MNI US MARKETS ANALYSIS - Weak Retail Sales Hit GBP

Highlights:

- Weak UK retail sales hits GBP, tips price back below uptrendline

- Hawkish BoJ sources story fails to prop up JPY

- Smooth Trump visit to Fed leaves STIR pricing fewest Fed cuts this year in months

US TSYS: Modestly Lower On Thin Volumes, Durable Goods Ahead

- Treasuries have stabilized after moving modestly lower overnight, outperforming EGBS throughout.

- A hawkish BOJ sources piece and yesterday’s ECB press conference has likely helped drive losses on the day, with the earlier shift higher in EGB yields appearing flow-driven.

- Today sees preliminary durable goods headline the docket whilst President Trump flies to Scotland.

- Cash yields are 0.5-2.3bp higher on the day, with increases lead by 30s.

- 30Y yields are 4.957% are off yesterday’s high of 4.989% having pulled back below 5% this week after a brief clearance last week for the first time since May.

- TYU5 trades at 110-25+ (-01) on particularly thin cumulative volumes of 195k, having remained within yesterday’s range throughout.

- Yesterday’s low of 110-19+, an hour after jobless claims as the ECB press conference was wrapping up, saw a step closer to a key support at 110-08+ (Jul 14/16 low). Resistance meanwhile is seen at 111-14+ (Jul 22 high).

- Data: Durable goods Jun prelim (0830ET), KC Fed services Jul (1100ET). Durable goods will mark one of the last updates before next week’s Q2 GDP advance release.

- Politics: Trump leaves the White House en route to Scotland (0800ET) with open press.

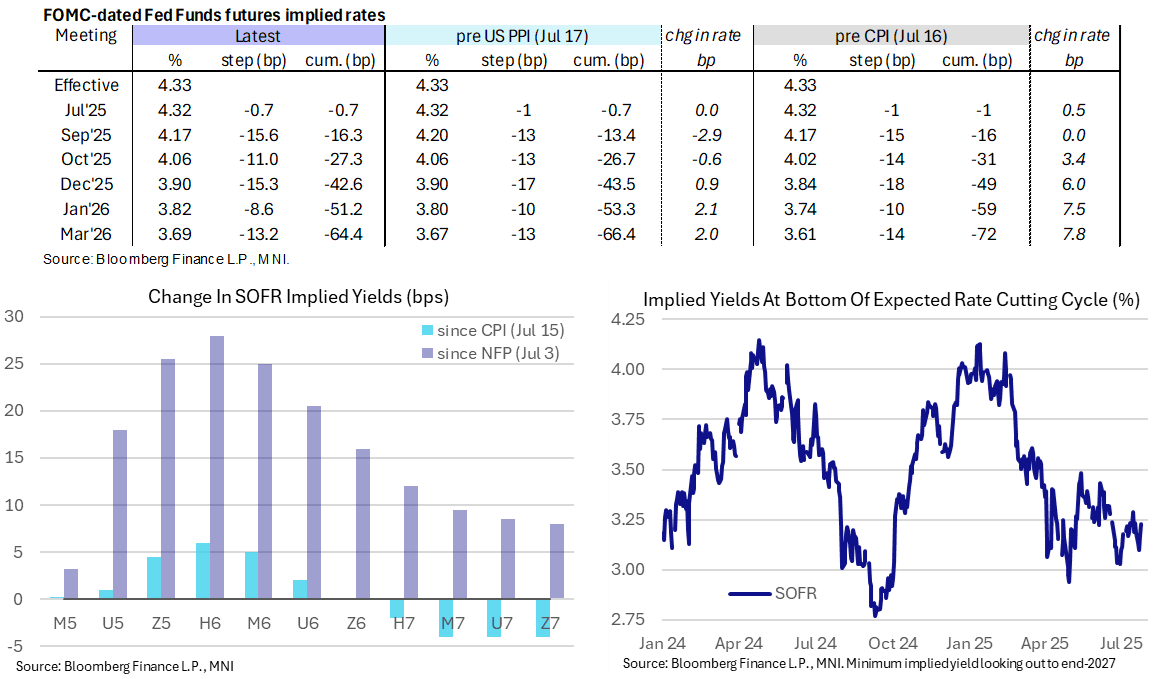

STIR: Holding Shift Close To Fewest 2025 Fed Cuts Priced Since February

- Fed Funds implied rates hold onto yesterday’s shift higher on lower-than-expected initial jobless claims, a net beat for flash PMIs and spillover from hawkish reaction to ECB’s Lagarde.

- Bloomberg following Trump’s visit to the Fed: “After a tour that saw Trump and Powell publicly trade barbs over the cost of the project, Trump maintained there was “no tension” with the Fed chief and indicated that problems with the project probably weren’t reason enough to fire the central bank head.”

- Cumulative cuts from 4.33% effective: 0.5bp Jul 30, 16bp Sep, 27.5bp Oct, 42.5bp Dec, 51bp Jan and 64bp Mar.

- The SOFR implied terminal yield is unchanged at 3.23% (SFRH7) having shifted back closer to four rather than five cuts for what’s left of the easing cycle.

- Today’s thin docket sees focus on the preliminary durable goods report for June.

US TSY FUTURES: Mix Of Positioning Moves Seen During Thursday's Twist Flattening

OI data points to a mix of net short setting (TU, FV, TY & UXY), long cover (US) and short cover (WN) as the curve twist flattened on Thursday.

- The net cover in US & WN provided the most meaningful net positioning moves on the curve from a DV01 equivalent perspective.

| 24-Jul-25 | 23-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,374,498 | 4,372,011 | +2,487 | +92,278 |

FV | 6,969,249 | 6,966,892 | +2,357 | +100,487 |

TY | 4,811,939 | 4,806,792 | +5,147 | +336,753 |

UXY | 2,413,017 | 2,406,720 | +6,297 | +544,329 |

US | 1,767,776 | 1,773,624 | -5,848 | -799,940 |

WN | 1,928,194 | 1,935,810 | -7,616 | -1,372,262 |

|

| Total | +2,824 | -1,098,355 |

SOFR: Mix Of short Setting & Long Cover Seen Thursday

OI data points to net short setting dominating in most of the white SOFR futures during Thursday's sell off, before net long cover moved to the fore further out the strip, with only two rounds of net short setting seen beyond the whites.

| 24-Jul-25 | 23-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,276,052 | 1,256,420 | +19,632 | Whites | +29,245 |

SFRU5 | 1,299,262 | 1,302,507 | -3,245 | Reds | -14,958 |

SFRZ5 | 1,321,223 | 1,316,404 | +4,819 | Greens | -14,596 |

SFRH6 | 1,031,522 | 1,023,483 | +8,039 | Blues | -10,750 |

SFRM6 | 868,777 | 857,522 | +11,255 |

|

|

SFRU6 | 825,523 | 837,543 | -12,020 |

|

|

SFRZ6 | 916,279 | 921,614 | -5,335 |

|

|

SFRH7 | 723,109 | 731,967 | -8,858 |

|

|

SFRM7 | 698,360 | 711,538 | -13,178 |

|

|

SFRU7 | 517,906 | 519,027 | -1,121 |

|

|

SFRZ7 | 449,803 | 448,865 | +938 |

|

|

SFRH8 | 330,845 | 332,080 | -1,235 |

|

|

SFRM8 | 224,359 | 227,133 | -2,774 |

|

|

SFRU8 | 200,770 | 205,451 | -4,681 |

|

|

SFRZ8 | 203,102 | 204,347 | -1,245 |

|

|

SFRH9 | 144,407 | 146,457 | -2,050 |

|

|

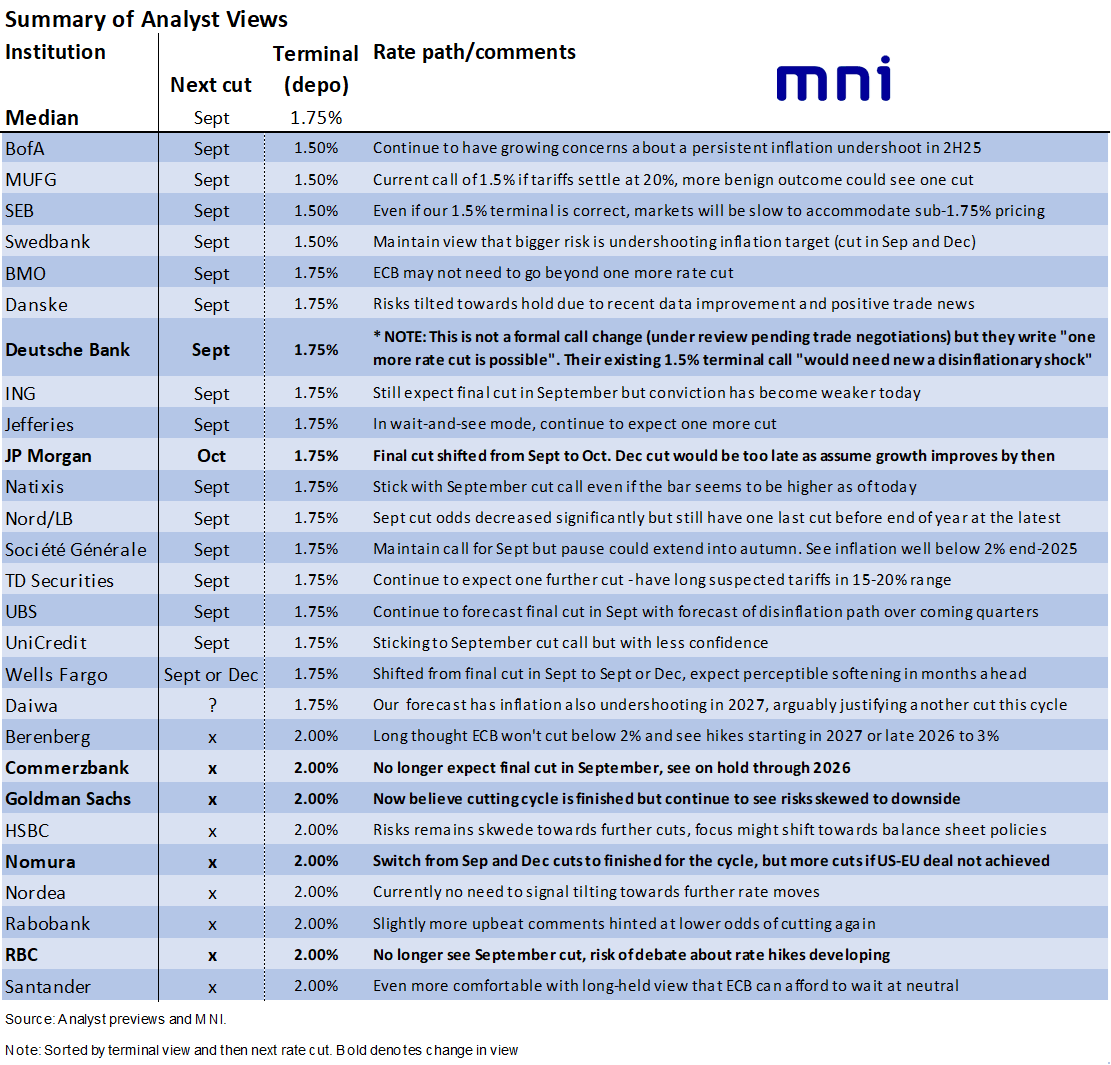

ECB: Hawkish Shifts In Analyst ECB Calls But Median Still Eyes 1.75% Terminal

- We count at least six hawkish changes to analyst rate calls after yesterday’s ECB decision and press conference (including Deutsche Bank which isn’t a formal view change but was hinted at).

- There is still a median terminal rate of 1.75%, with the final cut coming in September (vs just 4bp currently priced for the meeting) but there are multiple mentions of a higher bar for such a move.

- 9 of 27 analysts now look for no further cuts vs 5 of 29 analysts in the MNI preview.

- Specifically, Berenberg, HSBC, Nordea, Rabobank and Santander are joined by Commerzbank, Goldman Sachs, Nomura and RBC in calling for a 2% terminal.

- One added mention, whilst those who expect a cut generally still see September as their base case (with that higher bar), JPMorgan stand out with their shift to an Oct cut (i.e. outside of a projection meeting). They don’t push it back to Dec as their baseline forecast has growth starting to improve again by then.

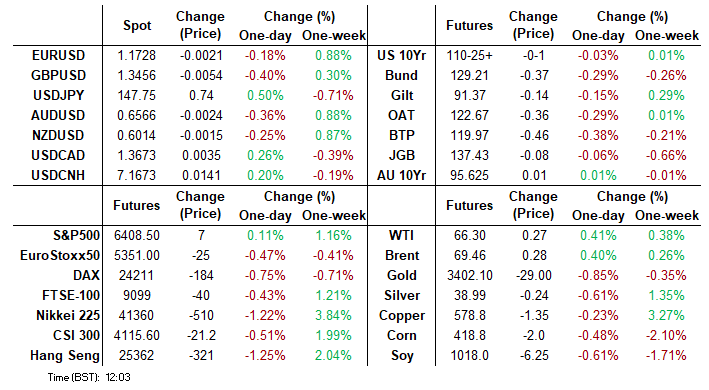

FOREX: Unusually Strong Volumes for a Friday, JPY Will Need More Rates Impetus

The rate-driven demand for USD/JPY has the pair comfortably through 147.52 resistance but further relief for the longer-end of the Japanese curve will likely be needed to tip prices through Y148 and anywhere closer to 149.19. The sensitivity to the long-end has firmed this week and raises the focus on 10y, 30y JGB auctions at the beginning of August (conveniently the week after the July Fed decision). Markets have shrugged off overnight reports that the BoJ are said to see potential rate hike environment in 2025 - which sits broadly inline with market pricing.

- GBP/USD trading back below broken uptrendline support drawn off the January low is a by-product of this USD demand - particularly as today's retail sales firms the focus on the August 7th BoE (at which a 25bps rate cut is effectively fully priced). The rate has oscillated either side of this trend (today at 1.3511). June retail sales came in notably below expectations, at 0.6% on the month vs. Exp. 1.2%.

- This makes for a decent start to the session for FX futures volumes: EUR, JPY and GBP futures are all seeing above-average activity - particularly for a Friday.

- Optionality today sees $600mln interest across Y147.75-85 strikes in USD/JPY, E1.7bln at $1.1740-50 in EUR/USD, while the rallies in both EUR/GBP and USD/CAD bring sizeable strikes at 0.8725-50 and 1.3700-20 into play (E892mln and $1.2bln respectively).

- Focus for the duration of Friday trade turns to the Kansas City Fed Services data and any post-decision commentary from members of the ECB governing council after yesterday's press conference leaned hawkish and suggested scant opportunity for further rate cuts this year. The Fed remain inside their pre-meeting media blackout period.

FOREX: EUR Crosses Continue to Trend North, Cycle Highs for EURJPY

- Earlier in the week, we wrote about how bullish indicators have been prevailing for EUR crosses, highlighting the impressive rallies for the likes of EURJPY, as trepidation surrounding the Japanese fiscal outlook lingers, and EURNZD following the softer domestic CPI reads.

- EURJPY (+0.42%) has printed fresh 12-month highs above 173.50 as the cautious yen optimism following Sunday’s upper house election dissipates. Opponents have secured the requisite signatures to convene a joint meeting of upper and lower house lawmakers from the governing LDP, stoking the already high levels of uncertainty surrounding PM Ishiba’s future.

- The ECB sounding notably constructive on euro area growth and several analysts no longer expecting further cuts this cycle also maintains a supportive Euro backdrop.

- Today’s move above 173.43 provides another bullish technical development for EURJPY, and a close at current levels would cement a ninth consecutive week of gains, the longest winning streak since 2008. Above here, 174.86 (Fib projection) provides the next target before 175.43, the July 11 ‘24 high and a key medium-term resistance.

HKD: USD/HKD Off Weak-Side as Front-End Rates Finally Move Higher

Spot USD/HKD has faded off the 7.85 weak-side of the band today in the most material price action of the week so far. In trade similar to the Jul 17th pull lower in spot, there is little evidence of HKMA intervention here - raising the likelihood that the vol in spot is led by a rebalancing of positioning, rather than official involvement.

- There has been some movement in front-end of the HKD swaps curve: one-week had been marked above 1.00%, and if it holds here, will be the strongest move in local rates since May's sharp spell of HKD weakness.

- The minor pressure in the front-end of the swaps curve spells upside risks for HIBOR fixes into next week (both the 1m and 3m fixes today were flat or lower) - which may make intraday spells of HKD strength (as seen this morning) stickier going forward.

OPTIONS: Expiries for Jul25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E679mln), $1.1740-50(E1.7bln), $1.1800(E2.1bln)

- USD/JPY: Y145.00($1.2bln), Y146.00($841mln), Y147.75-85($600mln)

- EUR/GBP: Gbp0.8725-50(E892mln)

- AUD/USD: $0.6450($552mln)

- USD/CAD: C$1.3700-20($1.2bln)

EQUITIES: E-Mini S&P Climbs to Fresh Cycle Highs

- The trend condition in Eurostoxx 50 futures remains bullish and short-term weakness for now, appears corrective. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. For bulls, a resumption of gains would refocus attention on key resistance and the bull trigger at 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00.

- S&P E-Minis have traded to fresh cycle highs this week. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. With the 6400.00 handle cleared, sights are on 6439.88, a Fibonacci projection. Key support is at the 50-day EMA, at 6142.04. Support at the 20-day EMA is at 6289.07.

COMMODITIES: Gold's Short-Term Weakness Corrective, Bull Cycle Still Intact

- A bearish theme in WTI futures remains intact and the shallow recovery since Jun 24 still appears corrective. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $64.75. The average has been pierced, a clear break of it would expose $58.17, the May 30 low. On the upside, initial resistance to watch is $69.41, the 50.0% retracement of the Jun 23 - 24 high-low range.

- Gold has pulled back from Tuesday’s high. Short-term weakness is considered corrective and a bull cycle that started Jun 30 remains intact. Resistance at $3395.1, the Jun 23 high, has recently been cleared. A continuation higher would open $3451.3, the Jun 16 high. Note that MA studies are in a bull-mode position highlighting a dominant uptrend. An initial firm support to watch is 3282.8, the Jul 9 low.

| Date | GMT/Local | Impact | Country | Event |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 25/07/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |