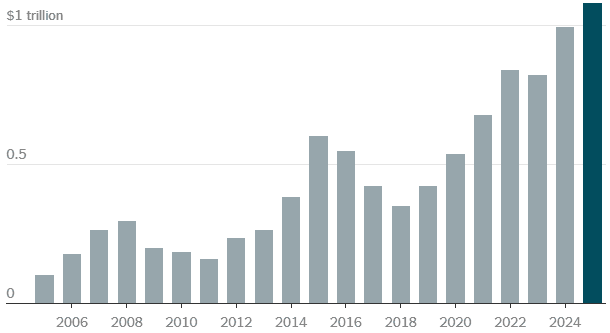

MNI US OPEN - China Trade Surplus Exceeds $1tn for First Time

EXECUTIVE SUMMARY

- MNI RBA PREVIEW: ON HOLD, COULD BE A HAWKISH SHIFT?

- ECB’S SCHNABEL SAYS SHE’D BE ‘READY’ TO SUCCEED LAGARDE IF ASKED

- CHINA TO ADOPT MORE PROACTIVE POLICIES – POLITBURO

- CHINA'S EXPORTS JUMP 5.9% Y/Y IN NOVEMBER; REBOUND FROM 8-MONTH LOW

Figure 1: China’s annual trade surplus exceeds $1tn

Note: Data for 2025 includes the first 11 months of the year

Source: The New York Times, China General Administration of Customs, FactSet

NEWS

MNI RBA PREVIEW: On Hold, Could Be A Hawkish Shift?

With October trimmed mean inflation printing at 3.3%, the RBA is unanimously expected to be on hold at its December meeting. The strength of the data since the November meeting plus inflation rising further above the top of the band increases the chance that the RBA now sees risks skewed to the upside and as a result it may sound more hawkish and at a minimum will remain “cautious”. RBA-dated OIS pricing is showing the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

ECB (BBG): ECB’s Schnabel Says She’d Be ‘Ready’ to Succeed Lagarde If Asked

European Central Bank Executive Board member Isabel Schnabel said she’d be willing to take over as president when Christine Lagarde’s term ends in less than two years. Asked about views that it’s time for a German to lead the ECB and whether she could be that person, Schnabel said in an interview that “if I was asked, I would stand ready.” Current front-runners for the role are thought to include former Dutch central-bank chief Klaas Knot, Spain’s Pablo Hernandez de Cos, who currently leads the Bank for International Settlements, and Bundesbank President Joachim Nagel.

ECB (BBG): ECB’s Schnabel ‘Comfortable’ on Bets Next Move Will Be Hike

Executive Board member Isabel Schnabel is comfortable with investor bets that the European Central Bank’s next interest-rate move will be an increase. While borrowing costs are at levels that — barring further shocks — will be appropriate for some time, consumer spending, business investments and a jump in government outlays on defense and infrastructure will bolster the economy, Schnabel said.

ECB (BBG): Macron Calls for Rethink on ECB Approach to Monetary Policy

French President Emmanuel Macron called for a change in approach to monetary policy at the European Central Bank to boost the single market and protect it from the risks of financial crisis. In an unusual move by a euro-zone leader to comment on the region’s central bank, Macron said in an interview with Les Echos the ECB needs to think differently if the European Union wants to capitalize on its strengths such as its domestic market and high savings rate.

US/RUSSIA/UKRAINE (BBG): Trump Voices Disappointment in Zelenskiy as Peace Talks Drag

President Donald Trump said he’s disappointed in Ukrainian President Volodymyr Zelenskiy’s handling of a US proposal to end the war that began with Russia’s full-scale invasion. Trump’s tone on Ukraine contrasted with comments in recent days about President Vladimir Putin’s reaction to the proposal. The US said Friday its negotiators had agreed with Kyiv on a “framework of security arrangements” and discussed what deterrence capabilities were needed as part of a deal to end the war with Russia. However, there was little indication of a major breakthrough.

US/CANADA (BBG): Trump Says ‘We’ll See’ on Restarting Canada Trade Talks

President Donald Trump says “we’ll see” when asked about whether he will restart the trade negotiations with Canada. “We will work it out,” he added. “I have a great relationships with Canada, with the prime minister.”

US (BBG): Trump to Unveil $12 Billion in Long-Awaited Farm Aid Program

The Trump administration on Monday plans to unveil a long-awaited farm aid package, according to a White House official, offering $12 billion in assistance to a key base of support hit hard by low crop prices and the impact of the president’s tariff policies. The aid will include up to $11 billion in one-time payments to crop farmers under the Department of Agriculture’s newly designed Farmer Bridge Assistance program, while the remaining is reserved for crops not covered under the FBA, according to the official, who asked not to be identified as the information isn’t public.

US (WSJ): Trump Tasks Top Advisers With Finding Way to Lower Soaring Beef Prices

A group of President Trump's top advisers have convened to tackle soaring beef prices, according to people familiar with the discussions, showing how the administration is escalating efforts to wrangle food inflation. Steak and ground beef have hit record highs this year, sending everyone including meatpackers, supermarkets and restaurants looking for ways to ease the pain.

US (BBG): Trump Warns Netflix-Warner Deal May Pose Antitrust ‘Problem’

US President Donald Trump raised potential antitrust concerns around Netflix Inc.’s planned $72 billion acquisition of Warner Bros. Discovery Inc., noting that the market share of the combined entity may pose problems. Trump’s comments, made as he arrived at the Kennedy Center for an event on Sunday, may spur concerns regulators will oppose the coupling of the world’s dominant streaming service with a Hollywood icon. The company faces a lengthy Justice Department review of a deal that would reshape the entertainment industry.

EU/UKRAINE (MNI): EU PMs Urge Quick Deal on Reparation Loan

The prime ministers of Finland, Poland, Sweden, Ireland and the three Baltic states have written to European Union President Antonio Costa and European Commission President Ursula von der Leyen urging an agreement on the Ukraine reparation loan proposal at the upcoming EU summit. The seven leaders say a loan based on immobilised Russian assets is the "most financially feasible and politically realistic solution, it addresses the fundamental principle of Ukraine’s right to compensation for damages caused by the aggression."

UK (The Times): Labour Group That Backed Starmer Canvasses Party on Leadership Candidates

The influential think tank that ran Sir Keir Starmer’s leadership campaign is canvassing party members on candidates to replace him. In the clearest sign yet that the Labour Party is preparing for a change of prime minister, Labour Together, the campaign group once run by Morgan McSweeney, Starmer’s chief of staff, this weekend asked activists for their views on contenders for the leadership. A survey sent to local Labour parties, seen by The Times, prompted members to name the politicians who stood “the best chance of leading Labour to electoral victory at the next general election” compared with Starmer and to rank those they would be likely to vote for in a leadership election.

CHINA (MNI): China to Adopt More Proactive Policies - Politburo

MNI (Beijing) China will continue to implement a more proactive fiscal policy and moderately loose monetary policy, increase counter- and cross-cyclical adjustments, and improve the efficiency of macroeconomic governance, Xinhua News Agency reported Monday following the Politburo meeting in Beijing. Authorities should better coordinate domestic economic work and international trade struggles, and implement more proactive macroeconomic policies and enhance their forward-looking, targeted, and coordinated nature, the meeting said, noting the key to expanding domestic demand and optimising supply.

BOJ (MNI EXCLUSIVE): BOJ Unshaken by JGB Volatility

MNI discusses the BOJ's stance on recent JGB yield moves. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA

GERMANY DATA (MNI): IP Starts Off Q4 on Comparably Strong Note

- GERMANY OCT IND PROD +1.8% M/M, +0.8% Y/Y (VS +1.1% M/M, -1.4% Y/Y SEP)

German industrial production was stronger than expected in October, even considering the downward September revision. "The less volatile three-month on three-month comparison showed that production was 1.5% lower in the period from August 2025 to October 2025 than in the previous three months [...] In October 2025, production in industry excluding energy and construction was up 1.5% [M/M] from September 2025 after seasonal and calendar adjustment."Destatis comments.

UK DATA (MNI): KPMG-REC Report Continues to Point to Slack in Labour Market

Big picture, permanent placements continue to decline, salary increases remain subdued by historical standards and availability of staff picked up . But there seems to be something for everyone in the details. The biggest red flag for us is the availability of staff index picking up at the second-fastest rate since November 2020. The index remains in the mid 60s as it has since March (except a tick up in August). This indicates that slack continues to increase in the labour market. In contrast, permanent placements showed their smallest reduction in five months. But they too remained in contractionary territory.

CHINA DATA (MNI): China's Nov Exports +5.9%; Rebound From 8-month Low

- CHINA NOV TRADE SURPLUS +$111.68 BLN VS MEDIAN +$103.3 BLN

- CHINA NOV EXPORTS +5.9% Y/Y VS MEDIAN +4.0% Y/Y

- CHINA NOV IMPORTS +1.9% Y/Y VS MEDIAN +2.9% Y/Y

MNI (Sydney) China's exports registered a 5.9% increase in November, while imports rose 1.9%, data released by China Customs showed on Monday. Exports in November rose 5.9% y/y to USD330.4 billion, quickly rebounding from the previous 1.1% drop and beating the expectations for a 4.0% increase. Imports gained 1.9% y/y, quicker from 1.0% in October and behind the 2.9% market consensus. China’s trade surplus in November hit USD111.7 billion, larger than the consensus of USD103.3 billion, taking Jan-Nov’s final surplus to USD1.08 trillion.

JAPAN DATA (MNI): Japan's Q3 GDP Revised Down on Capex

- JAPAN Q3 ANNUALIZED GDP REV -2.3%; PRELIM -1.8%; MEDIAN -2.2%

- JAPAN Q3 GDP REV -0.6% Q/Q; PRELIM -0.4%; MEDIAN -0.5%

Japan's Q3 GDP fell 0.6% q/q, or an annualised -2.3%, compared with the initial estimate of -0.4% q/q, or -1.8% annualised, as capital investment and public spending were revised down, although private consumption was revised slightly higher, second preliminary GDP data from the Cabinet Office showed Monday. Private consumption, which accounts for about 60% of Japan’s GDP, was revised up to 0.2% from 0.1%, though its contribution remained unchanged at 0.1 pp. Capital investment dropped 0.2% q/q, a sharp downward revision from the preliminary +1.0%. Its contribution was revised to -0.0 pp from +0.2 pp.

JAPAN DATA (MNI): Japan's Oct Negative Real Wages Narrow

Inflation-adjusted real wages, a barometer of households’ purchasing power, remained in negative territory for the 10th straight month in October, falling 0.7% after a 1.3% drop in September, preliminary data from the Ministry of Health, Labour and Welfare showed Monday. The figures indicate wages are still failing to keep pace with inflation, leaving households under pressure from high living costs. However, the pace of decline narrowed, suggesting real wages are gradually moving toward positive territory as year-on-year CPI gains are expected to slow due to government measures.

JAPAN DATA (MNI): Japan Nov Sentiments Post 1st Drop in 7 Months

Japan’s Economy Watchers sentiment index fell for the first time in seven months in November, with the outlook index for two to three months ahead also posting its first decline in seven months, although the government kept its overall assessment unchanged, data from the Cabinet Office showed Monday. Indexes covering households, the labour market and businesses all weakened. The current conditions index declined to a seasonally adjusted 48.7 in November from 49.1 in October, while the outlook index dropped 2.8 points to 50.3 from 53.1.

RATINGS: Affirmations & Outlook Tweaks on Friday

Sovereign rating reviews of note from after hours on Friday include:

- Fitch affirmed Austria at AA; Outlook Stable

- Fitch affirmed Hungary at BBB; Outlook revised to Negative

- S&P affirmed Malta at A-; Outlook Stable

- Morningstar DBRS confirmed Austria at AAA, Negative Trend

- Morningstar DBRS confirmed Estonia at AA (low), Stable Trend

- Morningstar DBRS confirmed Hungary at BBB, Stable Trend

FOREX: AUD and CAD Consolidating Gains Ahead of Central Bank Decisions

- G10 currency markets are trading with moderate adjustments Monday, as markets digest increasing China/Japan tensions over the weekend and await a busy calendar of central bank decisions ahead. Despite US yields continuing to edge higher, the USD index holds close to unchanged, hovering within 20 pips of the recent pullback lows.

- EURUSD was given a brief boost in early trade, matching its 1.1672 Friday high after ECB Executive Board member Schnabel noted that she is “rather comfortable” with markets pricing the next move from the ECB as a hike. The recent break above 1.1656 in EURUSD highlighted a potential reversal, although topside momentum has failed to immediately gain traction.

- JPY meanwhile is a modest underperformer after Chinese military aircraft breached Japanese airspace and Q3 Japanese GDP was downwardly revised. Moves have been contained, with USDJPY broadly remaining in a 155.00/50 range as verbal jawboning from Finmin Katayama somewhat offsets the yen pessimism.

- AUDUSD traded up to 0.6649 overnight and the subsequent dip as remained very shallow. This follows 10 consecutive sessions of higher highs as we approach tomorrow’s RBA decision. With a hold tomorrow widely expected, the tone of the statement and press conference will be scrutinised given the recent increase of hike pricing in 2026.

- Elsewhere, NZDUSD has been edging closer to the medium-term pivot at the 0.5800 mark, while USDCAD is holding the entirety of its post-data plunge from Friday. Technical developments have significantly bolstered the bearish USDCAD theme, following a breach of the bull channel and clean break of 1.3888.

- NY Fed inflation expectations is the main datapoint for today, while ECB's Cipollone and Villeroy as well as BoE's Taylor and Lombardelli are scheduled to speak.

EGBS: 10-year Bund Yields Push Through 2.80% as Hawkish ECB Repricing Persists

10-year Bund yields have pushed through the 2.80% figure to trade at the highest since March, now up over 3bps today. Hawkish repricing at the front-end has pulled yields higher across the curve, following a Bloomberg interview with ECB’s Schnabel and a solid German IP reading. Recent momentum suggests risks remain skewed in favour for further upside in yields.

- The short-end driven nature of recent moves has allowed the German 5s30s curve to flatten away from multi-week highs, currently -1.3bps today at 101.4bps. On the domestic front, focus remains on Germany’s 2026 issuance plan, which we expect to be released next week.

- Bund futures are -40 ticks at 127.75, on track for a seventh consecutive negative session. A bear cycle remains intact, with next support at 127.57, a Fibonacci projection. Options flow across the curve has been clearly skewed towards further downside.

- 10-year EGB spreads to Bunds are biased up to 1bp wider, a function of fading ECB rate cut expectations and an uptick in EUR rates vol. The BTP/Bund spread nonetheless remains below 70bps.

- Schnabel noted that she was “rather comfortable” with market expectations that “the next rate move is going to be a hike, albeit not anytime soon”. Although not too surprising given her hawkish stance, the remarks are being interpreted as a further signal that another cut is unlikely, viewed alongside sticky (core) inflation data, improving PMIs and a stronger-than-expected Q3 compensation per employee reading.

- Meanwhile, German October industrial production was stronger-than-expected at 1.8% M/M (vs 0.3% cons and a downwardly revised 1.1% prior).

- This week’s Eurozone calendar is reasonably light, with broader global focus on Wednesday's FOMC decision.

GILTS: Futures Hover Above Support After Sell Off, Hawkish Move in SONIA

Gilts sell off on bearish cues from EGBs in the wake of some typically hawkish remarks from ECBs Schnabel and firming wage indications in the latest REC report on jobs

- Futures trade as low as 90.88, basing just above the December 2 low (90.87).

- Bullish short-term technicals remain intact despite today’s sell off.

- Fresh extension lower would target the November 25 low (90.53), while resistance comes in at the November 27 high (91.93).

- Yields 3-4bp higher, 5- to 10-Year zone leads the weakness.

- Gilt/Bund spread little changed around 168bp.

- Gilt outperformance vs. Bunds stalled around the 165bp level last week, after the spread tightened by ~25bp since November 12.

- The speed of the tightening, coupled with ongoing medium-term UK fiscal fisks, have been cited as limiting factors by some.

- BoE-dated OIS still pricing over 80% odds of a December rate cut.

- SONIA futures flat to -5.0. Terminal rate pricing 3.42% after trading between 3.30-3.35% for much of last week. November lows in SFIZ6 (96.550) remain untested.

- Comments are due from BoE's Taylor (17:00) & Lombardelli (18:30), although the topics of their addresses may limit the scope for comments on monetary policy.

- Further out, UK monthly economic activity data is due Friday.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.758 | -21.5 |

Feb-26 | 3.692 | -28.1 |

Mar-26 | 3.620 | -35.3 |

Apr-26 | 3.528 | -44.5 |

Jun-26 | 3.484 | -48.9 |

Jul-26 | 3.425 | -54.8 |

Sep-26 | 3.416 | -55.7 |

EQUITIES: Bull Cycle in Eurostoxx 50 Futures Remains Intact

A bull cycle in Eurostoxx 50 futures remains intact. Price has recently cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next (pierced), the 76.4% retracement of the Nov 13 - 21 bear leg. Clearance of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support lies at 5621.75, the 50-day EMA. A bullish theme in S&P E-Minis is intact. Price remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6797.09, the 20-day EMA.

- Japan's NIKKEI closed higher by 90.07 pts or +0.18% at 50581.94 and the TOPIX ended 21.75 pts higher or +0.65% at 3384.31.

- Elsewhere, in China the SHANGHAI closed higher by 21.27 pts or +0.55% at 3924.078 and the HANG SENG ended 319.72 pts lower or -1.23% at 25765.36.

- Across Europe, Germany's DAX trades higher by 47.21 pts or +0.2% at 24074.68, FTSE 100 higher by 1.69 pts or +0.02% at 9668.82, CAC 40 down 13.07 pts or -0.16% at 8101.67 and Euro Stoxx 50 up 3.01 pts or +0.05% at 5726.94.

- Dow Jones mini down 0 pts or 0% at 48001, S&P 500 mini up 7 pts or +0.1% at 6885.25, NASDAQ mini up 41.75 pts or +0.16% at 25774.

Time: 10:00 GMT

COMMODITIES: WTI Future Moving Average Studies in a Bear-Mode Position

Short-term gains in WTI futures appear corrective - for now. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend needle in Gold continues to point north. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4031.1. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude down $0.4 or -0.67% at $59.67

- Natural Gas down $0.2 or -3.8% at $5.087

- Gold spot up $11.02 or +0.26% at $4208.61

- Copper down $0.65 or -0.12% at $545.5

- Silver up $0.09 or +0.15% at $58.4193

- Platinum up $15.99 or +0.97% at $1659.2

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 08/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/12/2025 | 1500/1600 | ECB Cipollone Lecture at Frankfurt School of Finance & Management | ||

| 08/12/2025 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/12/2025 | 1700/1700 | BOE Taylor Panel on Growth/Wealth/Debt | ||

| 08/12/2025 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/12/2025 | 1830/1830 | BOE Lombardelli Panel on Women in Economics | ||

| 09/12/2025 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 09/12/2025 | 0330/1430 | *** | RBA Rate Decision | |

| 09/12/2025 | 0700/0800 | ** | Trade Balance | |

| 09/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 09/12/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 09/12/2025 | - | FOMC Meetings with S.E.P. | ||

| 09/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 09/12/2025 | 1415/1415 | BOE Lombardelli, Ramsden, Dhingra, Mann at TSC | ||

| 09/12/2025 | 1500/1000 | *** | JOLTS Jobs Opening Level | |

| 09/12/2025 | 1500/1000 | *** | JOLTS Quits Rate | |

| 09/12/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/12/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result |