MNI US OPEN - BoE Pricing Pressured on Soft UK Jobs Data

EXECUTIVE SUMMARY

- TRUMP SAYS CHINA ‘NOT EASY’ AS TRADE TALKS TO RESUME TUESDAY

- MARINES ARE DEPLOYING TO L.A. AREA IN WAKE OF ICE PROTESTS

- BOJ'S UEDA SEES LIMIT TO BOOST ECONOMY VIA EASING

- UK WAGE AND PAYROLLS DATA SOFT

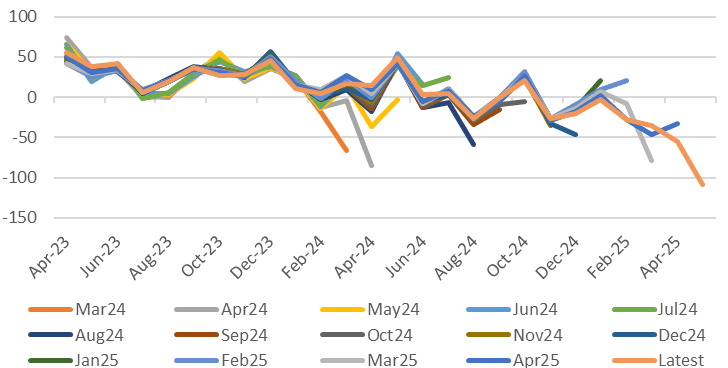

Figure 1: HMRC monthly change in payrolls (by release dates)

Source: MNI/ONS

NEWS

US/CHINA (BBG): Trump Says China ‘Not Easy’ as Trade Talks to Resume Tuesday

Trade talks between the US and China will continue into a second day, according to a US official, as the two sides look to ease tensions over shipments of technology and rare earth elements. Representatives for both nations ended their first day of negotiations in London after more than six hours at Lancaster House, a 19th century mansion near Buckingham Palace. The talks concluded around 8 p.m. London time. The advisers will meet again Tuesday at 10 a.m. in the British capital, the official said. “We are doing well with China. China’s not easy,” Trump told reporters at the White House on Monday. “I’m only getting good reports.”

US (WSJ): Marines Are Deploying to L.A. Area in Wake of ICE Protests

Roughly 700 Marines are deploying to the Los Angeles area to protect federal buildings and personnel in the wake of protests over immigration that have already led President Trump to federalize National Guard troops, the U.S. military said Monday. The troops, which are assigned to the 2nd Battalion, 7th Marines, 1st Marine Division out of Twentynine Palms, Calif., won’t engage with protesters, U.S. Northern Command, which is responsible for U.S. military operations in North America, said in a statement. A senior administration official told reporters on Monday evening that the move came in light of increased threats against federal officers and federal buildings.

US/IRAN (MNI): Sixth Round of Talks w/ US Planned for 15 June

The Iranian Foreign Ministry is reporting that a sixth round of indirect talks between Iran and the US will take place in the Omani capital, Muscat, on Sunday, 15 June. This would appear to counter US President Donald Trump's comments from 9 June suggesting that a meeting would take place on Thursday, 12 June. Asked by reporters whether Iran had submitted a counterproposal to the initial US proposal, Trump called Iran "tough" negotiations, adding, "We have a meeting with Iran on Thursday, so we're going to wait until Thursday."

ECB (BBG): ECB Still Agile After Reaching ‘Favorable Zone,’ Villeroy Says

The European Central Bank could still move quickly to adjust interest rates even after an eighth successive cut “normalized” monetary policy, according to Governing Council member Francois Villeroy de Galhau. “Since last Thursday, we have been in the favorable ‘2 and 2’ zone, with inflation forecast at 2% this year – which is our target – and our key rate at 2%,” the French official told a Europlace conference in Paris on Tuesday. “But in such an uncertain environment, this favorable zone does not mean a comfortable zone or a static zone: We will remain pragmatic and data-driven, and as agile as necessary.”

FRANCE (BBG): France’s Macron Doesn’t Rule Out Calling Snap Elections Again

French president Emmanuel Macron said he doesn’t rule out the possibility of again dissolving the National Assembly and calling snap elections. “My wish is that there’s not another dissolution but I’m not used to depriving myself of a constitutional power,” he said Monday in response to a reporter’s question on whether he had excluded the possibility of taking such an unusual step. France’s President Emmanuel Macron speaks during the United Nations Ocean Conference in Nice, France, on June 9. Speaking to the press in the southern city of Nice after addressing a United Nations summit on protecting the oceans, the French leader said he could potentially deploy that authority if political parties decided to have a “totally irresponsible approach and block the country.” Up to now, he has publicly said that early elections weren’t under consideration.

UK (BBG): UK Green-Lights £14 Billion for Sizewell C Nuclear Plant

The UK will invest £14.2 billion ($19.2 billion) to help build the Sizewell C nuclear plant, saying the reactor will help deliver “a golden age” of abundant clean energy. The proposed plant in Suffolk has been on the drawing board for more than a decade, and the funding announced Tuesday comes on top of billions of pounds already pledged during its development. The eventual price tag for construction may surpass £40 billion.

BOJ (MNI): BOJ's Ueda Sees Limit to Boost Economy Via Easing

The Bank of Japan has limited room to stimulate the economy via policy rate, currently 0.5%, cuts if growth comes under pressure, Governor Kazuo Ueda told lawmakers Tuesday. Underlying inflation still has some way to go before reaching the 2% target, Ueda said, emphasising that the BOJ's priority is to firmly anchor inflation at that level. He added that financial conditions will remain accommodative until the target is achieved, but the central bank will consider raising interest rates if the probability of underlying inflation reaching 2% increases.

JAPAN (BBG): Japan’s Ishiba Pledges 50% Pay Rise by 2040 Ahead of Elections

Japanese Prime Minister Shigeru Ishiba has set pay raises and a ¥1 quadrillion ($6.9 trillion) economy as the top campaign promises for this summer’s upper house election, as the date nears for voters to give their latest verdict on his administration. “I’ve instructed senior party officials to make our top election pledge an aim to reach ¥1 quadrillion in nominal GDP by 2040 and increase average pay by 50% or more from its current level,” Ishiba told reporters in Tokyo Monday evening.

CHINA (MNI INTERVIEW): China to Stabilise Manufacturing's Share of GDP

MNI speaks to the president of China Manufacturing Think Tank about the country's next five-year plan - On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (BBG): China Taps $1.5 Trillion Fund to Boost Home Market Support

China is tapping an often overlooked pool of funds worth 10.9 trillion yuan ($1.5 trillion) to salvage its housing sector, offering people an alternative to bank mortgages. The housing provident fund, a government savings program used to help people buy homes, has become an increasingly important means to obtain financing, as banks turn more cautious with profit challenges. The fund has outpaced banks in giving out loans, hitting 8.1 trillion yuan in outstanding mortgages last year.

NEW ZEALAND (BBG): New Zealand’s Willis Wants RBNZ to Add Summer Rate Decision

New Zealand Finance Minister Nicola Willis wants the central bank to increase the frequency of its rate decisions, ending its practice of a three-month summer break and bringing it in line with global peers. “I’m particularly concerned about the 12-week break over summer, which is a long time to go between meetings,” Willis told Bloomberg News in a statement. “The central banks of England, Canada, Australia and the United States have shorter breaks and meet more frequently. I think the Reserve Bank should return to meeting eight times a year.”

RUSSIA/UKRAINE (BBG): Russia Unleashes Massive Drone Attack Against Kyiv and Odesa

Russia unleashed a sweeping drone attack on the Ukrainian capital of Kyiv and the Black Sea city of Odesa that left a trail of destruction as President Volodymyr Zelenskiy demanded increased pressure on Moscow to end the war. Zelenskiy said the attacks resulted in fatalities and at least 13 others were injured. Russian projectiles destroyed a first aid station and damaged a maternity ward and other residential buildings in Odesa’s historic downtown, local authorities said.

DATA

UK DATA (MNI): Soft Wage and Payrolls Data

- UK APR AVE WEEKLY EARNINGS +5.3% YY

- UK APR AVE WEEKLY EARNINGS EX-BONUS +5.2% YY

- UK MAY CLAIMANT RATE +4.5%

- UK MAY CLAIMANT CHG +33100

The wage data there all a bit softer than expected, including the key private regular AWE data that was 2 tenths below consensus. The unemployment data was in line with expectations, rising to 4.6%. A really big miss for the very volatile flash PAYE RTI payrolls number at -109k for May. Take that with a handful of salt. But the April figure being

revised down to -55k (rather than revised up) is a little concerning here. Overall the data is on the soft side. Looking at the private regular AWE data in more detail, there was a downward revision to the single month Y/Y for March 2025 of 0.13ppt to 4.85%Y/Y which saw the 3-month data revised down to 5.51%Y/Y in the 3-months to March 2025 (so that is now 0.25ppt below the BOE's forecast of 5.76%).

UK BRC MAY BY VALUE SHOP SALES LFL +0.6% YY, TOTAL +1% YY (MNI)

NORWAY DATA (MNI): Easing CPI-ATE Momentum Underscores Case for H2 Easing

- NORWAY MAY CPI +0.4% M/M, +3% Y/Y

- NORWAY MAY UNDERLYING CPI +0.2% M/M, +2.8% Y/Y

Although Norges Bank is not under pressure to cut rates due to a relatively resilient mainland economy, the unwind of Q1 inflationary pressures (which delayed the first cut back in March) suggest there is scope to ease at least once in H2 - in line with the March MPR rate path. Seasonally adjusted CPI-ATE prices rose 0.08% M/M for the second consecutive month in May, and have now been consistent with 2% inflation on an annualised basis since March. 3m/3m momentum pulled back to 2.95% (vs 4.11% in April, 4.22% in March) for the lowest since November 2024.

SWEDEN DATA (MNI): Riksbank Business Survey Screens Dovish, Limited FX Impact for Now

The Riksbank Business Survey screens dovish at first glance. The activity signals highlight downside risks to demand, largely stemming from trade-related uncertainty. Although businesses selling to households are planning to increase their prices, the key excerpt (which is not in the press release, only the full report) is that "they are not planning to raise prices more or more often than normal". The survey appears to support market pricing that implies a near-80% implied probability of a June cut.

SWEDEN DATA (MNI): Solid Consumption and Production in April, but Pinch of Salt Needed

Swedish April GDP rose 0.4% M/M, which may come as somewhat of a relief after the weaker-than-expected Q1 GDP print (-0.2% Q/Q). However, as always the monthly activity data should be taken with a pinch of salt - it is not often a good predictor of actual GDP outcomes and is prone to revisions. Despite these caveats, household consumption and business production rose solidly in April. Consumption rose 0.5% M/M (vs -0.1% prior), corresponding to a 0.6% 3m/3m rate (vs 0.5% prior). There was monthly growth in food and beverage sales, furniture and household equipment, transport and recreation.

AUSTRALIA DATA (MNI): May NAB Business Labour Costs Fastest Since January

NAB business price/cost components in May were mixed containing elements of concern and optimism. The pickup in labour costs in addition to signs that wage growth is rising again are likely to be monitored closely. The employment component of the survey though was very weak which may pressure pay gains. Purchase costs rose 1.1% 3m/3m and the price of final products were up only 0.5%, both the slowest since January 2021. Retail prices rose 1.2% 3m/3m, unchanged from April and the fastest since October.

FOREX: GBP Dip Bottoms Out Ahead of Key EMA Support

- GBP has broken lower on the back of a poorer-than-expected labour market report. Average weekly earnings came in softer-than-expected at 5.3% vs. Exp. 5.5% and the monthly change in payrolled employees dropped sharply: to -109k vs. Exp. -20k, with the April figure also subject to a downward revision. As a result, the UK jobs picture and the latest insight into wage growth have been marked lower relative to the Bank of England's projections, raising the odds of a more activist approach from the MPC.

- As a result, BoE OIS markets have returned closer to 2 x 25bps rate cuts for this year, with September close to fully priced for the next cut. Risks to this position, however, include revisions to these numbers in subsequent releases, which have a track record in correcting data outliers.

- Weakness in GBP came in two phases this morning, first on the soft payrolls data, and then again on the SONIA open, with GBPUSD nearing 1.3462, its 20-day EMA. A clear break of this average would suggest potential for a

deeper correction and expose the 50-day EMA for direction, at 1.3299. EURGBP meanwhile has cleared 0.8440, its 50-day EMA and key resistance, exposing 0.8541, the May 2 high. - The USD trades firmer against broader G10, with the corrective relief for the USD Index isolating the downtrendline drawn off the early February high as next resistance, today at 99.575.

- There are no remaining key data releases due Tuesday, and no further central bank speakers (the Fed remain inside the pre-decision media blackout period), keeping focus on the resumption of trade talks between US and Chinese trade negotiation teams in London.

EGBS: Bund Futures Consolidate Early Rally; ECB Pullback Considered Corrective

Bund futures have consolidated the early rally, which came on the back of softer-than-expected UK labour market data and weak European equity sentiment. Futures are +36 ticks at 130.66, with initial resistance at 130.99 (yesterday’s high). The technical picture remains unchanged, with the ECB-driven pullback still appearing corrective - for now - and the trend condition remaining bullish.

- Regional headline flow has been light. ECB speakers (Villeroy, Rehn) have not shifted sentiment, nor did the stronger-than-expected June Sentix survey (0.2 vs -5.5 cons, -8.1 prior).

- The German curve has bull flattened, with 30-year Bund yields down 3bps and Schatz yields down 1bp. Germany will sell E4bln of the 2.40% Apr-30 Bobl at 1030BST.

- Meanwhile, the Netherlands sold 10-year DSLs earlier and the ESM is holding a E2bln WNG long 3-year syndication. Finland will sell RFGBs at 1100BST.

- 10-year EGB spreads to Bunds are within 1bp of yesterday’s closing levels. Overnight, French President Macron did not rule out another dissolution of the National Assembly to hold snap elections (he is legally allowed to do so as of July). While this has had limited impact on OAT spreads intraday (+1bps at 68bps), it serves as a reminder that French political (and fiscal) risks are still lurking in the background.

- Broader macro focus remains on the outcome of US-China trade talks, which have entered their second day.

GILTS: Labour Market-Driven Rally Holds, Next BoE Cut Priced for Sep

Gilts remain underpinned after drawing support from softer-than-expected wage data and a larger-than-expected fall in payrolled employees.

- Downticks in e-minis and European equity indices provided further support (but lacked an overt driver), even with the FTSE 100 benefitting from a softer GBP.

- Gilt futures traded as high as 92.66 before fading back to ~92.50, adding more than 70 ticks vs. yesterday’s settlement.

- Initial resistance located at the June 5 high (92.63) has been pierced, with bulls now looking to a Fibonacci resistance point (92.79).

- Yields 5-7bp lower, 10s outperform on the curve.

- 2-Year yields set for the lowest close seen since May 9, while 10s and 30s trade below their respective closes from the same day.

- 2s10s holds above 60bp, with recent moves below that level limited in scope and short-lived.

- 5s30s trade around 120bp after the recent run of closes below the level.

- GBP STIRs now fully discount the next 25bp cut come the end of the September MPC, with 48bp of cuts showing through year-end (vs. 41bp late yesterday). Labour market data drives things there.

- Books on the 1.75% Sep-38 I/L gilt syndication are closed, with demand nearing ~GBP60bln ~15 minutes before books closed (per bookrunners).

- Macro matters are set to dominate for the rest of the day, with domestic inputs (comments from BoE’s Saporta & the government spending review) set to come back to the fore tomorrow.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.208 | -0.3 |

Aug-25 | 4.019 | -19.3 |

Sep-25 | 3.957 | -25.5 |

Nov-25 | 3.800 | -41.2 |

Dec-25 | 3.730 | -48.2 |

Feb-26 | 3.629 | -58.3 |

Mar-26 | 3.606 | -60.6 |

EQUITIES: Fresh Cycle Highs for E-Mini S&P Affirm Bullish Conditions

The trend cycle in Eurostoxx 50 futures is bullish and the contract is trading closer to its recent highs. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5205.88, the 50-day EMA. A clear break of this average would signal a possible reversal. The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract has again traded to a fresh cycle high, today. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. A continuation would open 6057.00 next, the Mar 3 high. Key support lies at 5798.36, the 50-day EMA.

- Japan's NIKKEI closed higher by 122.94 pts or +0.32% at 38211.51 and the TOPIX ended 0.83 pts higher or +0.03% at 2786.24.

- Elsewhere, in China the SHANGHAI closed lower by 14.955 pts or -0.44% at 3384.816 and the HANG SENG ended 18.56 pts lower or -0.08% at 24162.87.

- Across Europe, Germany's DAX trades lower by 161.16 pts or -0.67% at 24012.39, FTSE 100 higher by 26.35 pts or +0.3% at 8858.64, CAC 40 down 12.11 pts or -0.16% at 7779.36 and Euro Stoxx 50 down 16.81 pts or -0.31% at 5404.71.

- Dow Jones mini down 50 pts or -0.12% at 42749, S&P 500 mini down 1.25 pts or -0.02% at 6009.25, NASDAQ mini down 9.25 pts or -0.04% at 21816.

Time: 10:00 BST

COMMODITIES: Medium-Term Trend Signals for Gold Remain Bullish

WTI futures are trading higher this week, extending the current bull cycle. The contract has cleared the 50-day EMA and this signals scope for an extension towards $65.82 next, the Apr 4 high. It is still possible that the recovery since early May is a correction. MA studies are in a bear-mode position, highlighting a dominant medium-term downtrend. Support to watch lies at $59.74, the May 30 low. A break would highlight a potential bearish reversal. A bullish theme in Gold remains intact and the latest pullback appears corrective. Medium-term trend signals are bullish - moving average studies remain in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would refocus attention on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, the next support to monitor is $3242.4, the 50-day EMA.

- WTI Crude up $0.12 or +0.18% at $65.43

- Natural Gas down $0.01 or -0.3% at $3.629

- Gold spot up $3.04 or +0.09% at $3329.28

- Copper down $4.9 or -0.99% at $487.65

- Silver down $0.22 or -0.61% at $36.5365

- Platinum down $9.05 or -0.74% at $1211.54

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 10/06/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 10/06/2025 | - | *** | Money Supply | |

| 10/06/2025 | - | *** | New Loans | |

| 10/06/2025 | - | *** | Social Financing | |

| 10/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 10/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 10/06/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/06/2025 | 0630/0730 | BOE Saporta Speech At Bank of Finland and SUERF Conference | ||

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0930/1130 | ECB Lane At 2025 Government Borrowers Forum | ||

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI | |

| 11/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/06/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/06/2025 | 1800/1400 | ** | Treasury Budget |