MNI US MARKETS ANALYSIS - Ylds Hold Higher, Putin-Witkoff Meet

Highlights:

- Treasuries hold entirety of yesterday's clear of support

- Putin - Witkoff set to meet to discuss latest Ukraine proposals

- Light data day / Fed inside blackout leaves newsflow quieter

US TSYS: Holding Yesterday’s Clearance Of Notable Support, Putin/Witkoff Ahead

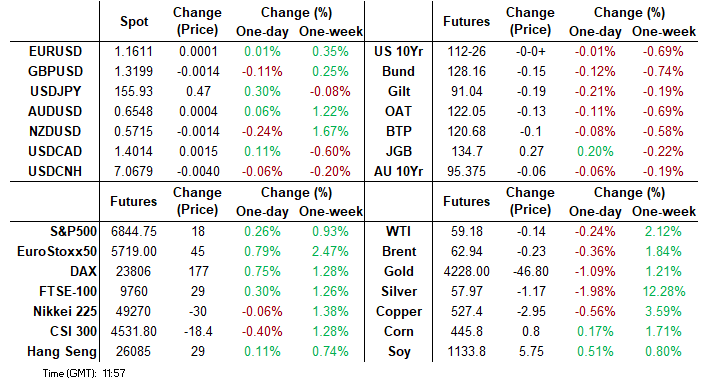

Treasuries have kept to narrow ranges overnight as they consolidate yesterday’s large sell-off attributed to rate-locks & speculative selling. Today sees a particularly thin docket leaving attention more firmly on Putin/Witkoff remarks along with broader headline watching. Tomorrow then starts to see more notable labor data and ISM services.

- Cash yields are 0.2-0.8bp higher on the day.

- TYH6 trades close to earlier lows of 112-25 (-01+) having nudged half a tick below yesterday’s low, with reasonable cumulative volumes of 280k.

- Yesterday saw it pierce the 50-day EMA at 112-27 and a clear breach here would undermine a recent bull theme and signal scope for a deeper retracement. Next lies 112-10+ (Nov 20 low) before a key 112-07 (Nov 5 low) whilst a reversal higher is required to refocus attention on the key resistance and bull trigger at 113-29+ (Oct 17 high).

- Data: Wards vehicle sales Nov

- Fedspeak: Fed VC Bowman financial testimony (1000ET) – in blackout, see STIR bullet

- Bill issuance: US Tsy $75B 6W bill auction (1130ET)

- Politics: Putin/Witkoff meet (0900ET), Trump hosts a Cabinet meeting (1130ET), Trump makes an announcement which WH Press Sec Leavitt has said will be on his Trump accounts initiative (1400ET)

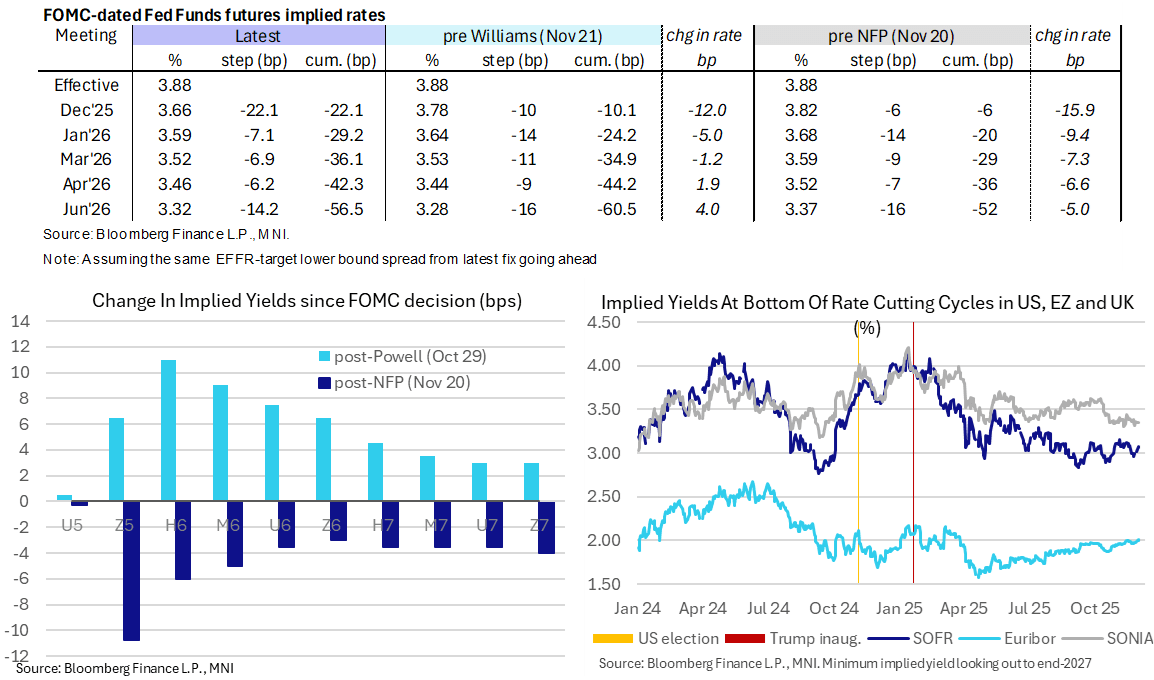

STIR: Fed Rates Consolidate Confidence In Hawkish Cut Next Week, Hassett At 80%

- Fed Funds implied rates are little changed on the day as they continue to reflect the push towards heavily pricing in another 25bp cut from the FOMC next week with a lack of pushback since Williams’ uncharacteristic guidance.

- NEC’s Hassett has continued to see a boost in betting markets, now seen with 80% likelihood of being the next Fed chair on Polymarket. There’s nothing concrete on potential timings, with Trump saying on Sunday he has made up his mind and “we’ll be announcing it”. Finalists are supposedly being interviewed by VP Vance and senior White House staff this week and Bessent has previously indicated a decision will be before Christmas.

- Cumulative cuts from 3.88% effective: 22bp Dec, 29bp Jan, 36bp Mar, 42.5bp Apr, 56.5bp Jun.

- SOFR futures are 0-0.01 higher, consolidating yesterday’s broader fixed income sell-off attributed to rate-locks & speculative selling. The terminal implied yield of 3.065% (H7) has increased off a particularly steady period around 3% seen since Williams on Nov 21.

- VC Supervision Bowman testifies before the House finance committee at a hearing on Oversight of Financial Regulators at 1000ET, with text and Q&A. Being within the FOMC media blackout period, it won’t touch on the economic outlook or monetary policy.

SOFR: Mix Of Short Setting & Long Cover Noted In Futures On Monday

OI data points to net short setting dominating in the white pack before net long cover moved to the fore further out the strip as most SOFR futures settled lower on Monday.

| 01-Dec-25 | 28-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,359,058 | 1,359,402 | -344 | Whites | +67,976 |

SFRZ5 | 1,704,831 | 1,685,992 | +18,839 | Reds | -312 |

SFRH6 | 1,339,735 | 1,324,380 | +15,355 | Greens | -18,051 |

SFRM6 | 1,160,427 | 1,126,301 | +34,126 | Blues | -20,787 |

SFRU6 | 1,086,000 | 1,098,478 | -12,478 |

|

|

SFRZ6 | 1,124,654 | 1,136,385 | -11,731 |

|

|

SFRH7 | 849,791 | 832,235 | +17,556 |

|

|

SFRM7 | 794,601 | 788,260 | +6,341 |

|

|

SFRU7 | 831,257 | 845,724 | -14,467 |

|

|

SFRZ7 | 851,757 | 863,074 | -11,317 |

|

|

SFRH8 | 444,857 | 437,506 | +7,351 |

|

|

SFRM8 | 407,296 | 406,914 | +382 |

|

|

SFRU8 | 369,077 | 371,881 | -2,804 |

|

|

SFRZ8 | 324,463 | 331,198 | -6,735 |

|

|

SFRH9 | 194,166 | 207,528 | -13,362 |

|

|

SFRM9 | 209,308 | 207,194 | +2,114 |

|

|

EUROPEAN INFLATION: MNI HICP tracking remains in line with consensus at 2.1%Y/Y

- MNI's tracking estimate for Eurozone HICP comes in line with consensus at 2.1%Y/Y with two-way risks (our unrounded tracking is currently at 2.10%).

- This is based on 92.4% of the country reports. Ahead of our initial tracking estimate last week we had received flash HICP having from Germany, France, Italy, Spain, Belgium, Portugal and Slovenia.

- The release of Ireland yesterday and the Netherlands and Austria today have reduced the unrounded tracking estimate from 2.11% to 2.10%.

- The data is due for release at 10:00GMT / 11:00CET.

EUROPE ISSUANCE UPDATE:

UK auction results

- GBP1bln of the 0.125% Aug-31 Linker. Avg yield 0.949% (bid-to-cover 3.88x).

German auction results

- E4.5bln (E3.563bln allotted) of the 2.00% Dec-27 Schatz. Avg yield 2.05% (bid-to-offer 1.37x; bid-to-cover 1.73x).

UK DMO UPDATE: Consultation: Syndication expectations for FQ4

- Medium green syndication (February): Most GEMMs supported a 10-12 year maturity with "some calls" for a 12-14 maturity. "Most recommendations" from investors were for 10-12 year maturitires, too.

- Note that the DMO bucket allows GBP6.2bln size which would bring green issuance for FY24/25 up to the GBP10bln limit.

- Long syndication (January): We have aruged that the 5.25% Jan-41 gilt would be the most likely gilt. There was "clear support" for this among investors with "most" GEMMs also supporting this. "Several" GEMMs and investors thought it prudent to delay a decision until nearer the time with some also calling for a reopening of the 5.375% Jan-56 gilt. We therefore think that we might not get confirmation in the operations schedule on Friday, but would still be very surprised if the 5.25% Jan-41 gilt was not chosen by the DMO.

- A reminder that there are no long auctions scheduled for the quarter (but there are two proposed tenders).

- Shorts (5 auctions): Views for both GEMMs and investors were for 2-3 auctions of each of these (but it doesn't seem to have been clear with of the gilts was favoured for three rather than two auctions).

- 4.00% May-29 gilt: 2-3 auctions

- 4.125% Mar-31: 2-3 auctions

- Medium (5 auctions)

- 4.125% Mar-33 gilt: MNI expects 2 auctions (generally supported by investors and GEMMs)

- 4.75% Oct-35 gilt: MNI expects 3 auctions (generally supported by investors and GEMMs)

- 5.25% Jan-41 gilt: Isolated calls from both GEMMs and investors for a reopening later in the quarter (we see this as unlikely, particularly as we strongly expect this to be the long syndication choice in January).

- Linkers (2 auctions):

- 1.125% Sep-35 linker: MNI expects 1 auction (supported by GEMMs and investors). There were isolated calls from GEMMs for 2 auctions.

- 1.875% Sep-49 Linker: Mainly supported by GEMMs and investors

- Programmatic gilt tender schedule: Some investors and GEMMs preferred to have a short-dated tender in January to allow reinvestment from the maturing 0.125% Jan-26 gilt.

FOREX: USDJPY Bounce Off Lows Erases Much of Monday Decline

- USDJPY extended its recovery from yesterday's 154.67 lows, erasing a large part of the move triggered by Ueda at the beginning of the week. The pair has pierced back above the 20-day EMA - which remains a key intraday pivot point. A stronger risk backdrop has helped, with the ~150 pip bounce back above 156.00 looking convictive. Technical considerations would also suggest the trend set-up in USDJPY is bullish and the latest pullback can be considered corrective. The bull trigger for USDJPY remains 157.89, the November 20 high.

- GBPUSD meanwhile weakened below the 1.3200 handle as BoE's Bailey talks through the Bank's Financial Stability Report, in which the FPC see the economy as being exposed to greater risks to financial stability. The trend theme in GBPUSD is unchanged, it remains bearish and a recovery in November appears corrective. Initial support sits at 1.3125, the Nov 26 low.

- Russian President Putin is set to meet US's Witkoff and Kushner later today to discuss the amended 19-point peace plan negotiated between American and Ukrainian officials in late November. A breakthrough would undoubtedly be risk-positive but prediction markets remain sceptical of a ceasefire in the very near term.

- The rest of today's calendar is light, with only Redbook Retail Sales scheduled in the US and the Fed remaining in blackout. ECB's Dolenc is scheduled to speak but unlikely to move the needle.

OPTIONS: Expiries for Dec02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1560(E1.1bln), $1.1600(E596mln), $1.1615-25(E1.4bln)

- USD/JPY: Y155.00($2.6bln), Y156.00($885mln), Y156.50($951mln)

- GBP/USD: $1.3030-50(Gbp2.1bln)

- EUR/GBP: Gbp0.8800(E700mln), Gbp0.8830-50(E1.1bln)

EQUITIES: E-Mini S&P Holding Onto Gains Following Recovery From Nov 21 Low

- Recent gains in Eurostoxx 50 futures undermines a recent bearish theme and the contract is holding on to its gains. Price has traded above the 20- and 50-day EMAs, signalling scope for a stronger recovery near-term. A continuation would open 5742.40, a Fibonacci retracement point. For bears, a reversal lower would instead expose the key short-term support and bear trigger at 5475.00, the Nov 21 low.

- S&P E-Minis are holding on to their recent gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

COMMODITIES: Short-Term Gains for WTI Futures Considered Corrective

- Short-term gains in WTI futures are considered corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. Note that the recovery since Oct 28 signals the end of the corrective cycle. Key support to watch lies at the 50-day EMA, at $4001.1. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 02/12/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 02/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 02/12/2025 | 1500/1000 | Fed Vice Chair Michelle Bowman | ||

| 03/12/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 03/12/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/12/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/12/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/12/2025 | 0030/1130 | *** | Quarterly GDP | |

| 03/12/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/12/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 03/12/2025 | 0700/0200 | * | Turkey CPI | |

| 03/12/2025 | 0730/0830 | *** | CPI | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 03/12/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/12/2025 | 1000/1100 | ** | EZ PPI | |

| 03/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/12/2025 | 1030/1130 | ECB Lane Keynote at Banca d'Italia Workshop on Exchange Rates | ||

| 03/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 03/12/2025 | 1315/0815 | *** | ADP Employment Report | |

| 03/12/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 03/12/2025 | 1330/1430 | ECB Lagarde Statement at ECON Hearing | ||

| 03/12/2025 | 1415/0915 | *** | Industrial Production | |

| 03/12/2025 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 03/12/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 03/12/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 03/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 03/12/2025 | 1530/1630 | ECB Lagarde Statement at ECON Hearing (as ESRB Chair) | ||

| 03/12/2025 | 1700/1700 | BOE Mann in Panel on Reserve Currencies |