MNI US MARKETS ANALYSIS - Zelenskyy to Oval Office

Highlights:

- With seemingly minimal progress at Trump-Putin meet, focus shfits to Zelesnkyy trip to Oval Office today

- USD Index looks to more neutral footing ahead of Powell appearance at Jackson Hole

- Bowman set to appear on Bloomberg TV after dovish dissent at latest FOMC

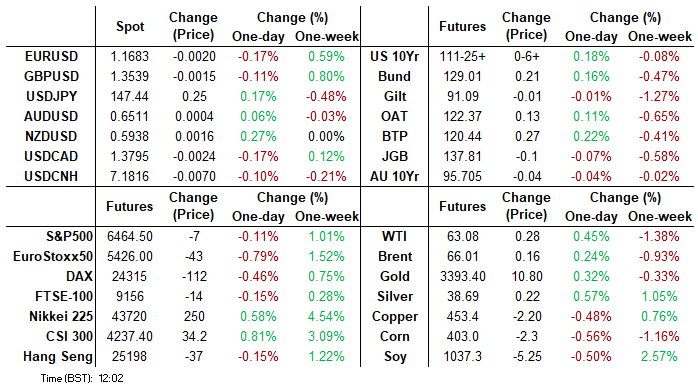

US TSYS: Mild Firmer Ahead Of Trump, Zelenskyy and EU Leader Meetings

- Treasuries are mildly firmer ahead of today’s geopol-focused session with Oval Office meetings with Trump, Zelenskyy and EU leaders.

- It’s a quiet docket otherwise although a recently notably dovish Bowman is also set to speak on Bloomberg TV.

- Cash yields are 1-2bp lower on the day, paring some of Friday’s slow-to-build post-data losses.

- 5s30s sits at 108bps having on Friday pushed to a fresh ytd high of 109.4bp.

- TYU5 trades at 111-25 (+05+) to help the late Friday lift off lows of 111-17+, amidst light cumulative volumes of 230k.

- Resistance is seen at 112-15+ (Aug 5 high), having come close with 112-14 before Thursday's PPI report, whilst support is seen at 110-19+ (Jul 24 low).

- Data: NY Fed services Aug (0830ET), NAHB index Aug (1000ET)

- Fedspeak: Bowman on Bloomberg TV (1245ET) – see STIR bullet

- Bill issuance: US Tsy $82B 13W & $73B 26W bill auctions (1130ET)

- Politics (timing as per politico): Trump and Zelenskyy only at 1315ET before Trump, Zelenskyy and EU leaders at 1500ET.

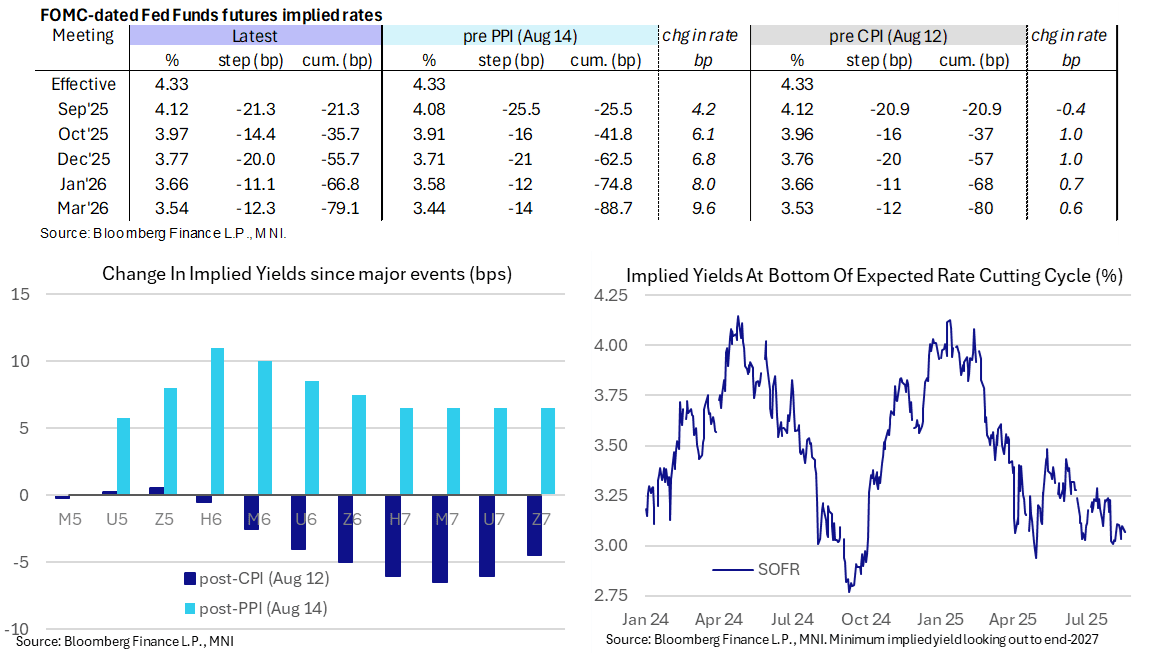

STIR: Fed Funds Futures Not Quite Convinced On September Cut

- Fed Funds implied rates consolidate last week’s shift to not quite fully pricing a 25bp cut next month, primarily after strong PPI but also helped by Friday’s retail sales. They sit up to 1bp softer from Friday’s close for the December meeting onwards.

- It’s ahead of a quiet docket and a quiet week more generally, with Powell’s Jackson Hole speech on Friday at 1000ET firmly in focus.

- Cumulative cuts from 4.33% effective: 21.5bp Sep, 35.5bp Oct, 55.5bp Dec, 67bp Jan and 79bp Mar.

- The SOFR implied terminal yield of 3.07% (SFRH7) is 3bp lower on the day as it continues to roughly hold the +/-5bp of 125bp of cuts priced from current levels seen since the Aug 1 payrolls report.

- Fed VC Supervision Bowman (permanent voter, dove) speaks on Bloomberg TV at 1245ET in her first remarks since last week’s mixed inflation data. She said on Aug 9 that she favors three cuts this year (unsurprising having dissented in July) and saw recent labor data as reinforcing this view.

- SF Fed’s Daly (non-voter) reiterated late Friday that two cuts this year remains a good projection. It’s clear the economy is slower but it’s not slow.

SOFR: Mix Of Net Short Setting & Long Cover Seen In Futures On Friday

OI data points to net short setting dominating in most contracts through the greens during Friday’s downtick in SOFR futures, before net long cover became slightly more prominent in the blues.

- The largest outright positioning swings came via net short setting in the late whites/early reds.

| 15-Aug-25 | 14-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,204,188 | 1,200,166 | +4,022 | Whites | +52,698 |

SFRU5 | 1,320,754 | 1,323,703 | -2,949 | Reds | +37,012 |

SFRZ5 | 1,402,684 | 1,379,914 | +22,770 | Greens | +7,372 |

SFRH6 | 1,044,907 | 1,016,052 | +28,855 | Blues | -1,902 |

SFRM6 | 927,356 | 905,061 | +22,295 |

|

|

SFRU6 | 902,186 | 888,757 | +13,429 |

|

|

SFRZ6 | 1,008,722 | 1,001,283 | +7,439 |

|

|

SFRH7 | 751,723 | 757,874 | -6,151 |

|

|

SFRM7 | 917,444 | 917,772 | -328 |

|

|

SFRU7 | 595,871 | 590,126 | +5,745 |

|

|

SFRZ7 | 590,479 | 590,822 | -343 |

|

|

SFRH8 | 346,329 | 344,031 | +2,298 |

|

|

SFRM8 | 272,866 | 274,676 | -1,810 |

|

|

SFRU8 | 205,145 | 206,383 | -1,238 |

|

|

SFRZ8 | 232,952 | 232,388 | +564 |

|

|

SFRH9 | 153,975 | 153,393 | +582 |

|

|

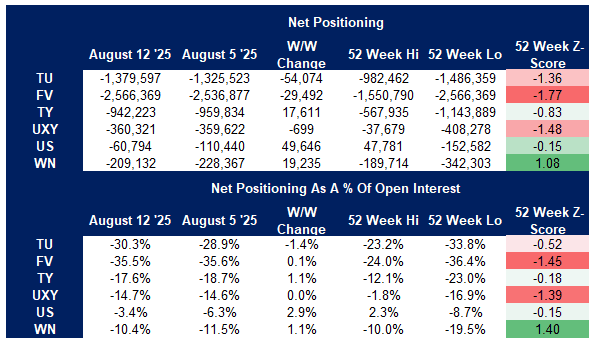

US TSY FUTURES: Asset Managers Add To Long While Funds Add To Short

The latest CFTC CoT report showed asset managers adding to their overall net long, while leveraged funds added to their net short.

- A reminder that the cut-off date for the survey was Tuesday August 12, which means that the reaction to the CPI data was captured, but price action and positioning swings in the second half of the week was not reflected.

- Asset managers added to their overall not long position, with net long setting in FV, TY, US & WN futures comfortably outweighing net long cover in TU & UXY futures. The cohort added ~$10mln DV01 equivalent in net long exposure across the curve and remains net long in all contracts.

- Leveraged funds added to their overall net short, with net short setting in every contract outside of net short cover in US futures. The cohort added ~$9.3mln DV01 equivalent in net short exposure across the curve and remains net short across all contracts.

- Wider non-commercial positioning (seen in the table below) saw net shorts extended in TU & FV futures, while they were pared back in TY, US & WN contracts (UXY positioning was little changed). The cohort remains net short across the curve.

Source: MNI - Market News/CFTC/Bloomberg Finance L.P.

GERMAN DATA: IFO Economic Experts See Above Target Inflation For 2026

Economist expectations for inflation in Germany "over the next few years are stable at 2.4 percent for 2025 and 2.3 percent for 2026 and 2028" according to an e-mailed press release with the global IFO Economic Experts Survey.

- This is noticeably above the Bundesbank expectations for these years, which are standing 2.2% for 2025, 1.5% for 2026 and 1.9% for 2027, respectively. IFO could not comment in detail on the discrepancy to us as they just collate the experts' numerical responses.

- Private sector consensus (MNI collation of 7 sellside analysts) for German CPI meanwhile stands at 2.1% for 2025, 1.7% in 2026, and 2.1% in 2027 - so more in line with the Bundesbank's view.

- A total of 1,340 economic experts from 121 countries participated in the IFO survey, which ran from June 17 to July 1 on a global level. For Germany, IFO collated expectations from around 60 economic experts.

GLOBAL POLITICAL RISK: Trump Hosts Zelenskyy & European Leaders From 13:00ET

US President Donald Trump hosts Ukrainian President Volodymyr Zelenskyy at the White House following the former’s meeting with Russian President Vladimir Putin on 15 August. Tho Oval Office meeting in February made headlines around the world after Zelenskyy was ambushed by Trump and Vice President JD Vance. This time around, Zelenskyy will have in-person support. German Chancellor Friedrich Merz, UK PM Sir Keir Starmer, French President Emmanuel Macron, Italian PM Giorgia Meloni, Finnish President Alexander Stubb and European Commission President Ursula von der Leyen will all be in attendance.

- Trump will meet with Zelenskyy first at 13:00ET/18:00BST/19:00ET, with a bilateral meeting a quarter of an hour later. Trump then greets European leaders at 14:15ET/19:15BST/20:15CET, followed by a multilateral meeting at 15:00ET/20:00BST/21:00CET.

- The sequencing that sees Zelenskyy and Trump meeting alone before the European leaders join means that the Ukrainian leader may still face public pressure from Trump to agree to a suboptimal (for Kyiv) peace agreement.

- While Zelenskyy and the European leaders will seek to impress upon Trump the requirement for security guarantees for Ukraine, the US president has already sought to rule out the return of Crimea and the prospect of Ukrainian NATO membership.

FOREX: Markets Look More Neutral into Ukraine Summit, Jackson Hole

- The USD trades furtively stronger early Monday, largely following a phase of EUR/USD sales that pressed the price back below 1.17 and through the Asia-Pac lows in early trade. The move came in tandem with equity weakness and concurrent UST strength, and while moves are shallow (EUR/USD remains well clear of any test of Thursday's pullback low at 1.1631), the price action shows that markets are wary of over-optimism after the Putin-Trump meeting that resulted in very little progress, and may be more comfortable trimming USD positioning to a more neutral poise (last week's CFTC update showed the USD net short trimmed off a multi-year low) headed into Powell's Jackson Hole appearance Friday.

- Despite a more sensitive equity market, AUD and NZD mildly outperform, helping AUD/USD hold its ground above the 0.6500 level. This keeps AUDUSD inside a range. From a trend perspective, the condition remains bullish and key resistance to monitor has been defined at 0.6625, the Jul 24 high. Clearance of this level would confirm a resumption of the uptrend and open 0.6677, a Fibonacci projection.

- Optionality today includes sizeable strikes between 1.1600-50 (approx. E2.2bln), with AUD/USD also notable interest between $0.6500-10 (A$690mln) expiring today.

- Focus for the duration of the session rests on President Trump's meeting with Ukraine's Zelenskyy at the White House. The meeting follows Friday's somewhat disappointing summit held between Trump and Putin - and while concerns remain over Zelenskyy's last appearance in the Oval Office, this time Germany's Merz, UK's Starmer and EU's von der Leyen will also be in attendance. Trump is to meet with Zelenskyy at 1300ET/1800BST. Trump then greets European leaders at 1415ET/1915BST.

- Continued speculation over the plan for Powell's succession into 2026 remains the medium-term risk, and Powell's Jackson Hole appearance will be viewed through this lens. Of note, prospective Fed Chair candidate Bowman appears on Bloomberg TV later today, having dissented from the most recent Fed meeting to opt for a rate cut.

OPTIONS: Expiries for Aug18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1560(E1.1bln), $1.1575(E678mln), $1.1600-05(E606mln), $1.1640-50(E1.2bln), $1.1800(E683mln)

- USD/JPY: Y147.90-00($544mln)

- AUD/USD: $0.6475(A$542mln), $0.6500-10(A$689mln)

EQUITIES: Dominant Uptrend in E-Mini S&P Remains Intact

- A bullish theme in Eurostoxx 50 futures remains intact and the contract is trading at its latest highs. The print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00, the Mar 3 high (cont) and key resistance. Moving average studies remain in a bull-mode position, highlighting an uptrend. Support to watch lies at 5345.89, the 50-day EMA.

- The dominant uptrend in S&P E-Minis remains intact and the contract is trading at its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6392.29, the 20-day EMA, and 6267.88, the 50-day EMA.

COMMODITIES: WTI Futures Remain in a Clear Bear Cycle

- WTI futures remain in a clear bear cycle and the contract is trading closer to its recent lows. A key support at $62.84, the Jun 24 low, has been breached, strengthening a bearish theme. A continuation lower would open $58,17 the May 30 low. Key short-term resistance has been defined at $70.51, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $64.94, the 50-day EMA.

- A bull cycle in Gold remains intact and this is highlighted by moving average studies that remain in a bull-mode position. This sideways trend that has been in place since the Apr peak appears to be a corrective phase. A resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. On the downside, first support to watch lies at $3268.2, the Jul 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 18/08/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 18/08/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 18/08/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 18/08/2025 | 1430/1530 | DMO likely to publish FQ3 consultation agenda | ||

| 18/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 18/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 19/08/2025 | 0800/1000 | ** | EZ Current Account | |

| 19/08/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 19/08/2025 | 1230/0830 | *** | CPI | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 19/08/2025 | 1810/1410 | Fed Vice Chair Michelle Bowman |