MNI US OPEN - FOMC Expected to Deliver a "Hawkish Cut"

EXECUTIVE SUMMARY

- MNI FED PREVIEW: WINTER OF DISCONTENT

- MNI BOC PREVIEW: FIRM HOLD, BUT HIKE TALK PICKING UP

- TRUMP TO PIT KEVIN HASSETT AGAINST TRIO OF FEDERAL RESERVE CHAIR FINALISTS: FT

- VILLEROY AND SIMKUS TRY TO PUSH BACK ON HIKE EXPECTATIONS

- CHINA CPI NEARS TWO-YEAR HIGH IN NOVEMBER

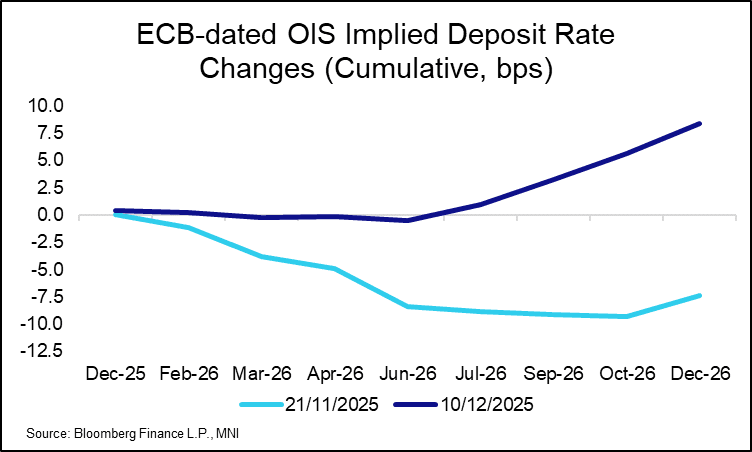

Figure 1: Growing expectations for a ECB rate hike as soon as December 2026

CENTRAL BANK PREVIEWS

MNI FED PREVIEW: Winter of Discontent

The FOMC is expected to look through the data fog and deliver a “hawkish cut” on December 10, with a third consecutive 25bp reduction in the Fed funds rate range to 3.50-3.75%. While a December cut is over 90% priced, a follow-up cut in January is seen as having under 30% probability, and the next easing is only fully priced by next June. There will be the usual attention on the Summary of Economic Projections including the Dot Plot, but more attention than usual on the Statement to see how resolutely the easing bias remains.

MNI BOC PREVIEW: Firm Hold, But Hike Talk Picking Up

The Bank of Canada’s easing cycle looks to be at an end, with markets overwhelmingly expecting a rate hold in December through the subsequent 4 meetings to mid-2026. Firmer-than-expected macroeconomic data since the October meeting has fuelled speculation that the BOC’s next move will be a hike and not a cut, with a 25bp increase fully priced by Q4 2026. With incoming data catching all observers off guard, it leaves open the possibility that the BOC could sound a little more cautious about its current rate stance than it did at the previous meeting, though MNI Markets (and consensus) expects the overall message to remain the same.

MNI SNB PREVIEW: Likely to Remain Neutral

The SNB are expected to keep policy rates unchanged at 0.00%, with a cut back into negative territory highly improbable given inflation has remained within the SNB’s defined range of price stability since June. The rate outlook is likely to continue to be characterized by a high bar to further cuts, with focus on any messaging on how far the Bank are from such a move given inflation undershot the latest Q4 forecasts by almost 0.3pp

MNI BCB PREVIEW: Guidance Focus as Policy Shift Nears

The Copom is widely expected to leave the Selic rate unchanged at 15.00% for a fourth successive meeting on Wednesday, as it remains cautious amid unanchored inflation expectations. However, the very restrictive stance appears to be having the desired effect, with inflation and inflation expectations now declining and economic activity softening. As such, focus will be on the forward guidance and any signals that the Copom is opening the door to a rate cut early next year.

MNI CBRT PREVIEW: Size of Cut in Question

Analysts are split on whether the CBRT will cut the one-week repo rate by another 100bps at its final meeting of the year or accelerate the easing pace to 150bps. Despite a significant downside surprise to headline CPI in November, underlying indicators and consumer inflation expectations remain at uncomfortable levels, which may justify keeping the rate cut pace unchanged at 100bp/meeting, particularly as repricing effects and minimum wage negotiations add uncertainty to the outlook for inflation for 2026.

NEWS

US (FT): Donald Trump to Pit Kevin Hassett Against Trio of Federal Reserve Chair Finalists

Donald Trump will soon launch a final round of interviews for Federal Reserve chair, pitting White House economic adviser Kevin Hassett against a trio of other candidates to replace Jay Powell. The US president and Treasury secretary Scott Bessent are scheduled to meet former Fed governor Kevin Warsh on Wednesday, said three senior administration officials. The officials said Hassett, the director of Trump’s National Economic Council, remains in pole position to succeed Powell as chair in May, despite concerns among some Wall Street investors that he is too close to the president and could cut interest rates too aggressively.

US (WSJ): U.S. Manufacturers Slow Orders Ahead of Supreme Court Tariff Ruling

U.S. manufacturers are pulling back harder on orders of parts and raw materials because of rising uncertainty around the future of the Trump administration's signature tariffs, a new survey shows. Buying activity among North American manufacturers, measured in a global poll of 27,000 businesses by GEP and S&P Market Intelligence, in November hit its lowest level since May. U.S. retailers and manufacturers are waiting for the Supreme Court to rule on the constitutionality of the administration's so-called reciprocal tariffs.

US (WSJ): Massive Debt-Fueled Deals Are Back on Wall Street

The megadeal is back and so is Wall Street’s immense appetite for debt. Paramount’s $77.9 billion bid for Warner—backed by $54 billion in debt—is making some bond investors queasy. Paramount’s hostile bid for Warner Bros. Discovery this week, the leveraged buyout of gaming company Electronic Arts earlier this year and other recent debt-laden transactions have all been possible thanks to a spike in lending by banks and even some private-credit funds.

US/EU (MNI EXCLUSIVE): EU Vote on EU-US Trade Deal to Be Delayed

MNI speaks to Brussels-based sources on pathway for EU/US trade agreement vote. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

ECB (BBG): ECB’s Villeroy Sees No Reason to Raise Interest Rates Soon

The European Central Bank has no reason to raise interest rates soon after probably holding borrowing costs at their current level at a meeting next week, Governing Council member Francois Villeroy de Galhau said. “It would probably be wise to maintain rates at the favorable level they are at currently, while remaining agile and open about future meetings,” the Bank of France chief said on Europe 1 radio, discussing the Dec. 18 policy decision. “As seen today, there is really no reason to envisage a rate increase in the near future, contrary to certain rumors and speculation that may have been heard.”

ECB (BBG): ECB’s Simkus Sees No More Cuts on Surprise Economic Strength

European Central Bank Governing Council member Gediminas Simkus said interest rates don’t need to be lowered further after economic activity and inflation both turned out stronger than expected. Downside risks facing the 20-nation euro area have materialized to a lesser extent than feared, the Lithuanian central-bank chief said Tuesday, citing evidence including a recent upward revision to third-quarter gross domestic product.

ECB (MNI): What Would Macron’s Suggestions Mean for the ECB?

French President Macron has called for a change in the ECB's monetary policy objectives: "it seems to me that European monetary policy can be significantly adjusted today" adding that "Reasserting the value of the European internal market means we can't let inflation be our sole objective, but also growth and employment", he said. What would that mean for interest rates? The ECB currently has a single mandate, "maintaining price stability". Macron's proposals look to align the ECB's mandate closer to the Federal Reserve's, which also optimizes for maximum sustainable employment.

FRANCE (MNI): Gov't Spox Acknowledges State Budget May Not Pass by Year-End

Following the narrow passage of the Social Security Financing Bill (PLFSS) in the National Assembly on 9 Dec (by a margin of 247 to 234 with 93 abstentions), PM Sebastien Lecornu now begins laying the groundwork for achieving a similar feat with the draft State Financing Bill (PLF). The Senate is currently examining the PLF ahead of a vote expected on Monday, 15 December. In the likely event that the Senate and National Assembly pass different versions of the legislation, a joint committee will be convened in an effort to reach a compromise.

UK (The Times): MPs Defy Whip on Brexit With Vote for UK Rejoining Customs Union

More than a dozen Labour MPs have defied the party whips and voted in favour of the UK rejoining a customs union with the European Union. The group, which included Dame Meg Hillier, the influential chair of the Treasury select committee, backed the Liberal Democrat motion in the Commons despite calls from party managers to abstain from the vote. As a result, the Liberal Democrat Ten-Minute Rule Bill passed the Commons with a majority of one, after the deputy Speaker cast the deciding vote in its favour.

GERMANY (MNI): Economy Minister Pushing for Earlier Lowering of Corporation Tax

German economy minister Reiche (CDU) is supporting demands from the influential Bavaria PM Söder (CSU) on pulling forward the planned lowering (to 10% from 15%, in stages) in corporation tax from January 2028 to July 2026. "Given the serious situation in the German economy, we should examine whether earlier entry into force is possible", Reiche says, but also cautioned that before any decision is made, public budgets must be examined to determine the necessary scope for action.

EU/UKRAINE (FT): EU Races to Bypass Viktor Orbán on Russian Assets Before Summit

EU countries are to fast-track a decision to indefinitely immobilise up to €210bn in Russian sovereign assets, in an attempt to bypass Hungary’s Prime Minister Viktor Orbán even before Europe’s leaders meet for a summit next week. The hurried effort to pass the legislation — which invokes emergency powers to override national vetoes on the extension of sanctions — aims to protect Brussels’ leverage in US-led peace talks over the war in Ukraine, according to officials familiar with the plans.

UKRAINE (WaPo): After Trump Criticism, Zelensky Says He’s Ready to Hold Elections

Ukrainian President Volodymyr Zelensky has asked members of his political party to prepare legislation to hold elections despite the country's war with Russia, he said Tuesday, contingent on the United States and Europe providing security guarantees. The comments, a sharp reversal of his long-held position that voting is impossible under martial law, came hours after new criticism from President Donald Trump.

CHINA (MNI EXCLUSIVE): China to Boost Foreign Participation in Services

MNI discusses Beijing's plans to expand foreign investment in the services sector. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI): IMF Revises China GDP Growth Forecast Upwards

MNI (Beijing) The IMF has revised its China GDP growth projection upwards to 5.0 percent in 2025 and 4.5 percent in 2026, 0.2 and 0.3 percentage points higher than the previous estimate from October, a country mission report from the fund said on Wednesday, with the uptick driven by macroeconomic policy measures and lower-than-expected tariffs on exports.

CHINA (FT): China Adds Domestic AI Chips to Official Procurement List for First Time

China has put domestic artificial intelligence chips on an official procurement list for the first time, bolstering the nation’s tech sector ahead of US President Donald Trump’s move to allow Nvidia exports to the country. The Ministry of Industry and Information Technology recently added AI processors from Chinese groups, including Huawei and Cambricon to its government-approved list of suppliers, according to two people familiar with the matter.

DATA

NORWAY DATA (MNI): No Massive Surprises in Nov CPI-ATE Report, Services Still Sticky

- NORWAY NOV CPI +0.1% M/M, +3.0% Y/Y

- NORWAY NOV CPI-ATE -0.3% M/M, +3.0% Y/Y

Overall, the Norwegian November inflation report did not contain much to push Norges Bank off its previously signalled cautious easing path. Although underlying CPI-ATE momentum is likely to ease in the coming months, services inflation remains too sticky for comfort. Focus turns to the Q4 Regional Network Survey tomorrow. On a seasonally adjusted basis using Stats Norway data, Norwegian CPI-ATE inflation rose 0.15% M/M. That follows 0.45% M/M last month and 0.15% the two months prior. 3m/3m annualised momentum was essentially unchanged at 2.81%, but recent sequential readings suggest a moderation is likely in the coming months.

CHINA DATA (MNI): China November CPI Near Two-Year High

- CHINA NOV CPI +0.7% Y/Y VS MEDIAN +0.7%; OCT +0.2%: NBS

China’s Consumer Price Index rose 0.7% y/y in November, up from October's 0.2% growth to hit the highest level since March 2024, in line with expectations for a 0.7% gain, according to data from the National Bureau of Statistics released Wednesday. The y/y increase was mainly driven by rising food prices. On a monthly basis, CPI fell 0.1%, reversing October's 0.2% growth, mainly due to the seasonal decline in service prices. Core CPI, which excludes food and energy, rose 1.2%, flat from October's 1.2%, marking the third consecutive month to be above 1%.

JAPAN DATA (MNI): Corporate Goods Price Index Rise 2.7% Y/Y in Nov; Import Price Drops

- JAPAN NOV CORP GOODS PRICE INDEX +2.7% Y/Y; OCT +2.7%

- JAPAN NOV CORP GOODS PRICE INDEX +0.3% M/M; OCT +0.5%

Japan’s corporate goods price index rose 2.7% y/y in November, unchanged from October’s revised 2.7%, while import prices fell for a 10th straight month, Bank of Japan data showed Wednesday. The index was lifted by nonferrous metals (+14.9% vs. +11.8%), while electric power, gas and water (-1.0% vs. -0.6%) dragged it down. CGPI rose 0.3% m/m, the third consecutive gain after a revised +0.5% in October. Import prices on a yen basis dropped 1.8% y/y after -1.7% in October, underscoring the limited pass-through of yen weakness.

FOREX: USDJPY Momentum Stalls Short of 157.00 Handle Ahead of FOMC

- USDJPY momentum stalled on the run-up to 156.95 yesterday, as a EUR-led phase of USD selling across early Europe contained any broader dollar rally. Downward pressure on the JPY continues to be a focus this week, amid the hawkish repricing for core fixed income markets and regional geopolitical uncertainty taking its toll. Key resistance for USDJPY remains at 157.89, the Nov 20 high and bull trigger. Despite a slightly weaker risk backdrop today, cross/JPY remains a notable beneficiary of the overall dynamics.

- The next key driver for the greenback will be today's FOMC, with more attention than usual on the Statement to see how resolute any remaining easing bias is. Forward guidance is likely to be amended to reflect a more patient stance on cuts. As such, the market reaction to the meeting could hinge on how Chair Powell portrays the burden of proof for further easing ahead.

- EURUSD meanwhile has seen an 1.1658 overnight high before this morning’s ECBspeak reaffirmed the idea that the Governing Council deems rates to be “in a good place”, despite Executive Board member Schnabel expressing her comfort with markets pricing the next rate move as a hike earlier in the week.

- Initial resistance comes in at the 50% retracement of the Sep17-Nov 5 bear leg (1.1694), while support is located at the 20-day EMA intersecting at 1.1607. A French Gov't spokesperson acknowledged this morning the 2026 budget may not pass by year-end in the country - further pessimism here despite yesterday's narrow passage of the Social Security Financing Bill would pressure EUR from here.

- Weekly MBA mortgage applications and the Q3 employment cost index are on the calendar ahead of the FOMC. Australian labour market data is scheduled overnight.

EGBS: Bund Futures Off Lows, But Bearish Pressure Still Dominant

Bund futures have moved away from session lows but bearish momentum remains dominant and volumes are elevated. Bunds are -31 ticks at 127.22, having fallen sharply to 127.05 this morning. Round number support at 127.00 is untested for now.

- Front-end repricing remains the key driver, with ECB-dated OIS now longer pricing any implied probability of a cut next year, with 11.5bps of hikes now priced through December 2026. That’s despite some pushback against the idea of hikes from ECB’s Villeroy and Simkus this morning.

- The German curve is bear flatter again, with 5-year yields up over 4bps and 30-year yields up 2bps. That sees 5s30s flatten 96.7bps, the lowest since the end of October. We note that flattening impulses at the long-end may represent an unwind of Dutch pension fund transition-related positions.

- 10-year Bund yields are up 3bps to 2.88%, with the 2.90% figure presenting an important topside level to watch.

- 10-year EGB spreads to Bunds are up to 2bps wider, with BTPs and OATs underperforming. Continued increases in EUR rates vol may be filtering into spreads. OAT price action comes despite the National Assembly passing the 2026 Social Security budget yesterday.

- Italian October IP was weaker-than-expected at -1.0% M/M (vs 0.2% cons).

- This afternoon’s focus is the BOC and Fed decisions.

GILTS: Under Pressure on Hawkish EUR Cues, Recent Lows in Futures Intact

Ongoing extension of the hawkish repricing in the short end of the EUR curve has weighed on gilts this morning. 5s and 10s register fresh month-to-date highs in yields.

- Futures -64 at 90.79. Initial support and resistance located at 90.62 & 91.29, respectively. Bears have negated much of the recent bullish move.

- A reminder that we have suggested that post-Budget movement in OI in futures doesn’t point to the establishment of a meaningful number of high conviction longs since that event, despite the market apparently deeming Chancellor Reeves’ fiscal consolidation to be credible.

- Risks surrounding the backloaded nature of the fiscal consolidation that was outlined in the Budget may be key here, albeit with the cash curve flattening as the DMO continues to skew issuance away from the long end.

- Yields 3-4bp higher across the curve. 5s under the most pressure.

- Gilt bulls are still unable to force the gilt/Bund spread below 165bp on a sustained basis.

- Little of note for markets to trade off as Chancellor Reeves is questioned by the Treasury Select Committee on the Budget and leaks leading up to the event.

- 4.75% Oct-35 gilt auction passes smoothly.

- SONIA futures flat to -6.0, strip steepens. SFIZ6 & Z7 trade to fresh multi-week lows.

- BoE-dated OIS still prices ~22bp of easing for this month’s decision, we look for a cut at that event.

- Terminal rate pricing ~3.45% after threatening a move below 3.30% in recent weeks.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.756 | -21.8 |

Feb-26 | 3.700 | -27.4 |

Mar-26 | 3.631 | -34.3 |

Apr-26 | 3.544 | -43.0 |

Jun-26 | 3.512 | -46.3 |

Jul-26 | 3.461 | -51.3 |

Sep-26 | 3.456 | -51.8 |

Oct-26 | 3.449 | -52.5 |

Dec-26 | 3.453 | -52.1 |

Feb-27 | 3.470 | -50.4 |

EQUITIES: Bull Cycle in E-Mini S&P Intact, Contract Still Above 20-, 50-Day EMAs

A bull cycle in Eurostoxx 50 futures remains intact and the contract is trading closer to its recent highs. Price has cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next (pierced), 76.4% of the Nov 13 - 21 bear leg. A clear breach of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support to watch lies at 5629.92, the 50-day EMA. A bull cycle in S&P E-Minis remains intact and price continues to trade above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6807.02, the 20-day EMA.

- Japan's NIKKEI closed lower by 52.3 pts or -0.1% at 50602.8 and the TOPIX ended 4.1 pts higher or +0.12% at 3389.02.

- Elsewhere, in China the SHANGHAI closed lower by 9.025 pts or -0.23% at 3900.496 and the HANG SENG ended 106.55 pts higher or +0.42% at 25540.78.

- Across Europe, Germany's DAX trades lower by 86.4 pts or -0.36% at 24076.12, FTSE 100 higher by 11.71 pts or +0.12% at 9653.42, CAC 40 down 20.87 pts or -0.26% at 8032.16 and Euro Stoxx 50 down 9.49 pts or -0.17% at 5709.02.

- Dow Jones mini up 9 pts or +0.02% at 47622, S&P 500 mini up 4.25 pts or +0.06% at 6852.5, NASDAQ mini up 6.75 pts or +0.03% at 25706.5.

Time: 10:00 GMT

COMMODITIES: Gold in Consolidation Mode, Trend Remains Bullish Overall

Short-term gains in WTI futures appear corrective - for now - and a bear threat remains present. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A stronger resumption of the bear leg would open key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. Gold is in consolidation mode. The trend condition is unchanged, the set-up remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4044.0. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude down $0 or 0% at $58.27

- Natural Gas down $0.02 or -0.33% at $4.557

- Gold spot down $14.42 or -0.34% at $4193.27

- Copper up $7.7 or +1.45% at $539.75

- Silver up $0.24 or +0.4% at $60.8945

- Platinum down $20.84 or -1.23% at $1671.97

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 10/12/2025 | 1055/1155 | ECB Lagarde Interview on Currencies/Digital Euro | ||

| 10/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 10/12/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 10/12/2025 | - | *** | Money Supply | |

| 10/12/2025 | - | *** | Social Financing | |

| 10/12/2025 | - | *** | New Loans | |

| 10/12/2025 | 1330/0830 | *** | Employment Cost Index | |

| 10/12/2025 | 1445/0945 | *** | Bank of Canada Policy Decision | |

| 10/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/12/2025 | 1530/1030 | BOC press conference | ||

| 10/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 10/12/2025 | 1900/1400 | ** | Treasury Budget | |

| 10/12/2025 | 1900/1400 | *** | FOMC Statement | |

| 10/12/2025 | 1930/1430 | Fed Chair Powell Press Conference | ||

| 11/12/2025 | - | Swiss National Bank Meeting | ||

| 11/12/2025 | 0001/0001 | * | RICS House Prices | |

| 11/12/2025 | 0030/1130 | *** | Labor Force Survey | |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0830/0930 | *** | SNB Interest Rate Decision | |

| 11/12/2025 | 0950/0950 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 11/12/2025 | 1000/1000 | BOE Bailey Gives Evidence At Covid-19 Inquiry | ||

| 11/12/2025 | 1100/0600 | *** | Turkey Benchmark Rate | |

| 11/12/2025 | - | ECB Lagarde and Cipollone at Eurogroup Meeting | ||

| 11/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 11/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 11/12/2025 | 1330/0830 | * | Household Debt-to-Income | |

| 11/12/2025 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1500/1000 | * | Services Revenues | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 11/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/12/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond |