost a confidence vote in the lower house of parliament. Prime Minister Francois Bayrou is formally presenting his resignation to Macron on Tuesday. Whoever Macron picks as his successor will need to assemble a government and then find a way to pass a budget in a starkly splintered National Assembly, an exercise that’s toppled the last two prime ministers.

NORWAY (MNI): Labour Wins Election While Progress Party Support Surges

Norwegian PM Jonas Gahr Støre has secured a second term in office following yesterday's election, with his centre-left Labour party winning 28% of the vote (53 seats out of 169, up from 48 prior). Labour and its allies (the Centre, Socialist Left, Green and Red parties) won 87 votes in total, a shade above the 85-seat threshold required for a

majority. This outcome is in line with the most likely scenario outlined in MNI's preview. As such, we don't expect major market moves in NOK FX and rates today, with the status quo around the aggregate fiscal stance likely to be retained.

UK (FT): Rachel Reeves to Tell Ministers to Prioritise Fight Against UK Inflation

Chancellor Rachel Reeves will on Tuesday tell ministers they must join the fight against inflation, in a sign of her fears that rising prices in Britain could hit growth and worsen the cost of living crisis. Reeves will tell colleagues at a cabinet meeting devoted to growth that they must scrap regulatory burdens on companies, resist public sector pay demands and back her fiscal rules, government officials said.

ISRAEL/MIDEAST (BBG): Israel Orders All Gaza City Residents to Leave Ahead of Assault

Israel ordered Gaza City’s one million residents to leave in advance of a major military offensive, with top officials vowing devastation unless Iran-backed Hamas surrenders. Global outrage has grown since Israel announced last month that it would take over the city, home to half the enclave’s population, with longtime European allies threatening to cut trade ties and planning to back Palestinian statehood at the United Nations in two weeks.

BOJ (BBG): BOJ Is Said to See Chance of Hike This Year Despite Politics

Bank of Japan officials are of the view that it may be possible to raise the benchmark interest rate again this year regardless of domestic political instability, as economic conditions have developed in line with expectations, according to people familiar with the matter. The US-Japan trade deal has removed a key source of uncertainty, but the BOJ is likely to keep its rate unchanged at 0.5% when it next sets policy on Sept. 19, as officials are still assessing the economic impact of US tariffs both at home and abroad, according to the people. The bank’s policy board will also meet in October and December.

BOJ (RTRS): BOJ Likely to Trim Super-Long Bond Buying in Q4, Sources Say

The Bank of Japan is likely to slightly reduce its purchases of super-long government bonds in the fourth quarter despite recent rises in yields for those maturity zones, said three sources familiar with its thinking. Any such move would be in line with market expectations and the central bank's guidance that it will prioritise tapering JGB maturity zones for which the ratio of its holdings against total issuance remains high. The BOJ will make a final decision on September 30, which could be swayed by the outcome of a 20-year government bond auction on September 17 and the degree of market volatility in super-long Japanese government bond (JGB) yields, they said.

JAPAN (BBG): Japan’s LDP Mulls All-Member Vote for PM on Oct. 4, Reports Say

Japan’s ruling party is set to decide when and how an upcoming leadership race will be held, after Prime Minister Shigeru Ishiba’s resignation announcement triggered a vote to choose his successor. The Liberal Democratic Party is considering holding a full-scale leadership election with the participation of just over 1 million rank-and-file party members from across the nation on Oct. 4, according to local media reports including broadcasters NHK and TBS. LDP officials see a need to sound out all its members, given the need to revive the party’s fortunes, NHK reported.

JAPAN (BBG): Japan’s Kono Says BOJ Needs to Hike Rate to Fix Yen, Inflation

The Bank of Japan should raise its benchmark rate to support the yen and curb inflation, Liberal Democratic Party lawmaker and former digital transformation minister Kono Taro said, as political uncertainty clouds the outlook for economic policy. “We need to fix the yen rate. In order to do that, the Bank of Japan needs to increase the interest rate,” Kono said Tuesday in an interview with Shery Ahn on Bloomberg TV.

CHINA (MNI INTERVIEW): China to Advocate for SCO Free Trade Zone

A Chinese diplomat provides insight into last week's SCO summit. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

RBNZ (MNI EXCLUSIVE): RBNZ Leadership Woes Present Reform Opportunity

Former senior RBNZ leaders say the bank's credibility rests on strong successors. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

THAILAND (BBG): Thaksin Gets One Year in Jail for Dodging Thai Prison Term

Thaksin Shinawatra, a two-time former Thai prime minister, was ordered by a court to serve one year in prison to complete a past conviction, the latest in a string of setbacks for the influential politician whose daughter was ousted as prime minister last month. The Supreme Court’s Criminal Division for Holders of Political Positions ruled that Thaksin’s six-month stay in a police hospital in 2023, when he began serving a reduced sentence for abuse of power and conflicts of interest, did not count toward his term. The ruling is final and cannot be appealed.

INDONESIA (BBG): New Indonesia Finance Chief Vows to Maintain Fiscal Discipline

Indonesia’s new finance minister Purbaya Yudhi Sadewa vowed to maintain fiscal discipline even as he hinted he’d allow more state spending than his predecessor. “I ask the Ministry of Finance to work with me so that fiscal policy can be a strong instrument to encourage economic growth,” he said at a ceremony with outgoing finance minister Sri Mulyani Indrawati in Jakarta on Tuesday. “We maintain the principle of fiscal discipline, so that the national budget remains healthy and credible to support the national agenda.”

CORPORATE (WSJ): Anglo American, Teck to Merge, Creating Copper Giant

Anglo American and Teck Resources have agreed to merge in a deal that will create one of the world’s largest copper producers with a combined market value of more than $53 billion. The deal comes as miners look to shore up access to copper, which is essential to the transition from fossil fuels to renewable energy and a core component in wiring used in the booming data-center sector.

DATA

UK DATA (MNI): BRC Aug Retail Sales Look Strong But Boosted by Food Inflation

- UK BRC AUG BY VALUE SHOP SALES LFL +2.9% Y/Y, TOTAL +3.1% Y/Y

BRC Shop Sales data for August shows a 3.1% Y/Y increase in total retail sales (vs 2.5% Jul, 1.0% Aug '24), above the 12-month average of 2.0%. Like-for-like sales grew by 2.9% Y/Y (vs 1.8% Jul, 0.8% Aug '24). High summer temperatures, the August rate cut and back-to-school purchases are highlighted as drivers by the BRC. However, with goods inflation (particularly food inflation) running at a fast pace, sales look a lot less impressive and there may be some boost here from calendar effects.

FRANCE DATA (MNI): July IP Higher Than Cons Due to Energy / Water; Manufacturing Soft

- FRANCE JUL IND PROD -1.1% M/M, +1.3% Y/Y (VS +3.7% M/M, +2.2% Y/Y JUN)

- FRANCE JUL MANUF OUTPUT -1.7% M/M, +1.5% Y/Y (VS +3.5% M/M, +2.6% Y/Y JUN)

July France industrial production was stronger than expected, at -1.1% M/M (-1.4% consensus). This followed the strong June (3.7%, revised from 3.8%). However, it appears as though it is energy and water / sewerage driving the upside surprise here with manufacturing softer-than-expected. Underlying manufacturing was weaker than the headline print this time, at -1.6% M/M, the lowest sequential reading since May 2024. On a 3m/3m comparison, the sector remains up, at 1.5% (2.6% prior).

AUSTRALIA DATA (MNI): Growth Recovery Continued in Q3, August Costs/Prices Moderated

August NAB business confidence fell to +4 from +8 but conditions improved to +7 from +5. Both have improved in Q3 to date by around 3 points signalling that GDP growth should continue to recover. The price/cost components were lower in August with purchase cost and retail price increases at multi-year lows, which should reassure the RBA. However, the Q3 average of final product prices is still around where it was in H1 signalling some stabilisation in disinflation. Labour demand also appears to have steadied.

AUSTRALIA DATA (MNI): Consumer Sentiment Weaker But Series Is Volatile

Westpac consumer sentiment fell 3.1% m/m to 95.4 in September after August's robust +5.7% m/m to 98.5. It remains in pessimistic territory but above the 2025 average helped by 75bp of monetary easing and lower inflation. RBA Deputy Governor Hauser had talked about "scarring" from contracting real incomes continuing to weigh on sentiment. There had not been an RBA meeting since the last confidence print. This month's decline was driven by increased concerns about the economic outlook and fears of unemployment.

FOREX: JPY Rallies as BoJ Report Suggests More Aggressive Tightening Schedule

- JPY started the session strong, carrying the theme through late Asia and early European trade. The stronger JPY helped aide USD weakness, prompting raising the importance of nearby USD Index support at 97.109, and into the bear trigger of 96.377. It's notable that today's USD weakness has not been triggered by a renewed pull lower in US yields (US 10y yield closed lower by over 5bps yesterday, but has steadied so far this morning).

- Instead, USDJPY selling looks the primary driver. JPY futures volumes are well ahead of average, with volumes supported by a sources report suggesting the BoJ see a strong chance of a further rate hike this year, despite the recent political upheaval in the ruling LDP. The piece reported some BoJ sources seeing the October meeting as a potential opportunity for tightening - a much more aggressive schedule than currently priced in.

- USD/JPY traded through the September lows in response, narrowing the gap with both the 100-dma of Y145.93 as well as decent-sized expiries into Y145.85-00 ($1.4bln).

- Focus for the duration of Tuesday trade rests on the annual benchmark payrolls revisions - which are expected to be marked notably lower for the 12 months into March - helping bolster the Oval Office's case for a more aggressive approach to monetary easing from the Fed. This morning's USD weakness is helping prop the major pairs through to new September highs headed into this week's economic and inflation data (today benchmark payrolls revisions, Wednesday PPI, Thursday CPI).

BONDS: Solid Gilt Auction Helps UK Paper Lightly Outperform German Peers

The strong 20-year Gilt auction helps UK paper extend this morning’s light outperformance versus German peers. Gilt yields are now 0.5 to 1.5bps higher across the curve, compared to the 0.5 to 2.5bp rise in German yields. The 10-year tenor underperforms on the UK curve, while Germany sees a clearer bear steepening dynamic.

- That leaves the 10-year Gilt/Bund spread 1bp narrower at 195bps, still above the August 25 closing low of 193bps.

- The German 5s30s curve is 1bp steeper at 106.2bps, moving away from this month’s 104.8bp low.

- Bund futures have drifted lower through the morning, currently -24 ticks at 129.07. The 129.00 handle has contained intraday downside for now, with key support not seen till 128.25 (Sep 4 low).

- Gilt futures have moved up to 91.48 following the 20-year auction, still -7 ticks on the session and shy of yesterday’s 91.61 high.

- OAT futures (-6 ticks at 121.83) haven’t seen much reaction to ex-PM Bayrou’s expected ousting following yesterday’s no-confidence vote. President Macron will try and appoint a new PM in the coming days. Note that a roll in Bloomberg’s 10-year OAT benchmark (now the 3.50% Nov-35 OAT) has skewed the 10-year OAT/Bund spread up to above 80bps. Meanwhile, the benchmark 10-year BTP/OAT spread is now negative for the first time.

- Alongside the Gilt auction, the Netherlands and Austria have sold bonds today. German greens are due at 1030BST, with the EU also holding a dual tranche syndication.

- Today’s regional data (French July industrial production and UK BRC shop sales) were not market moving. Global focus turns to the US preliminary payrolls revisions at 1500BST.

EQUITIES: Bull Cycle in E-Mini S&P Intact, Contract Close to Recent Highs

A corrective bear cycle in Eurostoxx 50 futures remains in play. Recent weakness resulted in a breach of 5368.87, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5377.49, the 20-day EMA. A clear break of it would be a bullish development. A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high last week, breaching the Aug 28 high of 6523.00. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6456.35, the 20-day EMA.

- Japan's NIKKEI closed lower by 184.52 pts or -0.42% at 43459.29 and the TOPIX ended 16.08 pts lower or -0.51% at 3122.12.

- Elsewhere, in China the SHANGHAI closed lower by 19.549 pts or -0.51% at 3807.292 and the HANG SENG ended 304.22 pts higher or +1.19% at 25938.13.

- Across Europe, Germany's DAX trades lower by 125.01 pts or -0.53% at 23680.44, FTSE 100 higher by 16.9 pts or +0.18% at 9238.13, CAC 40 up 0.05 pts or +0% at 7734.89 and Euro Stoxx 50 down 8.72 pts or -0.16% at 5354.09.

- Dow Jones mini up 2 pts or +0% at 45577, S&P 500 mini up 5.5 pts or +0.08% at 6511.5, NASDAQ mini up 35.75 pts or +0.15% at 23835.75.

Time: 10:00 BST

COMMODITIES: Gold Remains in a Clear Bull Cycle, Monday's Gains Reinforce Theme

The trend condition in WTI futures is unchanged - a bear cycle remains intact. The pullback from last Tuesday’s high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low. Gold remains in a clear bull cycle and last week’s gains plus Monday’s bullish start to the week, reinforce current conditions. The yellow metal has traded to a fresh all-time high. The break also confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a Fibonacci projection. Initial firm support lies at $3458.7, the 20-day EMA.

- WTI Crude up $0.8 or +1.28% at $63.09

- Natural Gas up $0.05 or +1.59% at $3.139

- Gold spot up $13.88 or +0.38% at $3650.52

- Copper up $0.15 or +0.03% at $456.05

- Silver down $0.12 or -0.28% at $41.2516

- Platinum up $5.18 or +0.37% at $1391.96

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 09/09/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 09/09/2025 | 1150/1350 | SNB's Schlegel at BIS fireside chat | ||

| 09/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 09/09/2025 | 1400/1000 | *** | Preliminary Benchmark Revision | |

| 09/09/2025 | 1515/1615 | BOE Breeden Moderates BIS Fireside Chat | ||

| 09/09/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 10/09/2025 | 0130/0930 | *** | CPI | |

| 10/09/2025 | 0130/0930 | *** | Producer Price Index | |

| 10/09/2025 | 0600/0800 | *** | CPI Norway | |

| 10/09/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/09/2025 | 0700/0900 | ** | Industrial Production | |

| 10/09/2025 | 0800/1000 | * | Industrial Production | |

| 10/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 10/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 10/09/2025 | 1145/1345 | SNB's Schlegel on Central Bank Communication in Vezia | ||

| 10/09/2025 | - | *** | Money Supply | |

| 10/09/2025 | - | *** | New Loans | |

| 10/09/2025 | - | *** | Social Financing | |

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1400/1000 | ** | Wholesale Trade | |

| 10/09/2025 | 1400/1000 | ** | Wholesale Trade | |

| 10/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 10/09/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result |