MNI US MARKETS ANALYSIS - Yield Curves Dictate Play; USD Rally

Highlights:

- Longer-end yields rise sharply across US, UK and Europe

- USD rally puts USD Index on cusp of forming downtrendline resistance

- Bumper issuance day, with sizeable syndications from UK, Italy, Lithuana and supply from Germany

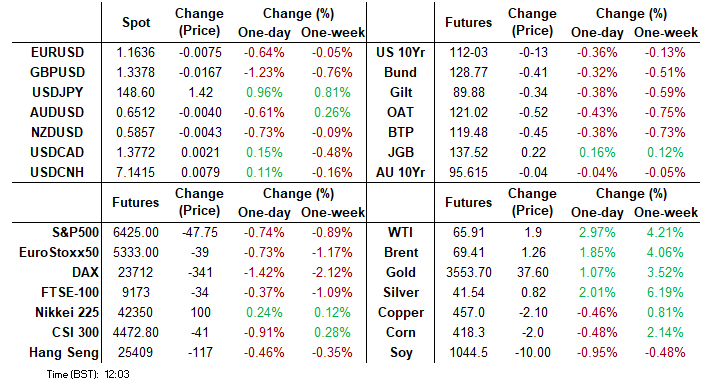

US TSYS: Bear Steeper With ISM Mfg, Cook Case and Heavy Bill Supply Ahead

- Treasuries trade firmly bear steeper and are at session lows across major benchmarks with no paring of the moves as US desks filter in after Labor Day cash closures.

- Cash yields are 3.9-6.0bps higher from Friday’s close, with 2s lagging increases and 7s to 10s modestly leading them.

- Fresh ytd steeps were seen in Asia trading, 5s30s hitting 124.5bps (currently 123.1bps) as curves reflect recent European steepening but also Japan after latest political developments.

- TYZ5 has seen session lows of 112-02+, -13+ from Friday’s settle although with a slightly smaller drop from 112-11+ at yesterday’s early close.

- It moves closer to resistance at 111-31 (20-day EMA) after which lies 111-18+ (50-day EMA), with a pullback deemed corrective. Resistance meanwhile is seen at 112-20+ (Aug 28/29 high).

- Steepening impetus can also depend on any headlines potentially today from the Fed Gov. Cook court case. US District Judge Jia Cobb on Friday asked Cook’s lawyers to file a brief today spelling out their arguments for why Trump’s firing of Cook was unlawful. This is a case that seems likely to ultimately end up in the Supreme Court.

- We also get the ISM manufacturing report for August, after most regional Fed surveys saw improvements in new orders, and heavily than usual bill issuance in the holiday-shortened week.

- Data: S&P Global mfg PMI Aug final (0945ET), ISM mfg Aug (1000ET), Construction spending Jul (1000ET)

- Bill issuance: US Tsy $82B 13W & $73B 26W bill auctions (1130ET), US Tsy $85B 6W bills & $50B 52W bill auctions (1300ET)

- Politics: Trump makes an announcement – topic unknown (1400ET)

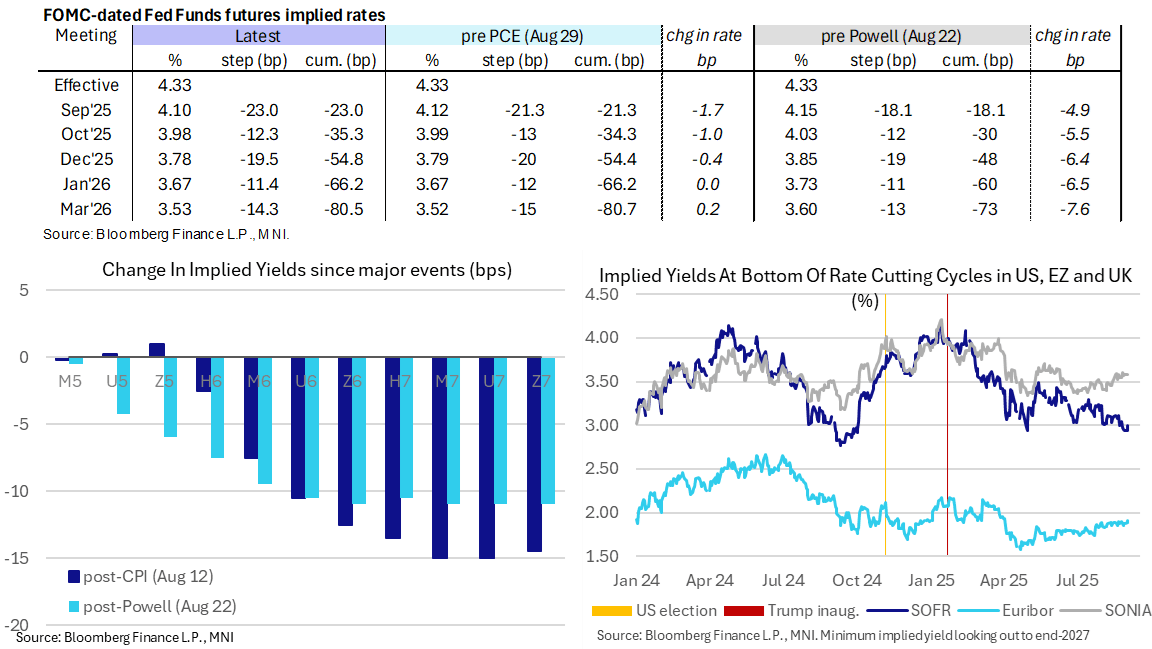

STIR: September Fed Cut Seen Mostly Locked In, ISM Mfg Ahead

- Fed Funds implied rates for near-term meetings are mixed relative to Friday’s levels post-Labor Day, with slightly higher odds of cut later this month but modestly more hawkish further out.

- Strong increases in WTI prices are having relatively little impact on front rates.

- Cumulative cuts from 4.33% effective: 23bp Sep, 35.5bp Oct, 55bp Dec, 66bp Jan and 80.5bp Mar.

- SOFR futures are up to 5 ticks lower in 2027 contracts vs Friday’s close, although with almost half of that coming yesterday in holiday-thinned trade.

- The SOFR implied terminal yield remains in the H7, at 2.995% (+5bp from Fri) having modestly lifted off last week’s recent lows of ~2.95%. It still points to more than 130bp of cuts ahead.

- Directionally, Fed terminal pricing remains at odds with the trend increase in BoE and ECB expectations over the past couple months.

- Today’s macro focus is on the ISM manufacturing survey before labor data comes into focus tomorrow ahead of Friday’s NFP report.

- Next scheduled Fedspeak comes from St Louis Fed’s Musalem (’25 voter, hawk) on the economy and policy tomorrow at 0900ET.

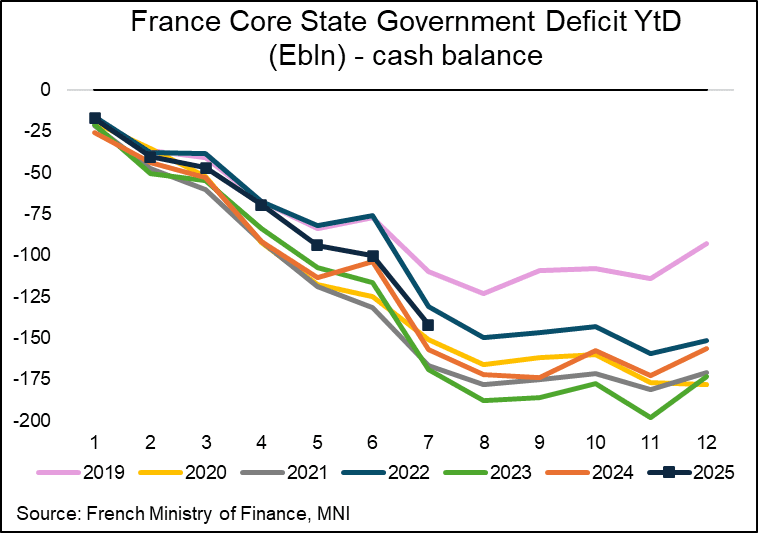

EUROPEAN FISCAL: French YTD Deficit Improved vs 2024, Confidence Vote In Focus

The French core state budget deficit returned to more favourable ytd tracking compared to 2024, primarily on higher revenues. The E142bn ytd deficit is already worth ~4.8% of annual GDP but with the bulk of the year's cumulative deficit likely already seen owing to the seasonal profile. As always though, take care translating this into the general government basis used for the 2025 deficit target of 5.4% GDP.

- The French core state year-to-date budget deficit widened to E142bn in July (vs E100.4bn June), an improvement of E14.9bn relative to E156.9bn in July 2024.

- It sees a return of more favourable tracking relative to a year ago after June’s E3bn limited improvement was helped by 2024 base effects from a shifting in EU RRF payments and also a temporarily smaller deficit in special accounts.

- Expenditures (BG + PSR) are E3.4bn lower ytd than in 2024, with the press release noting that this is “mainly explained by the elimination of Program 369”, the COVID-19 state debt amortisation programme.

- The relative improvement is instead mainly driven by revenues being E11.3bn higher, with the largest single contributor from other tax revenues of which E4.1bn is seen related to the end of the energy tariff shield.

- The 10-year OAT/Bund spread is almost 1.5bp wider today at 80bps, with intraday price action seemingly a function of broader core FI moves rather than any domestic developments. While the spread is off last week's closing extremes of 81.5bps, political/fiscal-related widening pressures remain in focus. A reminder that the spread was hovering around ~70bps prior to PM Bayrou's previous no-confidence vote announcement.

- The new upcoming confidence vote (called last week) takes place on Mon 8 Sept, with the dismissal of the current gov’t looking more likely than not, owing to both the left-wing New Popular Front and the right-wing National Assembly set to vote against the confidence motion.

- FM Lombard last week said France will meet the 2025 deficit target of 5.4% GDP and that he’s confident the 2026 budget deficit will be the proposed 4.6% GDP (both estimates on a broad general government basis rather than core state figures released today).

EUROPE ISSUANCE UPDATE:

UK syndication: Allocations

- GBP14bln (MNI expected GBP8-12bln with risks skewed to the higher end given the large book size) of the 4.75% Oct-35 gilt. Spread set earlier at 4.50% Mar-35 Gilt +8.25bp (guidance was +8.25/+8.75bps), books closed in excess of GBP140bln (inc JLM interest of GBP12bln - second largest ever for a gilt)

Italy syndication: Final terms

- E13bln (MNI expected E5-10bln with risks skewed to E7-8bln so this is much larger than expected). Books closed in excess of E110bln, spread set at 3.25% Jul-32 BTP + 8.0bp (guidance was +10bps area)

- Putting that Italian syndication size into context - the E13bln tranche is the largest ever for a 7-year (although we have seen two E13bln and one E14bln tranches for 10/10/15 year syndications - with the two E13bln seen this year).

- The combined transaction size of E18bln matches the January size of E18bln (10-year and 20-year green).

Lithuania syndication: Mandate

- "The Republic of Lithuania has mandated Erste Group, HSBC and Societe Generale as Joint Lead Managers and Luminor Bank as Co-Manager for a potential EUR-denominated Regulation S dual-tranche transaction, consisting of a long

10-year maturity and a 20-year maturity to be launched in the near future, subject to market conditions." - Lithuania's issuance plan for 2025 sees a E6.0bln Eurobonds issuance target. E2.0bln was raised at syndication in January (dual-tranche 5/15-year) and we calculate just under E1.2bln has been sold at auction.

- This leaves E2.0bln as our expected size (split equally between the two tranches). We see two-way risks to this (towards either E1.5bln or E2.5bln).

German auction results

- E4.5bln (E3.552bln allotted) of the 1.90% Sep-27 Schatz. Avg yield 1.96% (bid-to-offer 1.60x; bid-to-cover 2.03x).

FOREX: Early Dose of Risk-Off Triggers Losses for GBP, JPY

- Following generally steady Asia-Pac trade, markets underwent a sharp dose of risk-off alongside the European open as a sustained shoot higher in longer-end yields unsettled sentiment across equities, currencies and bond markets. The mix this morning of: political uncertainty in Japan (various resignations across the LDP), a window-dressing UK reshuffle (not expected to resolve Starmer's popularity crisis in the near-term) and acute pressure on the longer-end of the UK, US and European yield curves - has reignited fiscal, financing and politic risk concerns around higher borrowing costs - driving sentiment through the European open.

- Sizeable down-move in GBP/USD comes despite the bullish technical backdrop that stemmed from the bullish engulfing candle posted on August 22nd. With spot showing through the lows already today, this somewhat undermines the recovery off 1.3391 and instead retracement support expected into 1.3315 and 1.3369 is of more importance.

- Gains for the USD Index put the currency on for a strong start to September. The daily candle chart has the USD Index on course to form downtrendline resistance drawn off the early August high at today's 98.389 print.

- Today's price action serves as a further reminder of the pressure on governments from bond markets, particularly as Summer concludes. Today's Gilt price action shows markets are not satisfied with floated proposals so far for the UK Treasury to raise indirect taxes through property, capital gains, landlords, or otherwise. Given the internal party opposition to spending cuts, this places additional pressure on the Chancellor's pledge not to raise VAT, income tax or national insurance this parliament - a topic that will likely be a market focus into the Autumn Budget - and may have to become a more palatable option the longer yields stay higher.

- Focus for the duration of Tuesday trade remains on the volatility in the longer-end of the curve, as well as the ISM manufacturing print for August. The release will be watched carefully for clues or signals headed into this Friday's highly consequential NFP print.

UK: Yield Move in Focus as Treasury Preps to Notify OBR of Budget Date

Acute move in UK curve will be being carefully watched by the Chancellor and the Treasury this morning - particularly as Chancellor needs to give the OBR 10 weeks notice with which to prepare forecasts (which will incorporate the latest moves in yields).

- 5th November had previously been the most likely date for the Budget, in which case the 10 weeks notice would have to have been given last week, privately.

- As such, we see a November / December Budget looking more probable, with 12th November the earliest potential date (the date could be announced after parliament returns from recess this week).

- Worth noting, however, there is nothing to stop the Budget being later in the year either. For example, in 2020 the Autumn Statement was held on 25 November. Realistically 17th December is the latest possible date.

NOK: Crude Strength Underpins NOK, Norges Sep Hold Risk May Be Underappreciated

NOK is second only to the USD in today’s G10 leaderboard, with a near-2% rally in Brent crude futures underpinning today’s strength. EURNOK is now down 1.1% this week at 11.6374, and almost 3% since August 20.

- Today’s EURNOK selloff narrows the gap to support at 11.6270 (61.8% retracement of the June to August rally), clearance of which would expose an historical pivot level around 11.6000.

- Our commodities team highlight that Russian supply fears remain a key support driver of crude prices, alongside strikes on Russian energy infrastructure over the last month. Meanwhile, Oil product strength in Europe has added support to crude as Shell announced a 2-month maintenance period at its Pernis refinery.

- This week’s Norwegian macro calendar is relatively light, with only Q2 current account and July industrial production data due. There will be much more focus on next week’s heavy schedule, which includes the General Election (Monday), August inflation data (Wednesday) and the Q3 Regional Network Survey (RNS, Thursday).

- The election result doesn’t look likely to have a major impact on the fiscal (and hence Norges Bank) outlook, with much more interest in the inflation and RNS data.

- While analysts generally still lean in favour of 25bp cuts in September and December, we think the risk of a September hold may be somewhat underappreciated. Norges Bank have been clear in guiding for “one or two” more cuts this year, and a hawkish set of figures next week could tempt the board into another cautious rate hold, particularly after the solid Q2 GDP report released a few weeks ago.

EQUITIES: E-Mini S&P Remains in Bullish Cycle of Higher Highs and Higher Lows

- The trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high appears corrective - for now. Note that support at 5375.94, the 50-day EMA, has been pierced. A clear break of this average would strengthen a S/T bearish threat and signal scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, resistance to watch is 5522.00, the Aug 22 high. A break of it would resume the uptrend.

- A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high last week. This maintains the bullish price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position too, highlighting a clear uptrend and positive market sentiment. Attention is on 6543.75, a Fibonacci projection. Support to watch lies at 6332.30, the 50-day EMA. The latest pullback appears corrective.

COMMODITIES: Gold Extends Current Bull Cycle, Breaches Key Resistance at $3500

- A bear cycle in WTI futures remains intact and recent gains are considered corrective. A key support at $61.99, the Jun 30 low, has recently been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high.

- Gold is trading sharply higher this week as the metal extends its bull cycle. Today’s gains have resulted in breach of key resistance at $3500.1, the Apr 22 high, and delivered a fresh all-time high. This confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3547.9, a Fibonacci projection. Initial firm support to watch lies at $3381.8, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 02/09/2025 | 1130/1330 | ECB Elderson and Machado Panel at ECB Legal Conference | ||

| 02/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/09/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 03/09/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/09/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/09/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/09/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/09/2025 | 0130/1130 | *** | Quarterly GDP | |

| 03/09/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/09/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 03/09/2025 | 0700/0300 | * | Turkey CPI | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0730/0930 | ECB Lagarde Speaks at ESRB Conference | ||

| 03/09/2025 | 0730/0830 | BOE Mann at Signum's London Westminster Day roundtable | ||

| 03/09/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0815/0915 | BOE Breeden at Innovation in Money and Payments Conference | ||

| 03/09/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/09/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/09/2025 | 0900/1100 | ** | EZ PPI | |

| 03/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/09/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/09/2025 | 1300/0900 | St. Louis Fed's Alberto Musalem | ||

| 03/09/2025 | 1315/1415 | BOE testify at TSC: Bailey, Greene, Lombardelli, Taylor | ||

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 03/09/2025 | 1800/1400 | Fed Beige Book |